REPORT ON EXAMINATION

OF

BROOME CO-OPERATIVE INSURANCE COMPANY

AS OF

DECEMBER 31, 2017

DATE OF REPORT JANUARY 4, 2019

EXAMINER SABU CHERIAN

TABLE OF CONTENTS

ITEM NO. PAGE NO.

1

.

Scope of

e

xamination

2

2.

Description of Company

3

A.

Corporate governance

3

B. Territory and plan of operation 4

C.

Reinsurance ceded

5

D. Holding company system 7

E.

Significant ratios

7

3

.

Financial

s

tatements

8

A.

Balance sheet

8

B. Statement of income 10

C.

Capital and surplus account

11

4.

Losses and loss adjustment expenses

11

5

.

Compliance with prior report on examination

12

6

.

Summary of comments and recommendations

13

One State Street, New York, NY 10004-1511 │ (212) 480-6400│ www.dfs.ny.gov

ANDREW M. CUOMO

Governor

LINDA A. LACEWELL

Acting Superintendent

April 24, 2019

Honorable Linda A. Lacewell

Acting Superintendent

New York State Department of Financial Services

Albany, New York 12257

Madam:

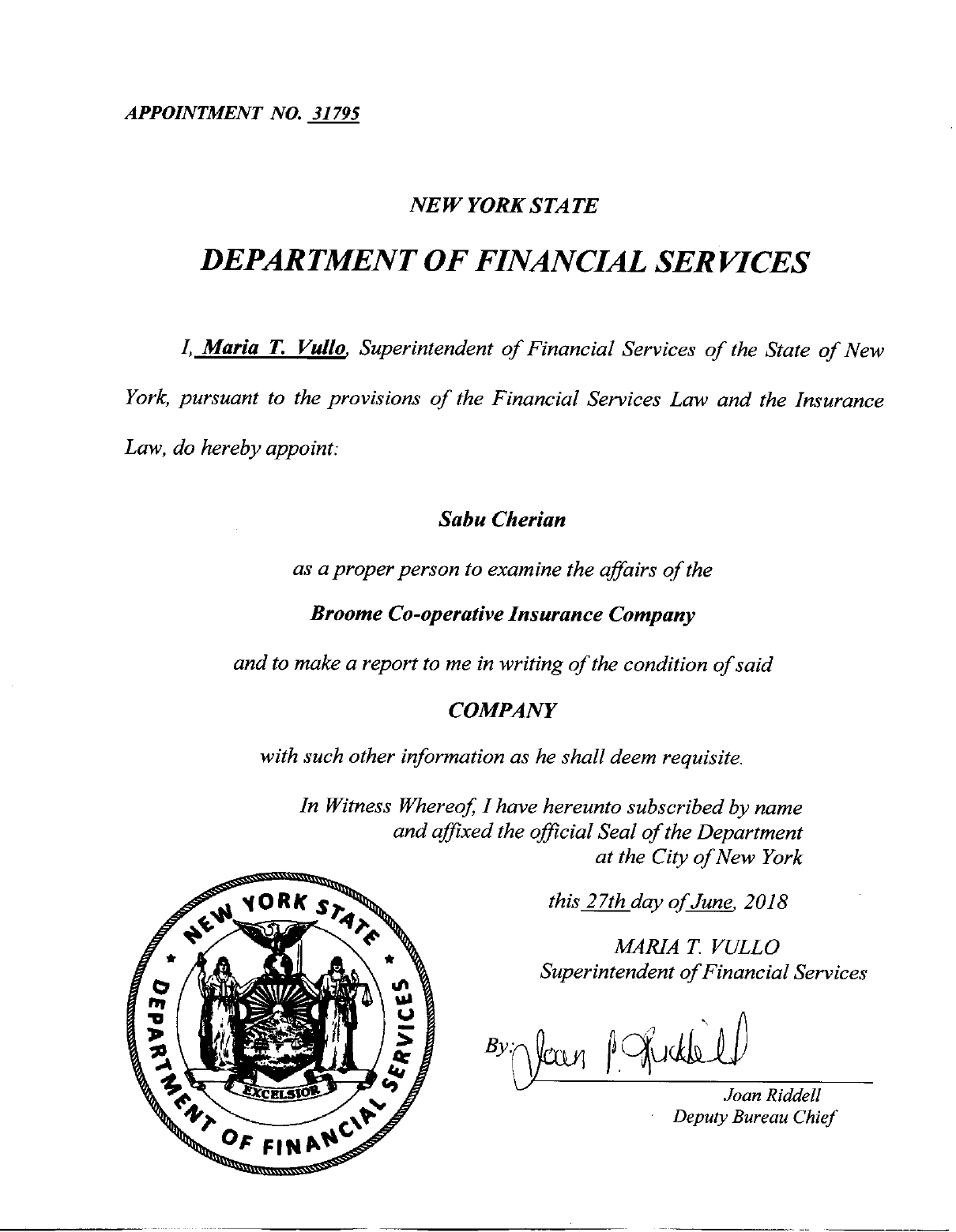

Pursuant to the requirements of the New York Insurance Law, and in compliance with the instructions

contained in Appointment Number 31795 dated June 27, 2018, attached hereto, I have made an

examination into the condition and affairs of Broome Co-operative Insurance Company as of December

31, 2017, and submit the following report thereon.

Wherever the designation “the Company” appears herein without qualification, it should be understood

to indicate Broome Co-operative Insurance Company.

Wherever the term “Department” appears herein without qualification, it should be understood to mean

the New York State Department of Financial Services.

The examination was conducted at the Company’s administrative office located at 1923 Vestal Parkway

East, Vestal, New York 13851.

2

1. SCOPE OF EXAMINATION

The Department has performed an examination of the Company, a single-state insurer. The previous

examination was conducted as of December 31, 2012. This examination covered the five-year period from

January 1, 2013 through December 31, 2017. Transactions occurring subsequent to this period were

reviewed where deemed appropriate by the examiner.

This examination was conducted in accordance with the National Association of Insurance

Commissioners (“NAIC”) Financial Condition Examiners Handbook (“Handbook”), which requires that

we plan and perform the examination to evaluate the financial condition and identify current and prospective

risks of the Company by obtaining information about the Company including corporate governance,

