UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, DC 20549

FORM 10-Q

☒

QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the quarterly period ended June 30, 2022

Or

☐

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to i

Commission File No. 001-37660

Avangrid, Inc.

(Exact Name of Registrant as Specified in its Charter)

New York 14-1798693

(State or other jurisdiction of incorporation or organization) (I.R.S. Employer Identification No.)

180 Marsh Hill Road

Orange, Connecticut 06477

(Address of principal executive offices) (Zip Code)

Registrant’s telephone number, including area code: (207) 629-1190

Securities registered pursuant to Section 12(b) of the Act:

Title of each class Trading Symbol Name of exchange on which registered

Common Stock, par value $0.01 per share AGR New York Stock Exchange

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange

Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been

subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to

Rule 405 of Regulation S-T (§ 232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was

required to submit such files). Yes ☒ No ☐

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, smaller reporting

company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company,”

and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer

☒

Accelerated Filer

☐

Non-accelerated Filer

☐

Smaller Reporting Company

☐

Emerging Growth Company

☐

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying

with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

As of July 26, 2022, the registrant had 386,624,231 shares of common stock, par value $0.01, outstanding.

Avangrid, Inc.

REPORT ON FORM 10-Q

For the Quarter Ended June 30, 2022

INDEX

GLOSSARY OF TERMS AND ABBREVIATIONS 3

PART I. FINANCIAL INFORMATION 5

Item 1. Financial Statements 5

Item 2. Management’s Discussion and Analysis of Financial Condition and Results of Operations 53

Item 3. Quantitative and Qualitative Disclosures about Market Risk 72

Item 4. Controls and Procedures 72

PART II. OTHER INFORMATION 74

Item 1. Legal Proceedings 74

Item 1A. Risk Factors 74

Item 2. Unregistered Sales of Equity Securities and Use of Proceeds 74

Item 3. Defaults Upon Senior Securities 74

Item 4. Mine Safety Disclosures 74

Item 5. Other Information 74

Item 6. Exhibits 75

SIGNATURES 76

2

GLOSSARY OF TERMS AND ABBREVIATIONS

Unless the context indicates otherwise, the terms “we,” “our” and the “Company” are used to refer to Avangrid, Inc. and its

subsidiaries.

2020 Joint Proposal

Joint proposal of NYSEG and RG&E and certain other signatory parties approved by the

NYPSC on November 19, 2020, for a three-year rate plan for electric and gas service

commencing December 1, 2020.

AOCI

Accumulated other comprehensive income

ARHI

Avangrid Renewables Holdings, Inc.

ARP

Alternative Revenue Programs

ASC

Accounting Standards Codification

AVANGRID

Avangrid, Inc.

BGC

The Berkshire Gas Company

CfDs

Contracts for Differences

CFIUS

Committee on Foreign Investment in the United States

CL&P

The Connecticut Light and Power Company

CMP

Central Maine Power Company

CNG

Connecticut Natural Gas Corporation

DEEP

Connecticut Department of Energy and Environmental Protection

DIMP

Distribution Integrity Management Program

DOC

Department of Commerce

DPA

Deferred Payment Arrangements

DPU

Massachusetts Department of Public Utilities

EBITDA

Earnings before interest, taxes, depreciation and amortization

ESM

Earnings sharing mechanism

Evergreen Power

Evergreen Power, LLC

English Station

The former generation site on the Mill River in New Haven, Connecticut

Exchange Act

The Securities Exchange Act of 1934, as amended

FASB

Financial Accounting Standards Board

FCC

Federal Communications Commission

FERC

Federal Energy Regulatory Commission

FirstEnergy

FirstEnergy Corp.

Form 10-K

Avangrid, Inc.’s Annual Report on Form 10-K for the year ended December 31, 2021, filed

with the Securities and Exchange Commission on March 1, 2022.

HLBV

Hypothetical Liquidation at Book Value

Iberdrola

Iberdrola, S.A., which owns 81.5% of the outstanding shares of Avangrid, Inc.

Iberdrola Group

The group of companies controlled by Iberdrola, S.A.

Installed capacity

The production capacity of a power plant or wind farm based either on its rated (nameplate)

capacity or actual capacity.

ISO

Independent system operator

Klamath Plant

Klamath gas-fired cogeneration facility located in the city of Klamath, Oregon.

KW

Kilowatts

LIBOR

The London Interbank Offered Rate

Merger

The merger of PNMR with and into Merger Sub on the terms and subject to the conditions set

forth in the Merger Agreement, with PNMR continuing as the surviving corporation and as a

wholly-owned subsidiary of AVANGRID.

Merger Agreement

Agreement and Plan of Merger, dated as of October 20, 2020, among AVANGRID, PNMR and

Merger Sub.

3

Merger Sub

NM Green Holdings, Inc., a New Mexico corporation and wholly-owned subsidiary of

AVANGRID.

MNG

Maine Natural Gas Corporation

MPUC

Maine Public Utility Commission

MtM

Mark-to-market

MW

Megawatts

MWh

Megawatt-hours

Networks

Avangrid Networks, Inc.

New York TransCo

New York TransCo, LLC.

NMPRC

New Mexico Public Regulation Commission

Non-GAAP

Financial measures that are not prepared in accordance with U.S. GAAP, including adjusted net

income, adjusted earnings per share, adjusted EBITDA and adjusted EBITDA with tax credits.

NRC

Nuclear Regulatory Commission

NYPSC

New York State Public Service Commission

NYSE

New York Stock Exchange

NYSEG

New York State Electric & Gas Corporation

NYSERDA

New York State Energy Research and Development Authority

OCI

Other comprehensive income

PJM

PJM Interconnection, L.L.C.

PNMR

PNM Resources, Inc.

PUCT

Public Utility Commission of Texas

PURA

Connecticut Public Utilities Regulatory Authority

Renewables

Avangrid Renewables, LLC

RDM

Revenue Decoupling Mechanism

RG&E

Rochester Gas and Electric Corporation

ROE

Return on equity

SCG

The Southern Connecticut Gas Company

SEC

United States Securities and Exchange Commission

Tax Act

Tax Cuts and Jobs Act of 2017 enacted by the U.S. federal government on December 22, 2017

TEF

Tax equity financing arrangements

UI

The United Illuminating Company

UIL

UIL Holdings Corporation

U.S. GAAP

Generally accepted accounting principles for financial reporting in the United States.

