UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Form 10-K

xx ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2015

Or

oo TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the transition period from to

Commission File No. 001-37660

Avangrid, Inc.

(Exact name of registrant as specified in its charter)

New York 4911 14-1798693

(State or other jurisdiction of

incorporation or organization)

(Primary Standard Industrial

Classification Code Number)

(I.R.S. Employer

Identification No.)

157 Church Street

New Haven, Connecticut

06506

(Address of principal executive offices) (Zip Code)

Telephone: (207) 688-6363

(Registrant’s telephone number, including area code)

Securities registered pursuant to Section 12(b) of the Act:

Title of each class Name of each exchange on which registered

Common Stock, $0.01 par value per share par value New York Stock Exchange

Securities registered pursuant to Section 12(g) of the Act: None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes o No x

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. Yes o No x

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12

months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes x No o

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data File required to be submitted and posted

pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for shorter period that the registrant was required to submit and post such files).

Yes x No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§229.405) is not contained herein, and will not be contained, to the best of

registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. x

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large

accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check one):

Large accelerated filer o Accelerated filer o

Non-accelerated filer x (Do not check if a smaller reporting company) Smaller reporting company o

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes o No x

State the aggregate market value of the voting and non-voting common equity held by non-affiliates of the registrant as of June 30, 2015, the last business day of the registrant’s most

recently completed second fiscal quarter: the registrant’s common stock was not publicly traded.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date: 308,962,088 shares of common stock, par value $0.01,

were outstanding as of March 28, 2016.

DOCUMENTS INCORPORATED BY REFERENCE

Portions of the documents listed below have been incorporated by reference into the indicated parts of this report, as specified in the responses to the item numbers involved.

Designated portions of the Proxy Statement relating to the 2016 Annual Meeting of the Shareholders are incorporated by reference into Part III to the extent described therein.

TABLE OF CONTENTS

GLOSSARY OF TERMS AND ABBREVIATIONS 1

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS 5

PART I 6

Item 1. Business 6

Item 1A. Risk Factors 25

Item 1B. Unresolved Staff Comments. 40

Item 2. Properties. 40

Item 3. Legal Proceedings. 40

Item 4. Mine Safety Disclosures. 43

Executive Officers of AVANGRID 44

PART II 46

Item 5. Market for Registrant’s Common Equity, Related Stockholder Matters and Issuer Purchases of Equity Securities. 46

Item 6. Selected Financial Data 47

Item 7. Management’s Discussion and Analysis of Financial Condition and Results of Operations 48

Item 7A. Quantitative and Qualitative Disclosures About Market Risk 77

Item 8. Financial Statements and Supplementary Data 80

Item 9. Changes in and Disagreements with Accountants on Accounting and Financial Disclosure. 168

Item 9A. Controls and Procedures. 168

Item 9B. Other information. 168

PART III 169

Item 10. Directors, Executive Officers and Corporate Governance. 169

Item 11. Executive Compensation. 169

Item 12. Security Ownership of Certain Beneficial Owners and Management and Related Stockholder Matters. 169

Item 13. Certain Relationships and Related Transactions, and Director Independence. 169

Item 14. Principal Accounting Fees and Services. 169

Part IV 170

Item 15. Exhibits and Financial Statement Schedules. 170

SIGNATURES 175

i

GLOSSARY OF TERMS AND ABBREVIATIONS

Unless the context indicates otherwise, the terms “we,” and “our” are used to refer to AVANGRID and its subsidiaries.

GenConn Devon refers to GenConn’s peaking generating plant in Devon, Connecticut.

GenConn Middletown refers to GenConn’s peaking generating plant in Middletown, Connecticut.

Iberdrola Group refers to the group of companies controlled by Iberdrola, S.A.

Iberdrola, S.A. refers to the 81.5% controlling parent company of AVANGRID, Inc.

Installed capacity refers to the production capacity of a power plant or wind farm based either on its rated (nameplate) capacity or actual capacity.

Klamath Plant refers to the Klamath gas-fired cogeneration facility.

Merger Agreement refers to the Agreement and Plan of Merger, dated as of February 25, 2015, by and among AVANGRID, Inc., Green Merger Sub, Inc. and

UIL Holdings Corporation.

NED pipeline refers to TGP’s proposed Northeast Energy Direct project.

Yankee Companies refers to the Maine Yankee Atomic Power Company, the Connecticut Yankee Power Corporation, and the Yankee Atomic Energy

Corporation.