identifying and assessing inherent risks within the Company and evaluating system controls and procedures

used to mitigate those risks. This examination also includes assessing the principles used and significant

estimates made by management, as well as evaluating the overall financial statement presentation,

management’s compliance with New York laws, statutory accounting principles, and annual statement

instructions.

This examination report includes, but is not limited to, the following:

Company history

Management and control

Territory and plan of operation

Reinsurance

L

oss

review and analysis

Financial statement presentation

Significant subsequent events

Summary of recommendations

A review was also made to ascertain what action was taken by the Company with regard to

comments and recommendations contained in the prior report on examination.

This report on examination is confined to financial statements and comments on those matters that

involve departures from laws, regulations or rules, or that are deemed to require explanation or description.

3

2. DESCRIPTION OF COMPANY

The Company was incorporated under the laws of the State of New York as the Broome County

Farmers’ Fire Relief Association (“Association”) on January 20, 1887 for the purpose of transacting the

business as an assessment cooperative fire insurance association in Broome County of New York State.

In 1951, the Association merged with Broome County Patrons’ Fire Relief Association of Whitney

Point, New York and the surviving corporation resulting from said merger became the Broome County Co-

operative Fire Insurance Company.

On March 27, 2002, approval was given by the Department for the Company to change its name

from “Broome County Co-operative Fire Insurance Company to “Broome Co-operative Insurance

Company.”

A. Corporate Governance

Pursuant to the Company’s charter and by-laws, management of the Company is vested in a board

of directors consisting of not less than seven nor more than ten members. The board meets four times

during each calendar year. At December 31, 2017, the board of directors was comprised of the following

seven members:

Name and Residence

Principal Business Affiliation

Kimberly S. Chidester

Lisle, New York

Owner,

Lakeside Bookkeeping & Tax Service.

J. Paul Cavatio

Owego, New York

Owner,

Agway Stores

Steven J. Coffey

Binghamton, New York

Steven D. Contento

Windsor, New York

Clifford W. Crouch

Bainbridge, New York

Michael Decker

Whitney Point, New York

President & CEO,

Broome Co-operative Insurance Co.