VIEs

Variable interest entities

4

PART I. FINANCIAL INFORMATION

Item 1. Financial Statements

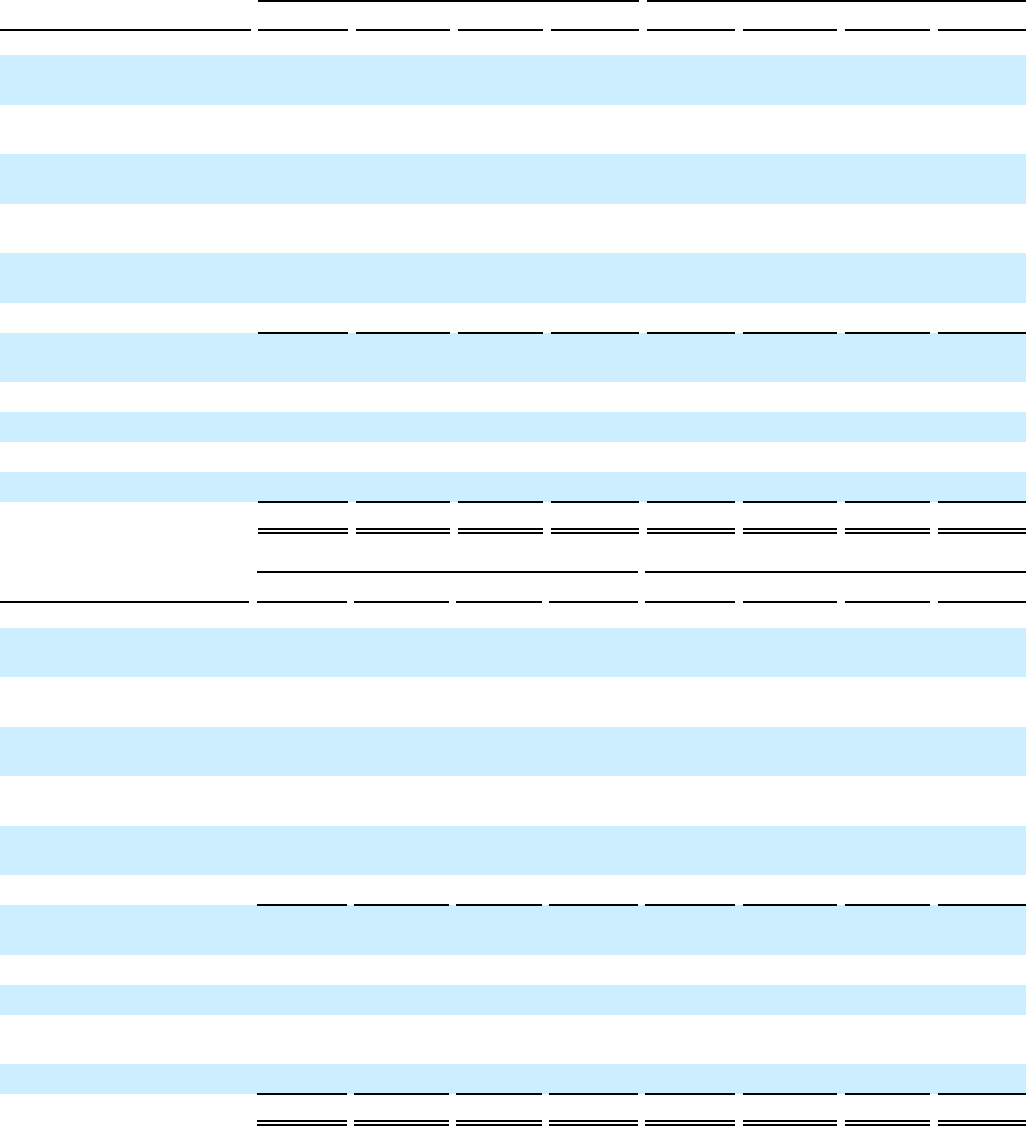

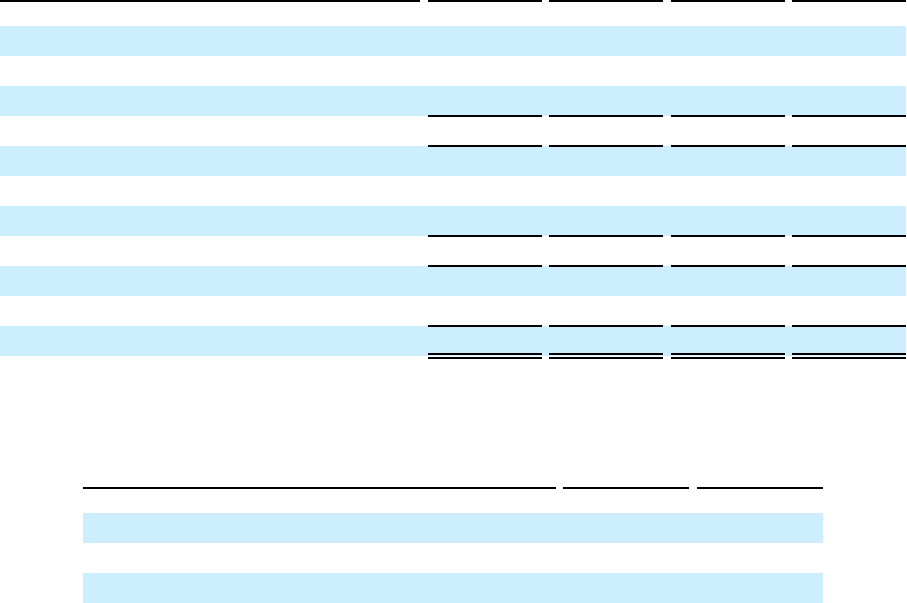

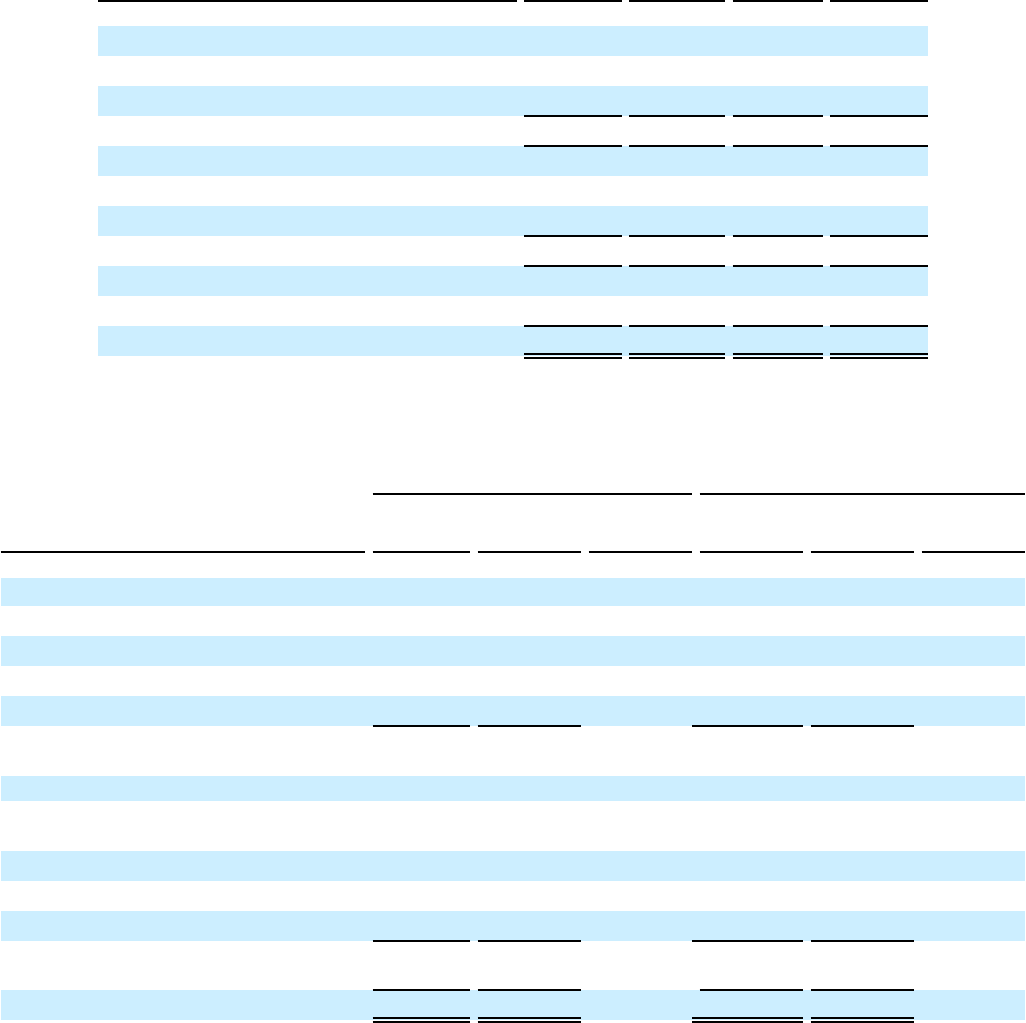

Avangrid, Inc. and Subsidiaries

Condensed Consolidated Statements of Income

(unaudited)

Three Months Ended June 30, Six Months Ended June 30,

2022 2021 2022 2021

(Millions, except for number of shares and per share data)

Operating Revenues

$ 1,794 $ 1,477 $ 3,927 $ 3,443

Operating Expenses

Purchased power, natural gas and fuel used

440 265 1,181 766

Operations and maintenance

693 676 1,344 1,318

Depreciation and amortization

271 250 532 497

Taxes other than income taxes

169 155 347 325

Total Operating Expenses

1,573 1,346 3,404 2,906

Operating Income

221 131 523 537

Other Income and (Expense)

Other income

9 34 20 35

Earnings from equity method investments

6 4 259 5

Interest expense, net of capitalization

(79) (75) (150) (148)

Income Before Income Tax

157 94 652 429

Income tax expense (benefit)

(4) 10 64 24

Net Income

161 84 588 405

Net loss attributable to noncontrolling interests 23 14 41 27

Net Income Attributable to Avangrid, Inc.

$ 184 $ 98 $ 629 $ 432

Earnings Per Common Share, Basic

$ 0.48 $ 0.28 $ 1.63 $ 1.31

Earnings Per Common Share, Diluted

$ 0.48 $ 0.28 $ 1.62 $ 1.31

Weighted-average Number of Common Shares

Outstanding:

Basic

386,736,774 347,121,197 386,717,560 328,412,163

Diluted

387,219,348 347,419,064 387,166,378 328,795,944

The accompanying notes are an integral part of our condensed consolidated financial statements.

5

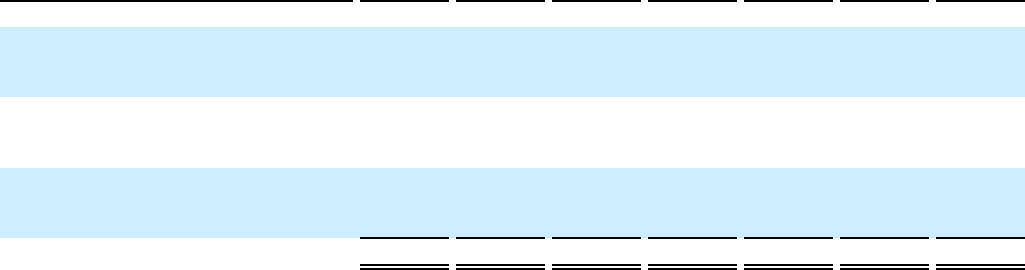

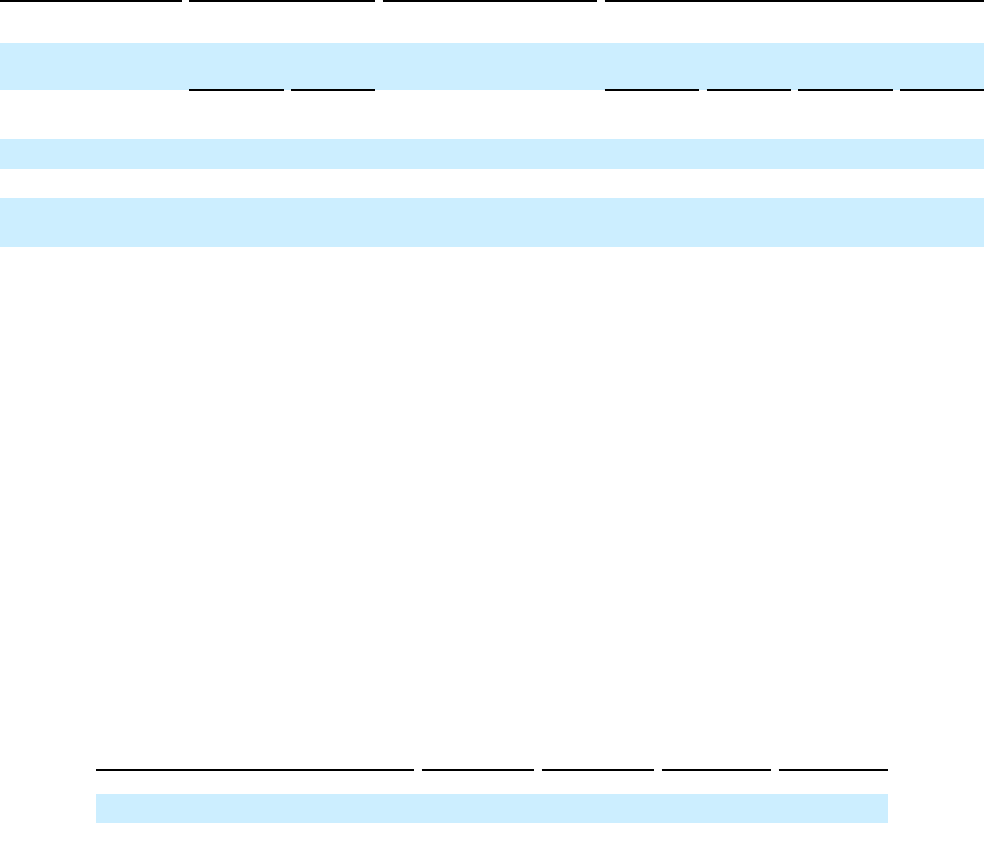

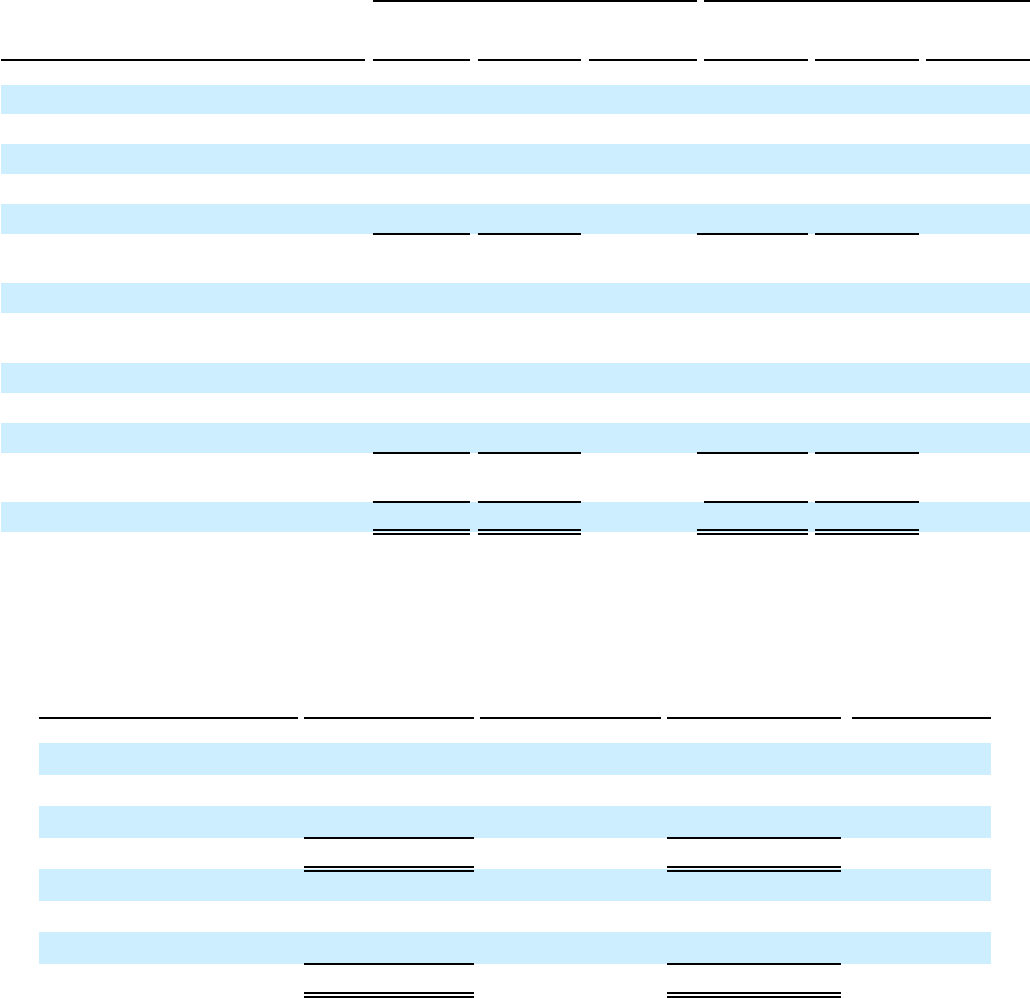

Avangrid, Inc. and Subsidiaries

Condensed Consolidated Statements of Comprehensive Income

(unaudited)