AMI Automated Metering Infrastructure

AOCI

Accumulated other comprehensive income

ARHI Avangrid Renewables Holdings, Inc.

ASC

Accounting Standards Codification

Army Corps U.S. Army Corps of Engineers

ARO Asset retirement obligation

AVANGRID AVANGRID, Inc.

Bcf One billion cubic feet

Berkshire The Berkshire Gas Company

BGEPA Bald and Golden Eagle Protection Act

BLM U.S. Bureau of Land Management

Cayuga Cayuga Operating Company, LLC

CENG Constellation Energy Nuclear Group, LLC

CfDs Contracts for Differences

CFTC Commodity Futures Trading Commission

CL&P The Connecticut Light and Power Company

CMP Central Maine Power Company

CNG Connecticut Natural Gas Corporation

CSC Connecticut Siting Council

DCF Discounted cash flow

DER Distributed energy resources

Dodd-Frank Act Dodd-Frank Wall Street Reform and Consumer Protection Act

DOE Department of Energy

DOJ Department of Justice

DPA Deferred Payment Arrangements

DPU Massachusetts Department of Public Utilities

DSIP Distributed System Implementation Plan

DSP Distributed System Platform

DTh Dekatherm

EBITDA Earnings before interest, taxes, depreciation and amortization

EPA Environmental Protection Agency

EPAct 2005 Energy Policy Act of 2005

ERCOT Electric Reliability Council of Texas

ESA Endangered Species Act

ESC Earnings Smart Community

ESM Earnings sharing mechanism

Exchange Act The Securities Exchange Act of 1934, as amended

FASB Financial Accounting Standards Board

FERC Federal Energy Regulatory Commission

FirstEnergy FirstEnergy Corp.

FPA Federal Power Act

Gas Enstor Gas, LLC

GenConn GenConn Energy LLC

Ginna Ginna Facility and GNPP

Ginna Facility R.E. Ginna Nuclear Power Plant

GNPP Ginna Nuclear Power Plant

GSRP Greater Springfield Reliability Project

HLPSA Hazardous Liquids Pipeline Safety Act of 1979

IRP Interstate Reliability Project

IRS Internal Revenue Service

ISO Independent system operator

ISO-NE ISO New England, Inc.

Kinder Morgan Kinder Morgan, Inc.

kV Kilovolts

kWh Kilowatt-hour

LIBOR London Interbank Offer Rate

LNS Local Network Service

MBTA Migratory Bird Treaty Act

Mcf One thousand cubic feet of natural gas

2

Merger Sub Green Merger Sub, Inc.

MEPCO Maine Electric Power Corporation

MGP Manufactured Gas Plants

MISO Midcontinent Independent System Operator, Inc.

MHI Mitsubishi Heavy Industries

MNG Maine Natural Gas Corporation

MOU Memorandum of Understanding

MPRP Maine Reliability Power Program

MPUC Maine Public Utilities Commission

MW Megawatts

MWh Megawatt-hours

NAV Net asset value

NEEWS New England East West Solution

NEPA National Environmental Policy Act

NERC North American Electric Reliability Corporation

Networks Avangrid Networks, Inc.

New York TransCo New York TransCo, LLC.

NIPSCO Northern Indiana Public Service Company

NGA Natural Gas Act of 1938

NGPSA Natural Gas Pipeline Safety Act of 1968

NOL Net operating loss

NPNS Normal purchases and normal sales

NYISO New York Independent System Operator, Inc.

NYPA New York Power Authority

NYPSC New York State Public Service Commission

NYSE New York Stock Exchange

NYSEG New York State Electric & Gas Corporation

OATT Open Access Transmission Tariiff

OCC Office of Consumer Counsel

OSHA Occupational Safety and Health Act, as amended

PCB Polychlorinated Biphenyls

PHMSA Pipeline and Hazardous Materials Safety Administration

PPA Power purchase agreement

PTF Pool Transmission Facilities

PUCT Public Utility Commission of Texas

PUHCA 2005 Public Utility Holding Company Act of 2005

3

PURA Connecticut Public Utilities Regulatory Authority

RAM Rate Adjustment Mechanism

RCRA Resource Conservation and Recovery Act

RDM Revenue decoupling mechanism

REC Renewable Energy Certificate

RFP Request for Proposals

Renewables Avangrid Renewables, LLC

REV Reforming the Energy Vision

RGE Rochester Gas and Electric Corporation

ROE Return on equity

RNS Regional Network Service

RPS Renewable Portfolio Standards

RSSA Reliability Support Services Agreement

RTO Regional transmission organizations

SCG The Southern Connecticut Gas Company

SEC United States Securities and Exchange Commission

SNF Spent Nuclear Fuel

SPHI Scottish Power Holdings, Inc.