Director,

Ross Park Zoo

Assemblyman,

New York State

Broker,

ERA Decker Realty

4

Name and Residence

Principal Business Affiliation

Debra K. Eaton-Turner

Smithville Flats, New Jersey

Ralph E. Kelsey

Endicott, New York

Marc J. Palumbo

Dryden, New York

Siobhan G. Davey

Vestal, New York

Bank Manager,

NBT Bank

Retired,

Tioga State Bank

Claims Adjuster,

Larose & Palumbo Claim Service

Chief Operating Officer,

Broome Co

-

o

perative Insurance Co.

At December 31, 2017, the principal officers of the Company were as follows:

B. Territory and Plan of Operation

At December 31, 2017, the Company was licensed to write business in New York only.

As of the examination date, the Company was authorized to transact the kinds of insurance as

defined in the following numbered paragraphs of Section 1113(a) of the New York Insurance Law:

Paragraph

Line of Business

4 Fire

5

Miscellaneous property

6 Water damage

7

Burglary and

theft

8 Glass

9

Boiler and machinery

12 Collision

13

Personal injury liability

14 Property damage liability

15 Workers' compensation and employers' liability (excluding

workers’ compensation)

19 Motor vehicle and aircraft physical damage (excluding aircraft

physical damage)

20

Marine and inland marine

(Inland only)

Name

Title

Steven J.Coffey

President

Siobhan G. Davey Chief Operating Officer

Ian T. Coffey

Vice President of Finance

Steven D. Contento Secretary/Treasurer

5

The Company is also licensed to accept and cede reinsurance provided in section 6606 of the New

York Insurance Law.

Based upon the lines of business for which the Company is licensed and the Company’s current

capital structure, and pursuant to the requirements of Articles 13, 41 and 66 of the New York Insurance

Law, the Company is required to maintain a minimum surplus to policyholders in the amount of $100,000.

The company did not assume any business during the examination period. The following schedule

shows the total gross premiums written by the Company for the period under examination:

Calendar Year

Total Gross Premiums

2013 $6,928,222

2014 $7,609,594

2015

$7,599,302

2016 $7,944,401

2017

$7,997,528

The Company predominantly wrote homeowners (51.3 %) and commercial (39.9%) multiple peril

in 2017. The Company’s products and services are distributed through a network of seventy-three

independent agents located in Southern tier, Central, and Western part of the New York State.

C. Reinsurance Ceded

The Company ceded $1,158,000 and has a reinsurance recoverable of $938,000 from reinsurers as

reported in the Company’s Schedule F.

The reinsurance treaties and arrangements principally consists of traditional reinsurance

arrangements whereby the reinsurer assumes a portion of the losses for a cost. The reinsurance contracts

cover property and casualty business and are as follows:

Type of Treaty Cession

Property Excess of Loss

(3 layers) 100% authorized

$850,000 excess of $150,000 ultimate net loss, each

loss, subject to a limit of liability to the reinsurer of

$2,55

0,000 each loss occurrence.

6

Type of Treaty

Cession

Casualty Excess of Loss

(3 layers) 100% authorized

$900,000 excess of $100,000 ultimate net loss, each

loss occurrence.

Property and Casualty Combined

(1 layer) 100% authorized

$150,000 excess of $100,000 ultimate net loss each

loss occurrence involving property and casualty loss.

Casualty Clash Excess of Loss

(1 layer) 100% authorized

$1,000,000 excess of $1,000,000 ultimate net loss,

each loss occurrence.

Property Catastrophe Excess of Loss

(3 layers) 100% authorized

$6,600,000 excess of $400,000 ultimate net loss each

loss, subject to a limit of liability to the reinsurer of

$13,200,000 for all loss occurrences during the term

of the contract. No claim shall be covered unless the

loss occurrence involves two or more risks insured or

reinsured by the Company.

At December 31, 2017, the Company ceded one hundred percent of its boiler and machinery net

retained liability.

The majority of the recoverable amounts reported on Schedule F – Part 3 are from Farmers Mutual

Hail Insurance Co. of Iowa (41%), Renaissance Reinsurance US Inc. (22%) and QBE Reinsurance Corp.

(11%), which are all authorized reinsurers.