Three Months Ended June 30, Six Months Ended June 30,

2022 2021 2022 2021

(Millions)

Net Income

$ 161 $ 84 $ 588 $ 405

Other Comprehensive Income (Loss)

Loss on nonqualified pension plans, net of income tax of $3

for the six months ended — — 9 —

Unrealized (loss) gain from equity method investment, net of

income taxes of $(1) and $(4) for the three months ended,

respectively, and $4 and $(4)for the six months ended,

respectively (4) (3) 11 (3)

Unrealized (loss) gain during the period on derivatives

qualifying as cash flow hedges, net of income taxes of $15

and $(21) for the three months ended, respectively, and $0

and $(26) for the six months ended, respectively 39 (73) — (100)

Reclassification to net income of losses on cash flow hedges,

net of income taxes $2 and $(3) for the three months ended,

respectively, and $6 and $(4) for the six months ended,

respectively 6 4 17 5

Other Comprehensive Income (Loss)

41 (72) 37 (98)

Comprehensive Income 202 12 625 307

Net loss attributable to noncontrolling interests 23 14 41 27

Comprehensive Income Attributable to Avangrid, Inc.

$ 225 $ 26 $ 666 $ 334

The accompanying notes are an integral part of our condensed consolidated financial statements.

6

Avangrid, Inc. and Subsidiaries

Condensed Consolidated Balance Sheets

(unaudited)

June 30, December 31,

As of 2022 2021

(Millions)

Assets

Current Assets

Cash and cash equivalents

$ 411 $ 1,474

Accounts receivable and unbilled revenues, net

1,319 1,269

Accounts receivable from affiliates

2 11

Derivative assets

118 35

Fuel and gas in storage

171 139

Materials and supplies

225 204

Prepayments and other current assets

380 245

Regulatory assets

363 400

Total Current Assets

2,989 3,777

Total Property, Plant and Equipment ($2,686 and $1,959 related to VIEs,

respectively) 30,063 28,866

Operating lease right-of-use assets

151 148

Equity method investments

431 560

Other investments

49 61

Regulatory assets

2,153 2,247

Other Assets

Goodwill

3,119 3,119

Intangible assets

285 293

Derivative assets

109 59

Other

403 374

Total Other Assets

3,916 3,845

Total Assets

$ 39,752 $ 39,504

The accompanying notes are an integral part of our condensed consolidated financial statements.

7

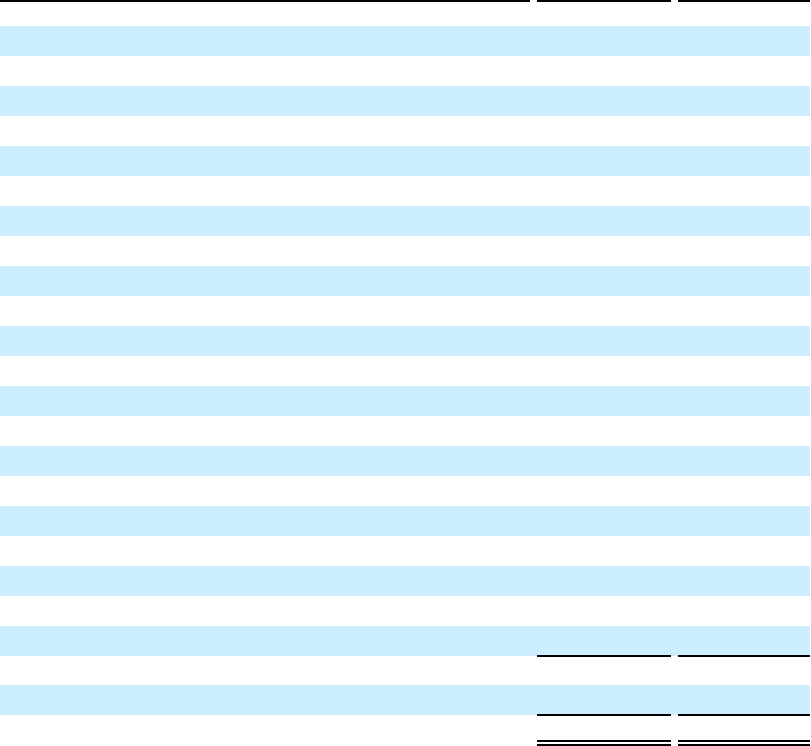

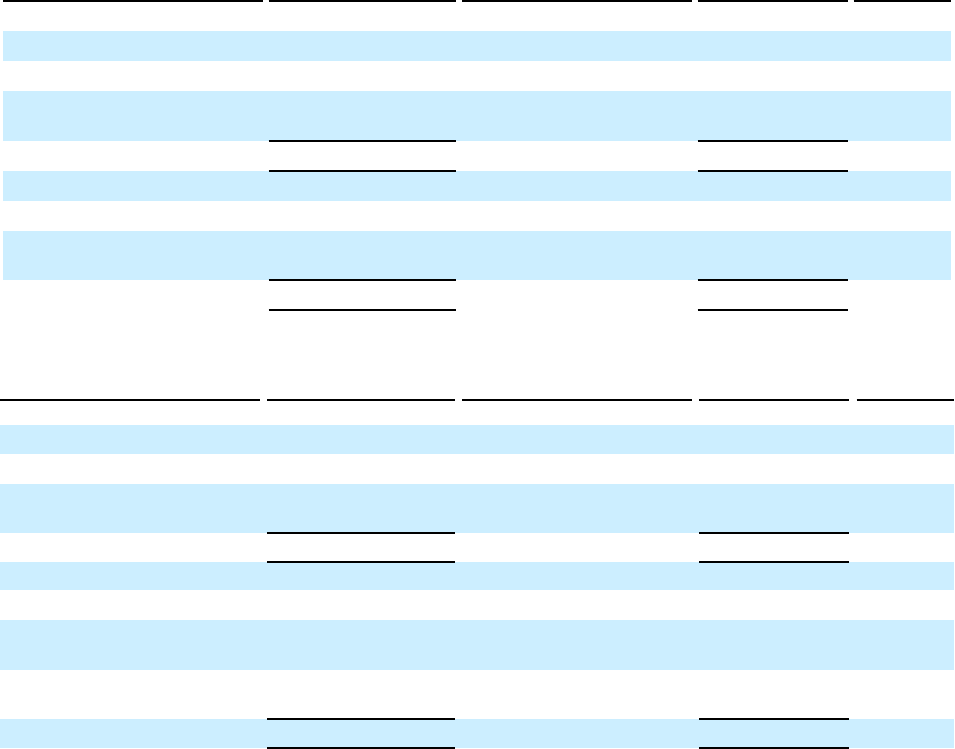

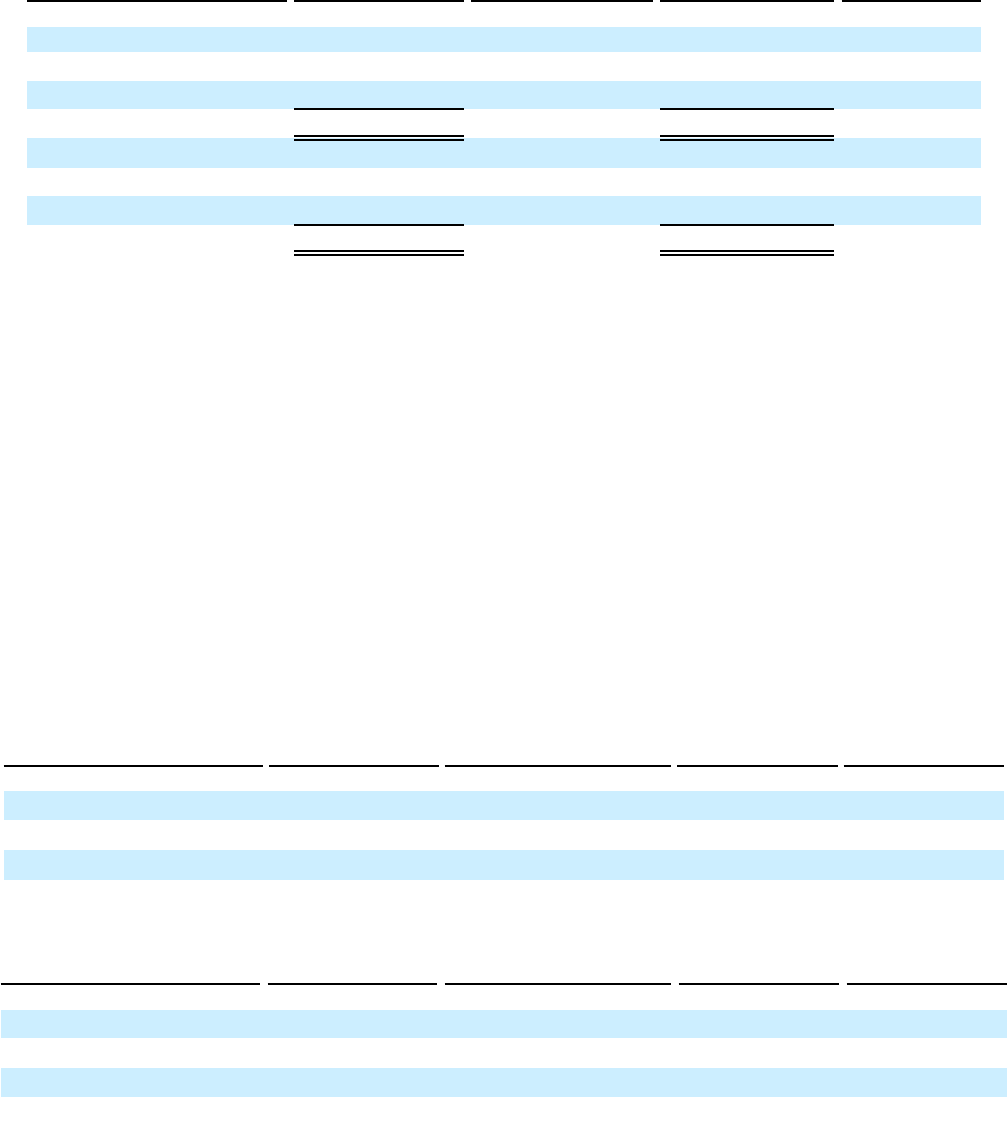

Avangrid, Inc. and Subsidiaries

Condensed Consolidated Balance Sheets

(unaudited)

June 30, December 31,

As of 2022 2021

(Millions, except share information)

Liabilities

Current Liabilities

Current portion of debt

$ 350 $ 372

Notes payable

92 159

Notes payable to affiliates

1 2

Interest accrued

67 69

Accounts payable and accrued liabilities

1,352 1,586

Accounts payable to affiliates

29 61

Dividends payable

170 170

Taxes accrued

63 43

Operating lease liabilities

11 12

Derivative liabilities

114 64

Other current liabilities

650 484

Regulatory liabilities

447 307

Total Current Liabilities

3,346 3,329

Regulatory liabilities

2,972 3,022

Other Non-current Liabilities

Deferred income taxes

2,179 2,016

Deferred income

1,096 1,130

Pension and other postretirement

457 684

Operating lease liabilities

132 149

Derivative liabilities

181 160

Asset retirement obligations

262 253

Environmental remediation costs

283 298

Other

570 580

Total Other Non-current Liabilities

5,160 5,270

Non-current debt

7,888 7,922

Total Non-current Liabilities

16,020 16,214

Total Liabilities

19,366 19,543

Commitments and Contingencies

Equity

Stockholders’ Equity:

Common stock, $.01 par value, 500,000,000 shares authorized, 387,734,757 and

387,678,630 shares issued; 386,624,231 and 386,568,104 shares outstanding,

respectively 3 3

Additional paid in capital

17,687 17,679

Treasury stock

(47) (47)

Retained earnings

2,003 1,714

Accumulated other comprehensive loss

(236) (273)

Total Stockholders’ Equity

19,410 19,076

Non-controlling interests

976 885

Total Equity

20,386 19,961

Total Liabilities and Equity

$ 39,752 $ 39,504

The accompanying notes are an integral part of our condensed consolidated financial statements.