TEF Tax equity financing arrangements

TGP Tennessee Gas Pipeline Company LLC

TOTS Transmission Owner Transmission Solutions

UI The United Illuminating Company

UIL UIL Holdings Corporation

WECC Western Electricity Coordinating Council

4

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This Annual Report on Form 10-K contains a number of forward-looking statements. Forward-looking statements may be identified by the use of

forward-looking terms such as “may,” “will,” “should,” “can,” “expects,” “believes,” “anticipates,” “intends,” “plans,” “estimates,” “projects,” “assumes,”

“guides,” “targets,” “forecasts,” “is confident that” and “seeks” or the negative of such terms or other variations on such terms or comparable terminology.

Such forward-looking statements include, but are not limited to, statements about our plans, objectives and intentions, outlooks or expectations for earnings,

revenues, expenses or other future financial or business performance, strategies or expectations, or the impact of legal or regulatory matters on business,

results of operations or financial condition of the business and other statements that are not historical facts. Such statements are based upon the current beliefs

and expectations of our management and are subject to significant risks and uncertainties that could cause actual outcomes and results to differ materially.

Important factors that could cause actual results to differ materially from those indicated by such forward-looking statements include, without limitation, the

risks and uncertainties set forth under Part I, Item 1A, “Risk Factors” in this report. Specifically, forward-looking statements may include statements relating

to:

·

the future financial performance, anticipated liquidity and capital expenditures of the company;

·

success in retaining or recruiting, or changes required in, our officers, key employees or directors;

·

the risk that the businesses will not be coordinated successfully, or that the coordination will be more costly or more time consuming and

complex than anticipated;

·

disruption from the merger making it difficult to maintain business and operational relationships;

·

adverse developments in general market, business, economic, labor, regulatory and political conditions;

·

the impact of any cyber-breaches, acts of war or terrorism or natural disasters; and

·

the impact of any change to applicable laws and regulations affecting operations, including those relating to environmental and climate

change, taxes, price controls, regulatory approval and permitting.

Should one or more of these risks or uncertainties materialize, or should any of the underlying assumptions prove incorrect, actual results may vary in

material respects from those expressed or implied by these forward-looking statements. You should not place undue reliance on these forward-looking

statements. We do not undertake any obligation to update or revise any forward-looking statements to reflect events or circumstances after the date of this

report, whether as a result of new information, future events or otherwise, except as may be required under applicable securities laws.

5

PART I

Item 1. Business

Overview

AVANGRID, Inc., or AVANGRID, formerly Iberdrola USA, Inc., is a New York corporation headquartered in New Gloucester, Maine. We are a direct,

majority owned subsidiary of Iberdrola, S.A., a corporation (sociedad anónima) organized under the laws of Spain, one of the world’s leading energy

companies. Our primary business is ownership of our operating businesses, which are described below.

Our direct, wholly-owned subsidiaries include Avangrid Networks, Inc., or Networks, Avangrid Renewables Holdings, Inc., or ARHI, and UIL Holdings

Corporation, or UIL. ARHI in turn holds subsidiaries including Avangrid Renewables LLC, or Renewables, and Enstor Gas, LLC, or Gas. Networks, along

with UIL, owns and operates our regulated utility businesses, including electric transmission and distribution and natural gas distribution, transportation and

sales. Renewables operates a portfolio of renewable energy generation facilities primarily using onshore wind power, and also solar, biomass and thermal

power. Gas operates our natural gas storage facilities and gas trading businesses through Enstor Energy Services LLC (gas trading) and Enstor Inc. (gas

storage). Avangrid Service Company, a subsidiary of Networks, provides corporate and back office services on a consolidated basis to our subsidiaries.

On December 16, 2015, we completed an acquisition, pursuant to which UIL merged with and into our wholly-owned subsidiary, Green Merger Sub,

Inc., or Merger Sub, with Merger Sub surviving as our wholly-owned subsidiary. The acquisition was effected pursuant to the Agreement and Plan of Merger,

dated as of February 25, 2015, or the Merger Agreement, by and among us, Merger Sub, and UIL. Following the completion of the acquisition, Merger Sub

was renamed “UIL Holdings Corporation.”