All significant reinsurance agreements in effect as of the examination date were reviewed and found

to contain the required clauses, including an insolvency clause, meeting the requirements of Section 1308

of the New York Insurance Law.

Examination review found that the Schedule F data reported by the Company in its filed annual

statement accurately reflected its reinsurance transactions. Additionally, management has represented that

all material ceded reinsurance agreements transfer both underwriting and timing risk as set forth in SSAP

No. 62R. Representations were supported by an appropriate risk transfer analyses and an attestation from

the Company’s Chief Executive Officer and Chief Financial Officer pursuant to the NAIC Annual

Statement Instructions. Additionally, examination review indicated that the Company was not a party to

any finite reinsurance agreements. All ceded reinsurance agreements were accounted for utilizing

reinsurance accounting as set forth in SSAP No. 62R.

7

D. Holding Company System

At December 31, 2017, the Company was not a member to a holding company system and did not

have any affiliated or pooling agreements in force.

E. Significant Ratios

The Company’s operating ratios, computed as of December 31, 2017, fall within the benchmark

ranges set forth in the Insurance Regulatory Information System of the National Association of Insurance

Commissioners.

Operating Ratios Result

Net premiums written to surplus as regards policyholders 46%

Liabilities to liquid assets (cash and invested assets less investments in affiliates)

34

%

Two-year overall operating 82%

Underwriting Ratios

The underwriting ratios presented below are on an earned/incurred basis and encompass the five-

year period covered by this examination:

Amounts

Ratio

Losses and loss adjustment expenses incurred $17,624,102

56.91%

Other underwriting expenses incurred

11,874,320

38.34%

Net underwriting gain

1,469,631

4.

75%

Premiums earned

$

30,968,053

100.00%

The Company’s reported risk based capital score (“RBC”) was 1,716.9% at 12/31/2017. The RBC

is a measure of the minimum amount of capital appropriate for a reporting entity to support its overall

business operations in consideration of its size and risk profile. An RBC of 200 or below can result in

regulatory action. There were no financial adjustments in this report that impacted the Company’s RBC

score.

8

3. FINANCIAL STATEMENTS

A. Balance Sheet

The following shows the assets, liabilities and surplus as regards policyholders as of December 31,

2017, as reported by the Company:

Assets

Assets

Assets Not

Admitted

Net Admitted

Assets

Bonds $14,913,294

$14,913,294

Common stocks (stocks)

5,285,587

5,285,587

First liens - mortgage loans on real estate 1,028

1,028

Properties occupied by the company

795,841

795,841

Cash, cash equivalents and short-term investments 541,626

541,626

Company owned life

i

nsurance

64,180

64,180

Investment income due and accrued 99,387

99,387

Uncollected premiums and agents' balances in the

course of collection 147,470 $10,249 137,221

Deferred premiums, agents' balances and

installments booked but deferred and not yet due 864,738 864,738

Amounts recoverable from reinsurers

85,625

85,625

Prepaid commissions 26,078 26,078 0

Cash corrections

(5)

(5)

0

Totals $22,885,165 $96,638 $22,788,527

9

Liabilities,

S

urplus and

O

ther

F

unds

Liabilities

Losses and loss adjustment expenses

$3,100,547

Commissions payable, contingent commissions and other similar

Charges

351,430

Other expenses (excluding taxes, licenses and fees)

205,358

Taxes, licenses and fees (excluding federal and foreign income

taxes)

1,992

Current federal and foreign income taxes

14,562

Net deferred tax liability

70,590

Unearned premiums

4,060,945

Advance premium

146,760

Ceded reinsurance premiums payable (net of ceding commissions)

(61,877)

Total liabilities

$7,890,237

Surplus and other funds

Unassigned funds (surplus)

$

14,898,289

Surplus as regards policyholders 14,898,289

Total liabilities, surplus and other funds

$22,788,526

Note: The Internal Revenue Service has not performed any audits of the examination years. The examiner

is unaware of any potential exposure of the Company to any tax assessment and no liability has been

established herein relative to such contingency.