8

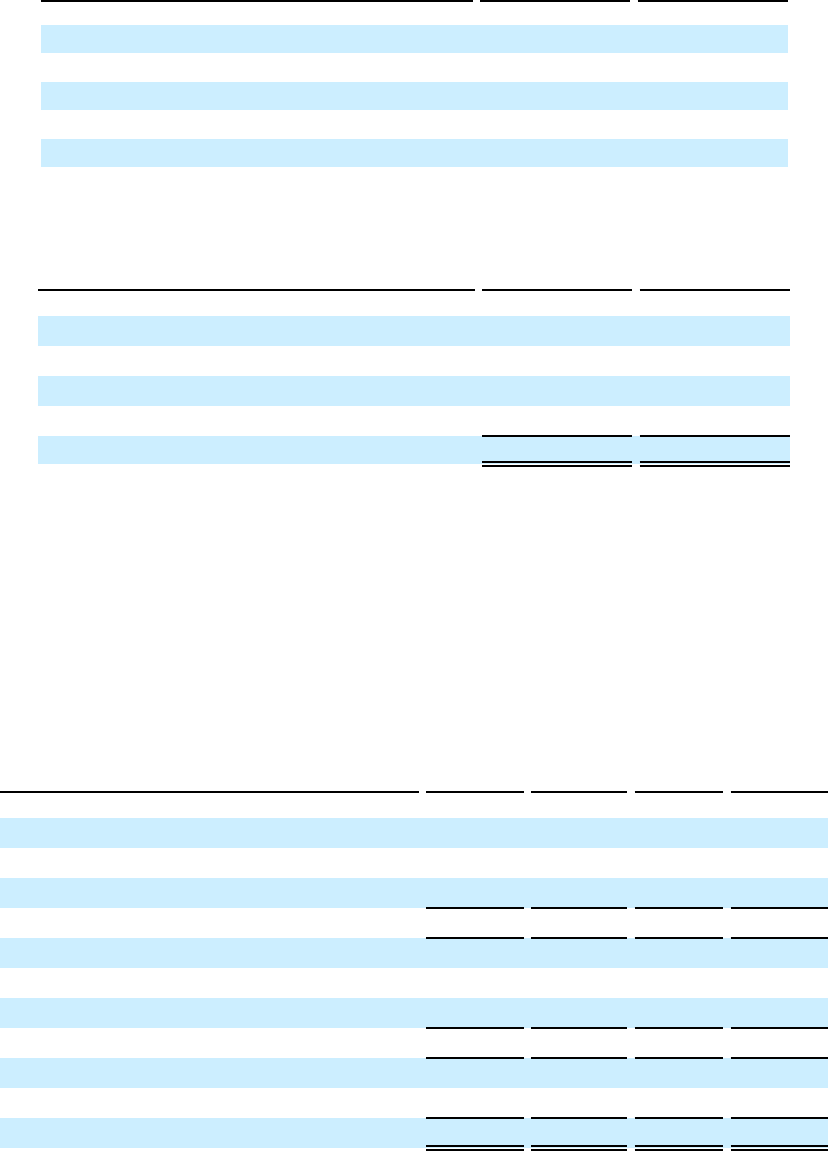

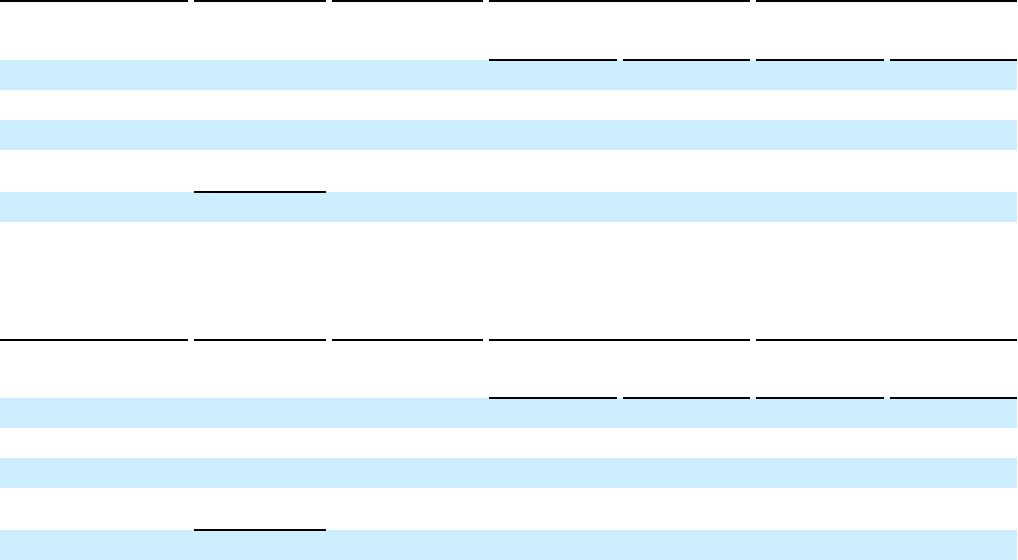

Avangrid, Inc. and Subsidiaries

Condensed Consolidated Statements of Cash Flows

(unaudited)

Six Months Ended June 30,

2022 2021

(Millions)

Cash Flow from Operating Activities:

Net income $ 588 $ 405

Adjustments to reconcile net income to net cash provided by operating activities:

Depreciation and amortization 532 497

Regulatory assets/liabilities amortization and carrying cost 3 34

Pension cost (12) 23

Earnings from equity method investments (259) (5)

Distributions of earnings received from equity method investments 13 9

Unrealized loss (gain) on marked-to-market derivative contracts (5) 74

Deferred taxes 58 45

Other non-cash items (12) (19)

Changes in operating assets and liabilities:

Current assets (208) 19

Noncurrent assets (289) (129)

Current liabilities 199 (11)

Noncurrent liabilities 197 (91)

Net Cash Provided by Operating Activities 805 851

Cash Flow from Investing Activities:

Capital expenditures (1,403) (1,264)

Contributions in aid of construction 80 21

Proceeds from sale of assets 9 5

Proceeds from notes receivable from affiliates (1) 2

Distributions received from equity method investments 2 4

Other investments and equity method investments, net (179) 231

Net Cash Used in Investing Activities (1,492) (1,001)

Cash Flow from Financing Activities:

Non-current debt issuances 216 —

Repayments of non-current debt (214) (2)

Repayment of non-current debt with affiliate — (3,000)

Repayments of other short-term debt, net (162) (307)

Repayments of financing leases (7) (4)

Repurchase of common stock — (2)

Issuance of common stock (1) 3,998

Distributions to noncontrolling interests (6) (5)

Contributions from noncontrolling interests 138 10

Dividends paid (340) (272)

Net Cash (Used in) Provided by Financing Activities (376) 416

Net (Decrease) Increase in Cash, Cash Equivalents and Restricted Cash (1,063) 266

Cash, Cash Equivalents and Restricted Cash, Beginning of Period 1,477 1,467

Cash, Cash Equivalents and Restricted Cash, End of Period $ 414 $ 1,733

Supplemental Cash Flow Information

Cash paid for interest, net of amounts capitalized $ 144 $ 143

Cash paid for income taxes $ 10 $ 5

The accompanying notes are an integral part of our condensed consolidated financial statements.

9

Avangrid, Inc. and Subsidiaries

Condensed Consolidated Statements of Changes in Equity

(unaudited)

Avangrid, Inc. Stockholders

(Millions, except for number of shares )

Number of

shares (*)

Common

Stock

Additional

paid-in

capital

Treasury

Stock

Retained

Earnings

Accumulated

Other

Comprehensive

Loss

Total

Stockholders’

Equity

Noncontrolling

Interests Total

As of March 31, 2021 309,369,894 $ 3 $ 13,667 $ (16) $ 1,864 $ (137) $ 15,381 $ 611 $ 15,992

Net income (loss) — — — — 98 — 98 (14) 84

Other comprehensive income, net of tax of $(28) — — — — — (72) (72) — (72)

Comprehensive income 12

Dividends declared, $0.44/share — — — — (171) — (171) — (171)

Release of common stock held in trust 4,260 — — — — — — — —

Issuance of common stock 77,830,402 — 3,999 — — — 3,999 — 3,999

Stock-based compensation — — 5 — — — 5 — 5

Distributions to noncontrolling interests — — — — — — — (2) (2)

Contributions from noncontrolling interests — — — — (1) — (1) 1 —

As of June 30, 2021 387,204,556 $ 3 $ 17,671 $ (16) $ 1,790 $ (209) $ 19,239 $ 596 $ 19,835

As of March 31, 2022 386,624,231 $ 3 $ 17,683 $ (47) $ 1,819 $ (277) $ 19,181 $ 879 $ 20,060

Net income (loss) — — — — 184 — 184 (23) 161

Other comprehensive income, net of tax of $16 — — — — — 41 41 — 41

Comprehensive income 202

Dividends declared, $0.44/share — — — — — — — — —

Stock-based compensation — — 4 — — — 4 — 4

Distributions to noncontrolling interests — — — — — — — (5) (5)

Contributions from noncontrolling interests — — — — — — — 125 125

As of June 30, 2022 386,624,231 $ 3 $ 17,687 $ (47) $ 2,003 $ (236) $ 19,410 $ 976 $ 20,386

10

Avangrid, Inc. Stockholders

(Millions, except for number of shares )

Number of

shares (*)

Common

Stock

Additional

paid-in

capital

Treasury

Stock

Retained

Earnings

Accumulated

Other

Comprehensive

Loss

Total

Stockholders’

Equity

Noncontrolling

Interests Total

As of December 31, 2020 309,077,300 $ 3 $ 13,665 $ (14) $ 1,666 $ (111) $ 15,209 $ 617 $ 15,826

Net income (loss) — — — — 432 — 432 (27) 405

Other comprehensive loss, net of tax of $(34) — — — — — (98) (98) — (98)

Comprehensive income 307

Dividends declared, $0.88/share — — — — (307) — (307) — (307)

Release of common stock held in trust 296,854 — — — — — — — —

Issuance of common stock 77,883,713 — 3,998 — — — 3,998 — 3,998

Repurchase of common stock (53,311) — — (2) — — (2) — (2)

Stock-based compensation — — 8 — — — 8 — 8

Distributions to noncontrolling interests — — — — — — — (5) (5)

Contributions from noncontrolling interests — — — — (1) — (1) 11 10

As of June 30, 2021 387,204,556 $ 3 $ 17,671 $ (16) $ 1,790 $ (209) $ 19,239 $ 596 $ 19,835

As of December 31, 2021 386,568,104 $ 3 $ 17,679 $ (47) $ 1,714 $ (273) $ 19,076 $ 885 $ 19,961

Net income (loss) — — — — 629 — 629 (41) 588

Other comprehensive loss, net of tax of $13 — — — — — 37 37 — 37

Comprehensive income 625

Dividends declared, $0.88/share — — — — (340) — (340) — (340)

Issuance of common stock 56,127 — (1) — — — (1) — (1)

Stock-based compensation — — 9 — — — 9 — 9

Distributions to noncontrolling interests — — — — — — — (6) (6)

Contributions from noncontrolling interests — — — — — — 138 138

As of June 30, 2022 386,624,231 $ 3 $ 17,687 $ (47) $ 2,003 $ (236) $ 19,410 $ 976 $ 20,386

(*) Par value of share amounts is $0.01

The accompanying notes are an integral part of our condensed consolidated financial statements.