The primary business of UIL is the ownership of its operating regulated utility businesses. The utility businesses consist of the electric distribution and

transmission operations of The United Illuminating Company, or UI, and the natural gas transportation, distribution and sales operations of The Southern

Connecticut Gas Company, or SCG, Connecticut Natural Gas Corporation, or CNG, and The Berkshire Gas Company, or Berkshire. For purposes of this

document, all references to “Networks” include UIL and its subsidiaries, unless otherwise indicated.

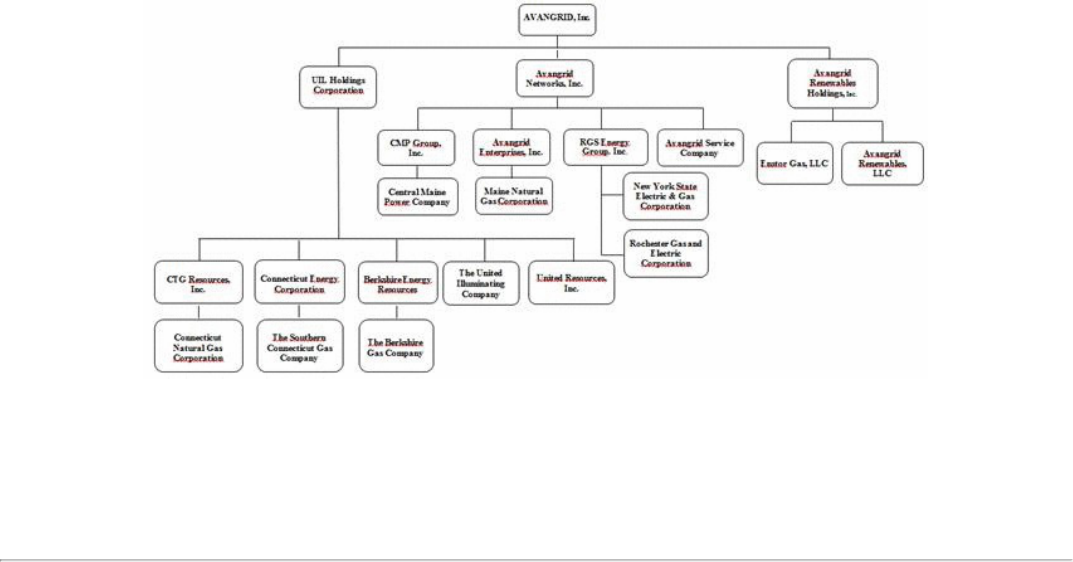

After the acquisition UIL became a direct subsidiary of AVANGRID, which resulted in the following structure:

We currently anticipate that UIL and its subsidiaries will be moved under Networks in the first half of 2016. Through Networks, we own electric

generation, transmission and distribution companies and natural gas distribution, transportation and sales companies in New York and Maine, and manage

electric generation, transmission and distribution companies and natural gas distribution, transportation and sales companies in Connecticut and

Massachusetts, delivering electricity to approximately 2.2 million electric utility customers and delivering natural gas to approximately 984,000 natural gas

public utility customers as of December 31, 2015. The interstate transmission and wholesale sale of electricity by these regulated utilities is regulated by the

Federal Energy Regulatory

6

Commission, or FERC, under the Federal Power Act, or FPA, including with respect to transmission rates. Further, Networks’ electric and gas distribution

utilities in New York, Maine, Connecticut and Massachusetts are subject to regulation by the New York State Public Service Commission, or NYPSC, the

Maine Public Utilities Commission, or MPUC, the Connecticut Public Utilities Regulatory Authority, or PURA, and the Massachusetts Department of Public

Utilities, or DPU, respectively. Networks strives to be a leader in safety, reliability and quality of service to its utility customers.

Through Renewables, we had a combined wind, solar and thermal installed capacity of 6,330 megawatts, or MW, as of December 31, 2015, including

Renewables’ share of joint projects, of which 5,643 MW was installed wind capacity. Approximately 67% of the capacity was contracted for an average

period of 9.7 years as of December 31, 2015. As the second largest wind operator in the United States based on installed capacity as of December 31, 2015,

Renewables strives to lead the transformation of the U.S. energy industry to a competitive, clean energy future. Renewables currently operates 53 wind farms

in 18 states across the United States.