10

B. Statement of Income

The net income for the examination period as reported by the Company was $2,806,053 as detailed

below:

Underwriting

in

come

Premiums earned

$

30,968,053

Deductions:

Losses and loss adjustment expenses incurred

$

17,624,102

Other underwriting expenses incurred

11,874,320

Total underwriting deductions

29,498,422

Net underwriting gain

$

1,469,631

Investment

i

ncome

Net

investment income earned

$ 1,468,591

Net realized capital gain

or (loss)

432,833

Net investment gain

1,901,424

Other

i

ncome

Net

gain or

(

loss

)

from agents' or premium balances charged off

$

10,148

Finance and service

charges not included in premiums

637,236

Aggregate write

-

ins for miscellaneous income

$

(48,408)

Total other income

598,976

Net income before federal

and foreign income taxes

$

3,970,031

Federal and foreign income taxes

incurred

1,109,978

Net

i

ncome

$

2

,860,053

11

C. Capital and Surplus Account

Surplus as regards policyholders increased $3,906,103 during the five-year examination period

January 1, 2013 through December 31, 2017 as reported by the Company, detailed as follows:

Surplus as regards policyholders as reported

by the Company as of December 31, 2012

$ 10,992,186

Gains in

Losses in

Surplus Surplus

Net income

$

2,860,053

Net unrealized capital gains or (losses) 764,760

Change in net deferred income tax

45,231

Change in non-admitted assets 236,059

Net increase in surplus

$3,906,103

$

3,906,103

Surplus as regards policyholders as reported

by the Company as

of December 31, 2017

$

14,898,289

No adjustments were made to surplus as a result of this examination.

4. LOSSES AND LOSS ADJUSTMENT EXPENSES

The examination liability for the captioned items of $3,100,547 is the same as reported by the

Company as of December 31, 2017. The examination analysis of the loss and loss adjustment expense

reserves was conducted in accordance with generally accepted actuarial principles and statutory accounting

principles, including the NAIC Accounting Practices & Procedures Manual, Statement of Statutory

Accounting Principle No. 55 (“SSAP No. 55”).

Significant reserves are concentrated in the following lines of business: Commercial multiple peril

(56%), Homeowners multiple peril (39%) and Other Liability - Occurrence (2%) Other Liability -

Occurrence consists of dwelling fire - liability.

12

5. COMPLIANCE WITH PRIOR REPORT ON EXAMINATION

The prior report on examination contained six recommendations as follows (page numbers refer to

the prior report):

ITEM

A.

i.

ii.

iii.

B.

C.

i.

ii.

Management

It is recommended that the Company implement control procedures to

ensure that its funds are not used to pay for non-business-related

expenses pursuant to Section 1217 of the New York Insurance Law,

Section 715(h) of the Business Corporation Law and the Company’s

own Travel and Expense Policy.

The Company has complied with this recommendation.

It is recommended that the Company’s board of directors review all

corporate credit usage during the examination period and seek

reimbursement of all expenses for which a specified business purpose is

not demonstrated.

The Company has complied with this recommendation.

It is recommended that the Company comply with Section 6613(a) of

the New York Insurance Law and monitor management expenses to

ensure they do not exceed 42.5% of net premiums written.

The Company has complied with this recommendation.

Reinsurance

It is recommended that the Company comply with SSAP No. 62R,

paragraph 8(d) by amending its reinsurance agreements to include all

required terms.

The Company has complied with this recommendation.

Accounts and Records

It is recommended that the Company report its loss data to the correct

lines of business on its filed annual statements pursuant to the NAIC

Annual Statement Instructions.

The Company has complied with this recommendation.

It is recommended that the Company obtain all required forms prior to

making claim payments pursuant to Regulation 21 and 96.

The Company has complied with this recommendation.

PAGE NO.

5

5

6

9

10

10

13

6. SUMMARY OF COMMENTS AND RECOMMENDATIONS

This report on examination does not contain any comments or recommendations.

Respectfully submitted,

/S/

Sabu Cherian

Financial Services Examiner 2

STATE OF NEW YORK )

)ss:

COUNTY OF NEW YORK )

Sabu Cherian, being duly sworn, deposes and says that the foregoing report, subscribed by him, is

true to the best of his knowledge and belief.

/S/

Sabu Cherian

Subscribed and sworn to before me

this day of , 2019.