11

Avangrid, Inc. and Subsidiaries

Notes to Condensed Consolidated Financial Statements

(unaudited)

Note 1. Background and Nature of Operations

Avangrid, Inc. (AVANGRID, we or the Company) is an energy services holding company engaged in the regulated energy

transmission and distribution business through its principal subsidiary, Avangrid Networks, Inc. (Networks), and in the

renewable energy generation business through its principal subsidiary, Avangrid Renewables Holding, Inc. (ARHI). ARHI in

turn holds subsidiaries including Avangrid Renewables, LLC (Renewables). Iberdrola, S.A. (Iberdrola), a corporation organized

under the laws of the Kingdom of Spain, owns 81.6% of the outstanding common stock of AVANGRID. The remaining

outstanding shares are owned by various shareholders with approximately 18.4% of AVANGRID's outstanding shares publicly

traded on the New York Stock Exchange (NYSE).

Proposed Merger with PNMR

On October 20, 2020, AVANGRID, PNM Resources, Inc., a New Mexico corporation (PNMR) and NM Green Holdings, Inc.,

a New Mexico corporation and wholly-owned subsidiary of AVANGRID (Merger Sub), entered into an Agreement and Plan of

Merger (Merger Agreement), pursuant to which Merger Sub is expected to merge with and into PNMR, with PNMR surviving

the Merger as a direct wholly-owned subsidiary of AVANGRID (Merger). Pursuant to the Merger Agreement, each issued and

outstanding share of the common stock of PNMR (PNMR common stock) (other than (i) the issued shares of PNMR common

stock that are owned by AVANGRID, Merger Sub, PNMR or any wholly-owned subsidiary of AVANGRID or PNMR, which

will be automatically cancelled at the time the Merger is consummated and (ii) shares of PNMR common stock held by a holder

who has not voted in favor of, or consented in writing to, the Merger who is entitled to, and who has demanded, payment for

fair value of such shares) will be converted, at the time the Merger is consummated, into the right to receive $50.30 in cash

(Merger Consideration).

Consummation of the Merger (Closing) is subject to the satisfaction or waiver of certain customary closing conditions,

including, without limitation, the approval of the Merger Agreement by the holders of at least a majority of the outstanding

shares of PNMR common stock entitled to vote thereon, the absence of any material adverse effect on PNMR, the receipt of

certain required regulatory approvals (including approvals from the Public Utility Commission of Texas (PUCT), the New

Mexico Public Regulation Commission (NMPRC), the Federal Energy Regulatory Commission (FERC), the Federal

Communications Commission (FCC), the Committee on Foreign Investment in the United States (CFIUS), the Nuclear

Regulatory Commission (NRC) and approval under the Hart-Scott-Rodino Antitrust Improvements Act of 1976), the Four

Corners Divestiture Agreements (as defined below) being in full force and effect and all applicable regulatory filings associated

therewith being made, as well as holders of no more than 15% of the outstanding shares of PNMR common stock validly

exercising their dissenters’ rights. On February 12, 2021, the shareholders of PNMR approved the proposed Merger. As of

November 1, the Merger had obtained all regulatory approvals other than from the NMPRC. On November 1, 2021, after public

hearing and briefing on the matter, the hearing examiner in the Merger proceeding at the NMPRC issued an unfavorable

recommendation related to the amended stipulated agreement entered into by PNMR, AVANGRID and several interveners in

the NMPRC proceeding with respect to consideration of the joint Merger application in June 2021. On December 8, 2021, the

NMPRC issued an order rejecting the amended stipulated agreement. On January 3, 2022, AVANGRID and PNMR filed a

notice of appeal of the December 8, 2021 decision of the NMPRC with the New Mexico Supreme Court. The Statement of

Issues was filed on February 2, 2022 and the Brief in Chief was filed on April 7, 2022. On June 14, 2022, the NMPRC filed its

Answer Brief. On June 13, 2022, New Energy Economy, an intervener in the Merger proceeding, filed its Answer Brief.

AVANGRID's Reply Brief is due on August 5, 2022 (pending any additional extensions granted to the parties). On February

24, 2022, the FCC granted an extension to its approval to transfer operating licenses in connection with the Merger.

In addition, on January 3, 2022, AVANGRID, PNMR and Merger Sub entered into an Amendment to the Merger Agreement

(the Amendment), pursuant to which AVANGRID, PNMR and Merger Sub each agreed to extend the “End Date” for

consummation of the Merger until April 20, 2023. The parties acknowledge in the Amendment that the required regulatory

approval from the NMPRC has not been obtained and that the parties have reasonably determined that such outstanding

approval will not be obtained by April 20, 2022. In light of this outstanding approval, the parties determined to approve the

Amendment. As amended, the Merger Agreement may be terminated by each of AVANGRID and PNMR under certain

circumstances, including if the Merger is not consummated by April 20, 2023 (subject to a three-month extension by

AVANGRID and PNMR by mutual consent if all of the conditions to the closing, other than the conditions related to obtaining

regulatory approvals, have been satisfied or waived). During the pendency of this appeal certain required regulatory approvals

and consents may expire and AVANGRID and PNMR will reapply and/or apply for extensions of such approvals, as the case

may be. We cannot predict the outcome of this proceeding for the outstanding approvals.

12

The Merger Agreement contains representations, warranties and covenants of PNMR, AVANGRID and Merger Sub, which are

customary for transactions of this type. In addition, among other things, the Merger Agreement contains a covenant requiring

PNMR to, prior to the closing, enter into agreements (Four Corners Divestiture Agreements) providing for, and to make filings

required to, exit from all ownership interests in the Four Corners Power Plant, all with the objective of having the closing date

for such exit be no later than December 31, 2024.

The Merger Agreement (as amended) provides for certain customary termination rights including the right of either party to

terminate the Merger Agreement if the Merger is not completed on or before April 20, 2023 (subject to a three-month extension

by AVANGRID and PNMR by mutual consent if all of the conditions to the closing, other than the conditions related to

obtaining regulatory approvals, have been satisfied or waived). The Merger Agreement further provides that, upon termination

of the Merger Agreement under certain specified circumstances (including if AVANGRID terminates the Merger Agreement

due to a change in recommendation of the board of directors of PNMR or if PNMR terminates the Merger Agreement to accept

a superior proposal (as defined in the Merger Agreement)), PNMR will be required to pay AVANGRID a termination fee of

$130 million. In addition, the Merger Agreement provides that (i) if the Merger Agreement is terminated by either party due to

a failure of a regulatory closing condition and such failure is the result of AVANGRID’s breach of its regulatory covenants, or

(ii) AVANGRID fails to effect the Closing when all closing conditions have been satisfied and it is otherwise obligated to do so

under the Merger Agreement, then, in either such case, upon termination of the Merger Agreement, AVANGRID will be

required to pay PNMR a termination fee of $184 million as the sole and exclusive remedy. Upon the termination of the Merger

Agreement under certain specified circumstances involving a breach of the Merger Agreement, either PNMR or AVANGRID

will be required to reimburse the other party’s reasonable and documented out-of-pocket fees and expenses up to $10 million

(which amount will be credited toward, and offset against, the payment of any applicable termination fee).

In connection with the Merger, Iberdrola has provided AVANGRID a commitment letter (Iberdrola Funding Commitment

Letter), pursuant to which Iberdrola has unilaterally agreed to provide to AVANGRID, or arrange the provision to AVANGRID

of, funds to the extent necessary for AVANGRID to consummate the Merger, including the payment of the aggregate Merger

Consideration.

On April 15, 2021, AVANGRID entered into a side letter agreement with Iberdrola, which sets forth certain terms and

conditions relating to the Iberdrola Funding Commitment Letter (the Side Letter Agreement). The Side Letter Agreement

provides that any drawing in the form of indebtedness made by the Corporation pursuant to the Funding Commitment Letter

shall bear interest at an interest rate equal to 3-month LIBOR plus 0.75% per annum calculated on the basis of a 360-day year

for the actual number of days elapsed and, commencing on the date of the Funding Commitment Letter, we shall pay Iberdrola

a facility fee equal to 0.12% per annum on the undrawn portion of the funding commitment set forth in the Funding

Commitment Letter.

On May 18, 2021, we issued 77,821,012 shares of common stock in two private placements. Iberdrola purchased 63,424,125

shares and Hyde Member LLC, a Delaware limited liability company and a wholly owned subsidiary of Qatar Investment

Authority, purchased 14,396,887 shares of our common stock, par value $0.01 per share, at the purchase price of $51.40 per

share, which was the closing price of the shares of our common stock on the NYSE as of May 11, 2021. Proceeds of the private

placements were $4,000 million. $3,000 million of the proceeds were used to repay the Iberdrola Loan. After the effect of the

private placements, Iberdrola retained its 81.6% ownership interest in AVANGRID.

Note 2. Basis of Presentation

The accompanying condensed consolidated financial statements should be read in conjunction with the Form 10-K for the fiscal

year ended December 31, 2021.

The accompanying unaudited financial statements are prepared on a consolidated basis and include the accounts of

AVANGRID and its consolidated subsidiaries, Networks and ARHI. All intercompany transactions and accounts have been

eliminated in consolidation. The year-end balance sheet data was derived from audited financial statements. The unaudited

condensed consolidated financial statements for the interim periods have been prepared in accordance with accounting

principles generally accepted in the United States of America (U.S. GAAP) for interim financial information and with the

instructions to Form 10-Q and Article 10 of Regulation S-X. Accordingly, the interim condensed consolidated financial

statements do not include all the information and note disclosures required by U.S. GAAP for complete financial statements.

In the opinion of management, the accompanying condensed consolidated financial statements contain all adjustments

necessary to present fairly our condensed consolidated financial statements for the interim periods described herein. All such

adjustments are of a normal and recurring nature, except as otherwise disclosed. The results for the three and six months ended

June 30, 2022, are not necessarily indicative of the results for the entire fiscal year ending December 31, 2022.

13

Note 3. Significant Accounting Policies and New Accounting Pronouncements

The new accounting pronouncements we have adopted as of January 1, 2022, and reflected in our condensed consolidated

financial statements are described below. There have been no other material changes to the significant accounting policies

described in our Form 10-K for the fiscal year ended December 31, 2021, except for those described below resulting from the

adoption of new authoritative accounting guidance issued by the Financial Accounting Standards Board (FASB).