Through Gas, as of December 31, 2015 we own approximately 67.5 billion cubic feet, or Bcf, of net working gas storage capacity. Through Enstor

Energy Services, LLC, Gas operates 53.25 Bcf of contracted or managed gas storage capacity in North America as of December 31, 2015.

Further information regarding the amount of revenues from external customers, including revenues by products and services, a measure of profit or loss

and total assets for each segment for each of the last three fiscal years is provided in Note 23 of our audited combined and consolidated financial statements

for the three years ended December 31, 2015, which is incorporated herein by reference.

History

We were incorporated in 1997 as a New York corporation under the name NGE Resources, Inc. and subsequently changed our name to Energy East

Corporation. The stock of Energy East Corporation was publicly traded on the New York Stock Exchange, or the NYSE. In 2007, Iberdrola, S.A. acquired

Scottish Power Ltd., or Scottish Power, including ScottishPower Holdings, Inc., or SPHI, the parent company of Scottish Power’s U.S. subsidiaries. Through

this acquisition, Iberdrola, S.A. acquired PPM Energy, a subsidiary that operated SPHI’s U.S. wind business, thermal generation operations and the gas storage

and energy management businesses and changed PPM Energy’s name to Renewables. In 2008, Iberdrola, S.A. acquired Energy East Corporation and we

changed our name to Iberdrola USA, Inc. in December 2009. In 2013, we completed an internal corporate reorganization to create a unified corporate

presence for the Iberdrola brand in the United States, bringing all of its U.S. energy companies under one single holding company, Iberdrola USA. The

internal reorganization, completed in November 2013, resulted in the concentration of our principal businesses in two major subsidiaries: Networks, which

holds all of our regulated utilities; Renewables, which holds our renewable and thermal generation businesses, and gas storage and marketing businesses.

We were the corporate parent of SCG, CNG and Berkshire prior to UIL acquiring those companies in 2010.

On December 16, 2015, UIL became our wholly-owned subsidiary as a result of merging into Merger Sub, our wholly-owned subsidiary, with Merger

Sub surviving as our wholly-owned subsidiary. Following the completion of the acquisition, Merger Sub was renamed “UIL Holdings Corporation” and we

were renamed AVANGRID, Inc. On February 18, 2016, the following AVANGRID subsidiaries changed their names as set forth below:

Old Company Name New Company Name

Iberdrola USA Networks, Inc. Avangrid Networks, Inc.

Iberdrola USA Solutions, Inc. Avangrid Solutions, Inc.

Iberdrola USA Group, LLC Avangrid Management Company, LLC

Iberdrola USA Management Corporation Avangrid Service Company

Iberdrola USA Enterprises, Inc. Avangrid Enterprises, Inc.

Iberdrola USA Networks New York TransCo, LLC Avangrid Networks New York TransCo, LLC

Iberdrola Energy Holdings, LLC Enstor Gas, LLC

Iberdrola Energy Services, LLC Enstor Energy Services, LLC

Iberdrola Renewables, LLC Avangrid Renewables, LLC

Iberdrola Renewables Holdings, Inc. Avangrid Renewables Holdings, Inc.

Iberdrola Arizona Renewables, LLC Avangrid Arizona Renewables, LLC

Iberdrola Texas Renewables, LLC Avangrid Texas Renewables, LLC

Iberdrola Logistic Services, LLC Avangrid Logistic Services, LLC

7

Networks

Overview

Networks, a Maine corporation, along with UIL, a Connecticut corporation, hold our regulated utility businesses, including electric transmission and

distribution and natural gas distribution, transportation and sales. Networks serves as a super-regional energy services and delivery company through eight

regulated utilities it owns directly or through UIL:

·

New York State Electric & Gas Corporation, or NYSEG: serves electric and natural gas customers across more than 40% of the upstate New

York geographic area;

·

Rochester Gas and Electric, or RGE: serves electric and natural gas customers within a nine-county region in western New York, centered

around Rochester;

·

UI: serves electric customers in southwestern Connecticut;

·

Central Maine Power Company, or CMP: serves electric customers in central and southern Maine;

·

SCG: serves natural gas customers in Connecticut;

·

CNG: serves natural gas customers in Connecticut;

·

Berkshire: serves natural gas customers in western Massachusetts; and

·

Maine Natural Gas Corporation, or MNG: serves natural gas customers in several communities in central and southern Maine;