Adoption of New Accounting Pronouncements

(a) Facilitation of the effects of reference rate reform on financial reporting, and subsequent scope clarification

In March 2020, the FASB issued amendments and created ASC 848 to provide temporary optional guidance to entities to ease

the potential burden in accounting for, or recognizing the effects of, reference rate reform on financial reporting. The

amendments respond to concerns about structural risks of interbank offered rates, and particularly, the risk of cessation of the

London Interbank Offered Rate (LIBOR). The guidance is elective and applies to all entities, subject to meeting certain criteria,

that have contracts, hedging relationships, and other transactions that reference LIBOR or another reference rate expected to be

discontinued due to reference rate reform, around the end of 2021. The guidance applies to contracts that have modified terms

that affect, or have the potential to affect, the amount or timing of contractual cash flows resulting from the discontinuance of

the reference rate reform. The amendments are effective for all entities as of March 12, 2020, through December 31, 2022,

although the FASB has indicated it will monitor developments in the marketplace and consider whether developments warrant

an extension.

In January 2021, the FASB issued amendments to clarify the scope of ASC 848 and respond to questions from stakeholders

about whether ASC 848 can be applied to derivative instruments that do not reference a rate that is expected to be discontinued

but that use an interest rate for margining, discounting, or contract price alignment that is modified because of reference rate

reform. The modification, commonly referred to as the “discounting transition,” may have accounting implications, raising

concerns about the need to reassess previous accounting determinations related to those derivatives and about the possible

hedge accounting consequences of the discounting transition. The amendments clarify that certain optional expedients and

exceptions in ASC 848 for contract modifications and hedge accounting apply to derivatives that are affected by the discounting

transition, capture the incremental consequences of the scope clarification and tailor the existing guidance to derivative

instruments affected by the discounting transition. The amendments are effective immediately, and may be elected

retrospectively to eligible modifications as of any date from the beginning of the interim period that includes March 12, 2020,

or prospectively to new modifications made on or after any date within the interim period that includes January 7, 2021.

We expect our adoption of reference rate reform and the subsequent scope clarification will not materially affect our

consolidated results of operations, financial position and cash flows.

(b) Disclosures by business entities about government assistance

In November 2021, the FASB issued amendments that apply to business entities (all entities except specified not-for-profit

entities and employee benefit plans) that account for a transaction with a government by applying a grant or contribution

accounting model by analogy to other accounting guidance (such as a grant model within International Accounting Standards

20 Accounting for Government Grants and Disclosure of Government Assistance, or ASC Subtopic 958-605, Not-For-Profit

Entities—Revenue Recognition). Government assistance can include tax credits (excluding transactions within the scope of

Topic 740, Income Taxes), cash grants, grants of other assets, and project grants. Often, government assistance is provided to

an entity for a particular purpose, and the entity promises to take specific actions. Transactions with a government, as used in

ASC 832, Government Assistance, include assistance administered by domestic, foreign, local (city, town, county, municipal),

regional (state, provincial, territorial), and national (federal) governments and entities related to those governments. The

amendments require annual disclosures in notes to financial statements about transactions with a government as follows: (1)

information about the nature of the transactions and the related accounting policy used to account for the transactions, (2) the

line items on the balance sheet and income statement affected by the transactions, and the amounts applicable to each financial

statement line item, and (3) significant terms and conditions of the transactions, including commitments and contingencies. For

entities within scope the amendments are effective for annual periods beginning after December 15, 2021, with early

application permitted. The amendments are to be applied either (1) prospectively to transactions within the scope of the

amendments that are reflected in financial statements at the date of initial application and new transactions that are entered into

after the date of initial application or (2) retrospectively to those transactions. Our adoption of the amendments on January 1,

2022 did not materially affect our disclosures.

Accounting Pronouncements Issued but Not Yet Adopted

The following are new accounting pronouncements not yet adopted, including those issued since December 31, 2021, that we

have evaluated or are evaluating to determine their effect on our condensed consolidated financial statements.

14

(a) Troubled Debt Restructurings and Vintage Disclosures

In March 2022, the FASB issued amendments to ASC 326 to provide guidance for troubled debt restructurings (TDRs) and

vintage disclosures. For TDRs, the update requires entities to measure and record lifetime expected credit losses on an asset that

is within scope of Topic 326. The prior guidance in Topic 310 of designating a loan as a TDR was considered unnecessarily

complex. For vintage disclosures, the amendments require an entity to disclose current-period gross write-offs by year of

origination for financing receivables and net investments in leases within the scope of Subtopic 326-20.

The amendments are effective for fiscal years beginning after December 15, 2022, including interim periods within those fiscal

years. The amendments should be applied prospectively, except as provided in the next sentence. For the transition method

related to the recognition of TDRs, an entity has the option to apply a modified retrospective transition method, resulting in a

cumulative-effect adjustment to retained earnings in the period of adoption. Early adoption is permitted.

We expect our adoption will not materially affect our consolidated results of operations, financial position and cash flows.

Note 4. Revenue

We recognize revenue when we have satisfied our obligations under the terms of a contract with a customer, which generally

occurs when the control of promised goods or services transfers to the customer. We measure revenue as the amount of

consideration we expect to receive in exchange for providing those goods or services. Contracts with customers may include

multiple performance obligations. For such contracts, we allocate revenue to each performance obligation based on its relative

standalone selling price. We generally determine standalone selling prices based on the prices charged to customers. Certain

revenues are not within the scope of ASC 606, such as revenues from leasing, derivatives, other revenues that are not from

contracts with customers and other contractual rights or obligations, and we account for such revenues in accordance with the

applicable accounting standards. We exclude from revenue amounts collected on behalf of third parties, including any such

taxes collected from customers and remitted to governmental authorities. We do not have any significant payment terms that are

material because we receive payment at or shortly after the point of sale.

The following describes the principal activities, by reportable segment, from which we generate revenue. For more detailed

information about our reportable segments, refer to Note 13.

Networks Segment

Networks derives its revenue primarily from tariff-based sales of electricity and natural gas service to customers in New York,

Connecticut, Maine and Massachusetts, with no defined contractual term. For such revenues, we recognize revenues in an

amount derived from the commodities delivered to customers. Other major sources of revenue are electricity transmission and

wholesale sales of electricity and natural gas.

Tariff-based sales are subject to the corresponding state regulatory authorities, which determine prices and other terms of

service through the ratemaking process. The applicable tariffs are based on the cost of providing service. The utilities’ approved

base rates are designed to recover their allowable operating costs, including energy costs, finance costs, and the costs of equity,

the last of which reflect our capital ratio and a reasonable return on equity. We traditionally invoice our customers by applying

approved base rates to usage. Maine state law prohibits the utility from providing the electricity commodity to customers. In

New York, Connecticut and Massachusetts, customers have the option to obtain the electricity or natural gas commodity

directly from the utility or from another supplier. For customers that receive their commodity from another supplier, the utility

acts as an agent and delivers the electricity or natural gas provided by that supplier. Revenue in those cases is only for providing

the service of delivery of the commodity.

Transmission revenue results from others’ use of the utility’s transmission system to transmit electricity and is subject to FERC

regulation, which establishes the prices and other terms of service. Long-term wholesale sales of electricity are based on

individual bilateral contracts. Short-term wholesale sales of electricity are generally on a daily basis based on market prices and

are administered by the Independent System Operator-New England (ISO-NE) and the New York Independent System

Operator (NYISO) or PJM Interconnection, L.L.C. (PJM), as applicable. Wholesale sales of natural gas are generally short-term

based on market prices through contracts with the specific customer.

The performance obligation in all arrangements is satisfied over time because the customer simultaneously receives and

consumes the benefits as Networks delivers or sells the electricity or natural gas or provides the delivery or transmission

service.

Certain Networks entities record revenue from Alternative Revenue Programs (ARPs), which is not ASC 606 revenue. Such

programs represent contracts between the utilities and their regulators. The Networks ARPs include revenue decoupling

15

mechanisms (RDMs), other ratemaking mechanisms, annual revenue requirement reconciliations and other demand side

management programs.

Networks also has various other sources of revenue including billing, collection, other administrative charges, sundry billings,

rent of utility property and miscellaneous revenue. It classifies such revenues as other ASC 606 revenues to the extent they are

not related to revenue generating activities from leasing, derivatives or ARPs.

Renewables Segment

Renewables derives its revenue primarily from the sale of energy, transmission, capacity and other related charges from its

renewable wind, solar and thermal energy generating sources. For such revenues, we will recognize revenues in an amount

derived from the commodities delivered and from services as they are made available. Renewables has bundled power purchase

agreements consisting of electric energy, transmission, capacity and/or renewable energy credits (RECs). The related contracts

are generally long-term with no stated contract amount, that is, the customer is entitled to all or a percentage of the unit’s

output. Renewables also has unbundled sales of electric energy and capacity, RECs and natural gas, which are generally for

periods of less than a year. The performance obligations in substantially all of both bundled and unbundled arrangements for

electricity and natural gas are satisfied over time, for which we record revenue based on the amount invoiced to the customer

for the actual energy delivered. The performance obligation for stand-alone RECs is satisfied at a point in time, for which we

record revenue when the performance obligation is satisfied upon delivery of the REC.

Renewables classifies certain contracts for the sale of electricity as derivatives, in accordance with the applicable accounting

standards. Renewables also has revenue from its energy trading operations, which it generally classifies as derivative revenue.

However, trading contracts not classified as derivatives are within the scope of ASC 606, with the performance obligation of

the delivery of energy (electricity, natural gas) and settlement of the contracts satisfied at a point in time at which time we

recognize the revenue. Renewables also has other ASC 606 revenue, which we recognize based on the amount invoiced to the

customer.

Other

Other, which does not represent a segment, includes miscellaneous Corporate revenues and intersegment eliminations.

Contract Costs and Contract Liabilities

We recognize an asset for incremental costs of obtaining a contract with a customer when we expect the benefit of those costs

to be longer than one year. We have contract assets for costs from development success fees, which we paid during the solar

asset development period in 2018, and will amortize ratably into expense over the 15-year life of the power purchase agreement

(PPA), expected to commence in December 2022 upon commercial operation. Contract assets totaled $9 million at both

June 30, 2022 and December 31, 2021, and are presented in "Other non-current assets" on our condensed consolidated balance

sheets.

We have contract liabilities for revenue from transmission congestion contract (TCC) auctions, for which we receive payment

at the beginning of an auction period, and amortize ratably each month into revenue over the applicable auction period. The

auction periods range from six months to two years. TCC contract liabilities totaled $14 million and $16 million at June 30,

2022 and December 31, 2021, respectively, and are presented in "Other current liabilities" on our condensed consolidated

balance sheets. We recognized $6 million and $14 million as revenue during the three and six months ended June 30, 2022,

respectively, and $5 million and $9 million for the three and six months ended June 30, 2021, respectively.

16

Revenues disaggregated by major source for our reportable segments for the three and six months ended June 30, 2022 and

2021 are as follows:

Three Months Ended June 30, 2022 Six Months Ended June 30, 2022

Networks Renewables Other (b) Total Networks Renewables Other (b) Total

(Millions)

Regulated operations –

electricity

$ 1,029 $ — $ — $ 1,029 $ 2,199 $ — $ — $ 2,199

Regulated operations –

natural gas

350 — — 350 1,071 — — 1,071

Nonregulated operations –

wind

— 277 — 277 — 497 — 497

Nonregulated operations –

solar

— 9 — 9 — 16 — 16

Nonregulated operations –

thermal

— 11 — 11 — 24 — 24

Other(a)

37 26 — 63 59 42 — 101

Revenue from contracts

with customers

1,416 323 — 1,739 3,329 579 — 3,908

Leasing revenue

1 — — 1 4 — — 4

Derivative revenue

— 5 — 5 — (58) — (58)

Alternative revenue programs

24 — — 24 36 — — 36

Other revenue

23 2 — 25 30 7 — 37

Total operating revenues

$ 1,464 $ 330 $ — $ 1,794 $ 3,399 $ 528 $ — $ 3,927

Three Months Ended June 30, 2021 Six Months Ended June 30, 2021

Networks Renewables Other (b) Total Networks Renewables Other (b) Total

(Millions)

Regulated operations –

electricity

$ 912 $ — $ — $ 912 $ 1,854 $ — $ — $ 1,854

Regulated operations –

natural gas

256 — — 256 820 — — 820

Nonregulated operations –

wind

— 243 — 243 — 614 — 614

Nonregulated operations –

solar

— 7 — 7 — 11 — 11

Nonregulated operations –

thermal

— 16 — 16 — 28 — 28

Other(a)

14 41 — 55 24 73 — 97

Revenue from contracts

with customers

1,182 307 — 1,489 2,698 726 — 3,424

Leasing revenue

3 — — 3 5 — — 5

Derivative revenue

— (63) — (63) — (94) — (94)

Alternative revenue

programs

22 — — 22 69 — — 69

Other revenue

12 14 — 26 20 19 — 39

Total operating revenues

$ 1,219 $ 258 $ — $ 1,477 $ 2,792 $ 651 $ — $ 3,443

(a) Primarily includes certain intra-month trading activities, billing, collection and administrative charges, sundry billings and

other miscellaneous revenue.

(b) Does not represent a segment. Includes Corporate and intersegment eliminations.

As of June 30, 2022 and December 31, 2021, accounts receivable balances related to contracts with customers were

approximately $1,228 million and $1,220 million, respectively, including unbilled revenues of $315 million and $405 million,

which are included in “Accounts receivable and unbilled revenues, net” on our condensed consolidated balance sheets.

17

As of June 30, 2022, the aggregate amount of the transaction price allocated to performance obligations that are unsatisfied (or

partially unsatisfied) were as follows:

As of June 30, 2022 2023 2024 2025 2026 2027 Thereafter Total

(Millions)

Revenue expected to be recognized on

multiyear retail energy sales contracts in

place $ 1 $ 1 $ — $ — $ — $ — $ 2

Revenue expected to be recognized on

multiyear capacity and carbon-free

energy sale contracts 60 14 12 10 7 60 163

Revenue expected to be recognized on

multiyear renewable energy credit sale

contracts 32 28 11 2 1 1 75

Total operating revenues

$ 93 $ 43 $ 23 $ 12 $ 8 $ 61 $ 240

As of June 30, 2022, the aggregate amount of the transaction price allocated to performance obligations that are unsatisfied (or

partially unsatisfied) for the remainder of 2022 was $39 million.

Note 5. Regulatory Assets and Liabilities

Pursuant to the requirements concerning accounting for regulated operations, our utilities capitalize, as regulatory assets,

incurred and accrued costs that are probable of recovery in future electric and natural gas rates. We base our assessment of

whether recovery is probable on the existence of regulatory orders that allow for recovery of certain costs over a specific period,

or allow for reconciliation or deferral of certain costs. When costs are not treated in a specific regulatory order, we use

regulatory precedent to determine if recovery is probable. Our operating utilities also record, as regulatory liabilities,

obligations to refund previously collected revenue or to spend revenue collected from customers on future costs. The primary

items that are not included in rate base or accruing carrying costs are regulatory assets for qualified pension and other

postretirement benefits, which reflect unrecognized actuarial gains and losses; debt premium; environmental remediation costs,

which are primarily the offset of accrued liabilities for future spending; unfunded future income taxes, which are the offset to

the unfunded future deferred income tax liability recorded; asset retirement obligations; hedge losses; and contracts for

differences. As of June 30, 2022, the total net amount of these items is approximately $888 million.

CMP Distribution Rate Case

In an order issued on February 19, 2020, the MPUC authorized an increase in CMP's distribution revenue requirement of

$17 million, or approximately 7.00%, based on an allowed ROE of 9.25% and a 50.00% equity ratio. The rate increase was

effective March 1, 2020. Commencing on March 1, 2020, the MPUC also imposed a 1.00% ROE reduction (to 8.25%) for

management efficiency associated with CMP’s customer service performance following the implementation of its new billing

system in 2017 which would be removed after demonstrating satisfactory customer service performance. In September 2021,

CMP met the 18-month required rolling average satisfactory customer service benchmarks and filed with the MPUC a request

for removal of the management efficiency adjustment, which was approved by the MPUC effective as of its February 18, 2022

order.

The order provided additional funding for staffing increases, vegetation management programs and storm restoration costs,

while retaining the basic tiered structure for storm cost recovery implemented in the 2014 stipulation. The MPUC order also

retained the RDM implemented in 2014. The order denied CMP’s request to increase rates for higher costs associated with

services provided by its affiliates and ordered the initiation of a management audit to evaluate whether CMP's current

management structure, and the management and other services from its affiliates, are appropriate and in the interest of Maine

customers. The management audit was commenced in July 2020 by the MPUC's consultants and culminated with a report

issued by the MPUC’s consultants in July 2021. On February 18, 2022, the MPUC opened a narrowly tailored follow-on

investigation examining how CMP and its customers are affected by decisions made at the CMP corporate parent level about

earnings, capital budgeting, and planning. In this context, the investigation will also examine regulatory approaches and

structures including ratemaking and performance mechanisms. We cannot predict the outcome of this investigation.

In accordance with Chapter 120 of MPUC Rules, on May 26, 2022, CMP filed a nonbinding notice of intent to file a

distribution rate case on or after sixty days from the issuance of the letter. In the notice, CMP signaled its intent to propose a

three-year rate plan, which includes a multi-year capital investment plan to fund investments needed to improve reliability and

resiliency, as well as to continue to improve the customer experience and cost-effectively advance clean energy transformation.

CMP’s notice estimated a revenue change in the range of $45 to $50 million in the first year of the rate plan followed by

18

increases in the range of $25 to $30 million in the second year and $20 to $25 million in the third year. We cannot predict the

outcome of this matter.

NYSEG and RG&E Rate Plans

On November 19, 2020, the NYPSC approved a new three-year rate plan for NYSEG & RG&E (2020 Joint Proposal), with

modifications to the rate increases at the two electric businesses. The effective date of new tariffs was December 1, 2020 with a

make-whole provision back to April 17, 2020. The proposed rates facilitate the companies’ transition to a cleaner energy future

while allowing for important initiatives such as COVID-19 relief for customers and additional funding for vegetation

management, hardening/resiliency and emergency preparedness. The rate plans continue the RAM designed to return or collect

certain defined reconciled revenues and costs, have new depreciation rates and continue existing RDMs for each business. The

2020 Joint Proposal bases delivery revenues on an 8.80% ROE and 48.00% equity ratio; however, for the proposed earnings

sharing mechanism, the equity ratio is the lower of the actual equity ratio or 50.00%. The below table provides a summary of

the approved delivery rate increases and delivery rate percentages, including rate levelization and excluding energy efficiency,

which is a pass-through, for all four businesses:

Year 1 Year 2 Year 3

Rate

Increase

Delivery

Rate %

Rate

Increase

Delivery

Rate %

Rate

Increase

Delivery

Rate %

Utility (Millions) Increase (Millions) Increase (Millions) Increase

NYSEG Electric $ 34 4.6 % $ 46 5.9 % $ 36 4.2 %

NYSEG Gas $ — — % $ 2 0.8 % $ 3 1.6 %

RG&E Electric $ 17 3.8 % $ 14 3.2 % $ 16 3.3 %

RG&E Gas $ — — % $ — — % $ 2 1.3 %

On May 26, 2022, NYSEG and RG&E filed for a new rate plan with the NYPSC. The rate filings are based on test year 2021

financial results adjusted to the rate year May 1, 2023 – April 30, 2024. Since these rate filings were submitted on May 26,

2022, the effective date of new rates, assuming an approximately 11-month suspension period, will be May 1, 2023. NYSEG

and RG&E filed for a one-year rate plan but expressed interest in exploring a multi-year plan during the pendency of the case

(as is the custom in New York). We cannot predict the outcome of these proceedings. In their filings, the following revenue

changes were requested:

Requested Revenue Change

Utility (Millions)

NYSEG Electric $ 274

NYSEG Gas $ 43

RG&E Electric $ 94

RG&E Gas $ 38

UI, CNG, SCG and BGC Rate Plans

In 2016, the Connecticut Public Utilities Regulatory Authority (PURA) approved new distribution rate schedules for The

United Illuminating Company (UI) for three years, which became effective January 1, 2017 and, among other things, provide

for annual tariff increases and an ROE of 9.10% based on a 50.00% equity ratio, continued UI’s existing earnings sharing

mechanism (ESM) pursuant to which UI and its customers share on a 50/50 basis all distribution earnings above the allowed

ROE in a calendar year, continued the existing decoupling mechanism and approved the continuation of the requested storm

reserve. Any dollars due to customers from the ESM continue to be first applied against any storm regulatory asset balance (if

one exists at that time) or refunded to customers through a bill credit if such storm regulatory asset balance does not exist.

In 2017, PURA approved new tariffs for the Southern Connecticut Gas Company (SCG) effective January 1, 2018. The new

tariffs also include an RDM and Distribution Integrity Management Program (DIMP) mechanism, ESM, the amortization of

certain regulatory liabilities (most notably accumulated hardship deferral balances and certain accumulated deferred income

taxes) and tariff increases based on an ROE of 9.25% and an equity ratio of approximately 52.00%. Any dollars due to

customers from the ESM will be first applied against any environmental regulatory asset balance as defined in the settlement

agreement (if one exists at that time) or refunded to customers through a bill credit if such environmental regulatory asset

balance does not exist.

19

In 2018, PURA approved new tariffs for Connecticut Natural Gas Corporation (CNG) effective January 1, 2019 for a three-year

rate plan with annual rate increases. The new tariffs continued the RDM and DIMP mechanism. ESM and tariff increases are

based on an ROE of 9.30% and an equity ratio of 54.00% in 2019, 54.50% in 2020 and 55.00% in 2021.

In 2019, the Massachusetts Department of Public Utilities (DPU) approved new distribution rates for Berkshire Gas Company

(BGC). The distribution rate increase is based on a 9.70% ROE and 54.00% equity ratio. The new tariffs provide for the

implementation of an RDM and pension expense tracker and also provide that BGC will not file to change base distribution

rates to become effective before November 1, 2021.

On June 24, 2022, BGC filed a Settlement Agreement with the Massachusetts Attorney General’s Office (AGO) for DPU

approval. The Settlement Agreement followed BGC’s December 14, 2021 filing of a Notice of Intent to File Rate Schedules.

Following that filing, BGC and the AGO negotiated the Settlement Agreement in lieu of a fully litigated rate case before the

DPU. The Settlement Agreement allows for agreed-upon adjustments to BGC’s revenue requirement as well as various step

increases BGC shall be entitled to on January 1, 2023 and January 1, 2024. The Settlement Agreement provides that it shall be

void unless approved in its entirety by the DPU by November 1, 2022. It provides for the opportunity to increase BGC’s

revenue requirement by as much as $5.6 million over current rates (reflective of a 9.7% ROE and a 54% equity ratio as well as

other stepped adjustments) through January 1, 2024. The Settlement Agreement is now before the DPU for approval. We

cannot predict the outcome of this proceeding.

Connecticut Energy Legislation

On October 7, 2020, the Governor of Connecticut signed into law an energy bill that, among other things, instructs PURA to

revise the rate-making structure in Connecticut to adopt performance-based rates for each electric distribution company,

increases the maximum civil penalties assessable for failures in emergency preparedness, and provides for certain penalties and

reimbursements to customers after storm outages greater than 96 hours and extends rate case timelines.

Pursuant to the legislation, on October 30, 2020, PURA re-opened a docket related to new rate designs and review, expanding

the scope to consider (a) the implementation of an interim rate decrease; (b) low-income rates; and (c) economic development

rates. Separately, UI was due to make its annual RAM filing on March 8, 2021 for the approval of its RAM Rate Components

reconciliations: Generation Services Charges, By-passable Federally Mandated Congestion Costs, System Benefits Charge,

Transmission Adjustment Charge and RDM.

On March 9, 2021, UI, jointly with the Office of the CT Attorney General, the Office of CT Consumer Counsel, DEEP and

PURA’s Office of Education, Outreach, and Enforcement entered into a settlement agreement and filed a motion to approve the

settlement agreement, which addressed issues in both dockets.

In an order dated June 23, 2021, PURA approved the as amended settlement agreement in its entirety and it was executed by the

parties. The settlement agreement includes a contribution by UI of $5 million and provides customers rate credits of $50 million

while allowing UI to collect $52 million in RAM, all over a 22-month period ending April 2023 and also includes a distribution

base rate freeze through April 2023.

Pursuant to the legislation, PURA opened a docket to consider the implementation of the associated customer compensation and

reimbursement provisions in emergency events where customers were without power for more than 96 consecutive hours. On

June 30, 2021, PURA issued a final decision implementing the legislative mandate to create a program pursuant to which

residential customers will receive $25 for each day without power after 96 hours and also receive reimbursement of $250 for

spoiled food and medicine. The decision emphasizes that no costs incurred in connection with this program are recoverable

from customers. The Company is reviewing the requirements of this program and evaluating next steps.

PURA Investigation of the Preparation for and Response to the Tropical Storm Isaias and Connecticut Storm

Reimbursement Legislation

On August 6, 2020, PURA opened a docket to investigate the preparation for and response to Tropical Storm Isaias by the

electric distribution companies in Connecticut including UI. Following hearings and the submission of testimony, PURA issued

a final decision on April 15, 2021, finding that UI “generally met standards of acceptable performance in its preparation and

response to Tropical Storm Isaias," subject to certain exceptions noted in the decision, but ordered a 15-basis point reduction to

UI's ROE in its next rate case to incentivize better performance and indicated that penalties could be forthcoming in the penalty

phase of the proceedings. On June 11, 2021, UI filed an appeal of PURA’s decision with the Connecticut Superior Court.

On May 6, 2021, in connection with its findings in the Tropical Storm Isaias docket, PURA issued a Notice of Violation to UI

for allegedly failing to comply with standards of acceptable performance in emergency preparation or restoration of service in

an emergency and with orders of the Authority, and for violations of accident reporting requirements. PURA assessed a civil

penalty in the total amount of $2 million. PURA held a hearing on this matter and, in an order dated July 14, 2021, reduced the

20

civil penalty to approximately $1 million. UI filed an appeal of PURA’s decision with the Connecticut Superior Court. This

appeal and the appeal of PURA’s decision on the Tropical Storm Isaias docket have been consolidated. We cannot predict the

outcome of these appeals.

Regulatory Assets and Liabilities

The regulatory assets and regulatory liabilities shown in the tables below result from various regulatory orders that allow for the

deferral and/or reconciliation of specific costs. Regulatory assets and regulatory liabilities are classified as current when

recovery or refund in the coming year is allowed or required through a specific order or when the rates related to a specific

regulatory asset or regulatory liability are subject to automatic annual adjustment.

Regulatory assets as of June 30, 2022 and December 31, 2021, respectively, consisted of:

June 30, December 31,

As of 2022 2021

(Millions)

Pension and other post-retirement benefits cost deferrals $ 327 $ 545

Pension and other post-retirement benefits 63 95

Storm costs 548 448

Rate adjustment mechanism 56 68

Revenue decoupling mechanism 53 68

Transmission revenue reconciliation mechanism 13 15

Contracts for differences 64 73

Hardship programs 26 24

Plant decommissioning 1 2

Deferred purchased gas 9 52

Deferred transmission expense 12 13

Environmental remediation costs 254 256

Debt premium 68 71

Unamortized losses on reacquired debt 22 23

Unfunded future income taxes 462 424

Federal tax depreciation normalization adjustment 139 142

Asset retirement obligation 20 20

Deferred meter replacement costs 52 46

COVID-19 cost recovery and late payment surcharge 22 21

Low income arrears forgiveness 36 —

Other 269 241

Total regulatory assets

2,516 2,647

Less: current portion 363 400

Total non-current regulatory assets

$ 2,153 $ 2,247

“Pension and other post-retirement benefits” represent the actuarial losses on the pension and other post-retirement plans that

will be reflected in customer rates when they are amortized and recognized in future pension expenses.

“Pension and other post-retirement benefits cost deferrals” include the difference between actual expense for pension and other

post-retirement benefits and the amount provided for in rates for certain of our regulated utilities. A portion of this balance is

amortized through current rates, the remaining portion will be refunded in future periods through future rate cases.

“Storm costs” for CMP, NYSEG, RG&E and UI are allowed in rates based on an estimate of the routine costs of service

restoration. The companies are also allowed to defer unusually high levels of service restoration costs resulting from major

storms when they meet certain criteria for severity and duration. A portion of this balance is amortized through current rates,

and the remaining portion will be determined through future rate cases.

“Rate adjustment mechanism” represents an interim rate change to return or collect certain defined reconciled revenues and

costs for NYSEG and RG&E following the approval of the Joint Proposal by the NYPSC. The RAM, when triggered, is

implemented in rates on July 1 of each year for return or collection over a twelve-month period.

21

"Revenue decoupling mechanism" represents the mechanism established to disassociate the utility's profits from its delivery/

commodity sales.

"Transmission revenue reconciliation mechanism" reflects differences in actual costs in the rate year from those used to set

rates. This mechanism contains the Annual Transmission True up (ATU), which is recovered over the subsequent June to May

period.

“Contracts for Differences” represent the deferral of unrealized gains and losses on contracts for differences derivative

contracts. The balance fluctuates based upon quarterly market analysis performed on the related derivatives. The amounts,

which do not earn a return, are fully offset by a corresponding derivative asset/liability.

“Hardship Programs” represent hardship customer accounts deferred for future recovery to the extent they exceed the amount in

rates.

“Plant decommissioning” represents decommissioning and demolition expenses related to closing fossil plant facilities - Beebe

& Russell.

“Deferred Purchased Gas” represents the difference between actual gas costs and gas costs collected in rates.

“Deferred Transmission Expense” represents deferred transmission income or expense and fluctuates based upon actual

revenues and revenue requirements.

“Environmental remediation costs” includes spending that has occurred and is eligible for future recovery in customer rates.

Environmental costs are currently recovered through a reserve mechanism whereby projected spending is included in rates with

any variance recorded as a regulatory asset or a regulatory liability. The amortization period will be established in future

proceedings and will depend upon the timing of spending for the remediation costs. It also includes the anticipated future rate

recovery of costs that are recorded as environmental liabilities since these will be recovered when incurred. Because no funds

have yet been expended for the regulatory asset related to future spending, it does not accrue carrying costs and is not included

within rate base.

“Debt premium” represents the regulatory asset recorded to offset the fair value adjustment to the regulatory component of the

non-current debt of UIL at the acquisition date. This amount is being amortized to interest expense over the remaining term of

the related outstanding debt instruments.

“Unamortized losses on reacquired debt” represent deferred losses on debt reacquisitions that will be recovered over the

remaining original amortization period of the reacquired debt.

“Unfunded future income taxes” represent unrecovered federal and state income taxes primarily resulting from regulatory flow

through accounting treatment and are the offset to the unfunded future deferred income tax liability recorded. The income tax

benefits or charges for certain plant related timing differences, such as removal costs, are immediately flowed through to, or

collected from, customers. This amount is being amortized as the amounts related to temporary differences that give rise to the

deferrals are recovered in rates. These amounts are being collected over a period of 46 years, and the NYPSC staff has initiated

an audit, as required, of the unfunded future income taxes and other tax assets to verify the balances.

“Federal tax depreciation normalization adjustment” represents the revenue requirement impact of the difference in the deferred

income tax expense required to be recorded under the IRS normalization rules and the amount of deferred income tax expense

that was included in cost of service for rate years covering 2011 forward. The recovery period in New York is from 25 to 35

years and for CMP 32.5 years beginning in 2020.

“Asset retirement obligations” represents the differences in timing of the recognition of costs associated with our AROs and the

collection of such amounts through rates. This amount is being amortized at the related depreciation and accretion amounts of

the underlying liability.

“Deferred meter replacement costs” represent the deferral of the book value of retired meters which were replaced or are

planned to be replaced by AMI meters. This amount is being amortized over the initial depreciation period of related retired

meters.

"COVID-19 cost recovery and late payment surcharge" represents: a) deferred COVID-19-related costs in the state of

Connecticut based on the order issued by PURA on April 29, 2020, requiring utilities to track COVID-19-related expenses and

lost revenue and create a regulatory asset, and b) deferred lost late payment revenue in the state of New York based on the order

issued by the NYPSC on June 17, 2022, approving deferral and surcharge/sur-credit mechanism to recover/return deferred

balances starting July 1, 2022.

22

“Low-income arrears forgiveness” represents deferred bill credits in the state of New York based on the order issued by the

NYPSC on June 16, 2022, approving deferral of bill credits for low-income customers and recovery of regulatory asset from all

customers over five years for RG&E and three years for NYSEG. Surcharge will start August 1, 2022.

“Other” includes post-term amortization deferrals and various items subject to reconciliation including hedge losses and

deferred property tax.

Regulatory liabilities as of June 30, 2022 and December 31, 2021, respectively, consisted of:

June 30, December 31,

As of 2022 2021

(Millions)

Energy efficiency portfolio standard

$ 34 $ 45

Gas supply charge and deferred natural gas cost

28 7

Pension and other post-retirement benefits cost deferrals

69 73

Carrying costs on deferred income tax bonus depreciation

16 23

Carrying costs on deferred income tax - Mixed Services 263A

5 7

2017 Tax Act

1,286 1,327

Rate Change Levelization

86 99

Revenue decoupling mechanism

17 13

Accrued removal obligations

1,198 1,192

Asset sale gain account

— 2

Economic development

23 26

Positive benefit adjustment

19 22

Theoretical reserve flow thru impact

5 6

Deferred property tax

18 22

Net plant reconciliation

14 16

Debt rate reconciliation

43 49

Rate refund – FERC ROE proceeding

35 35

Transmission congestion contracts

27 23

Merger-related rate credits

11 12

Accumulated deferred investment tax credits

22 24

Asset retirement obligation

18 18

Earning sharing provisions

14 13

Middletown/Norwalk local transmission network service

collections

17 17

Low income programs

25 25

Non-firm margin sharing credits

19 15

New York 2018 winter storm settlement

3 5

Hedge Gains

66 19

Other

301 194

Total regulatory liabilities

3,419 3,329

Less: current portion

447 307

Total non-current regulatory liabilities

$ 2,972 $ 3,022

“Energy efficiency portfolio standard” represents the costs of energy efficiency programs deferred for future recovery to the

extent they exceed the amount in rates. A portion of this balance is amortized through current rates, the remaining portion will

be refunded in future periods through future rate cases. The amortization period in current rates is three years and began in

2020.

23

"Gas supply charge and deferred natural gas cost" reflects the actual costs of purchasing, transporting and storing of natural gas.

Gas supply reconciliation is determined by comparing actual gas supply expenses to the monthly gas cost recoveries in rates.

Prior rate year balances are collected/returned to customers beginning the next calendar year.

“Pension and other postretirement benefits cost deferrals” include the difference between actual expense for pension and other

post-retirement benefits and the amount provided for in rates for certain of our regulated utilities. A portion of this balance is