For the year ended December 31, 2015, Networks distributed 37,528,920 megawatt-hours, or MWh, of electricity (includes 12 months of operation of

UIL). As of December 31, 2015, Networks provided service to its 2.2 million customers in the states of New York, Maine, Connecticut and Massachusetts. In

total, the electric system of Networks’ regulated utilities consisted of 8,482 miles of transmission lines, 70,916 miles of distribution lines and 826 substations

as of December 31, 2015. Furthermore, for the year ended December 31, 2015, Networks delivered more than 205 million dekatherms, or DTh, of natural gas

(includes 12 months of operation of UIL), to approximately 984,000 customers, providing service in the states of New York, Maine, Connecticut and

Massachusetts.

The demand for electric power and natural gas is affected by seasonal differences in the weather. Demand for electricity in each of the states in which

Networks operates tends to increase during the summer months to meet cooling load or in winter months for heating load while statewide demand for natural

gas tends to increase during the winter to meet heating load.

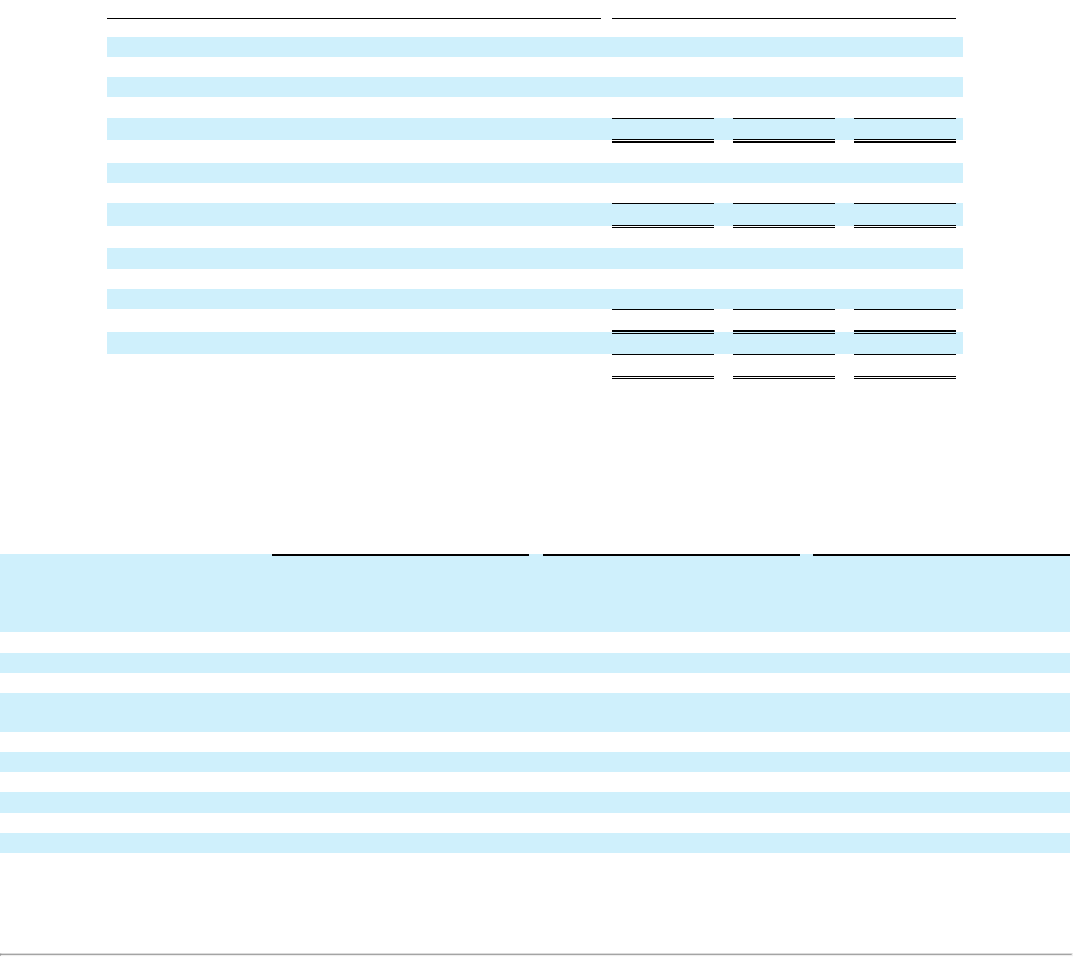

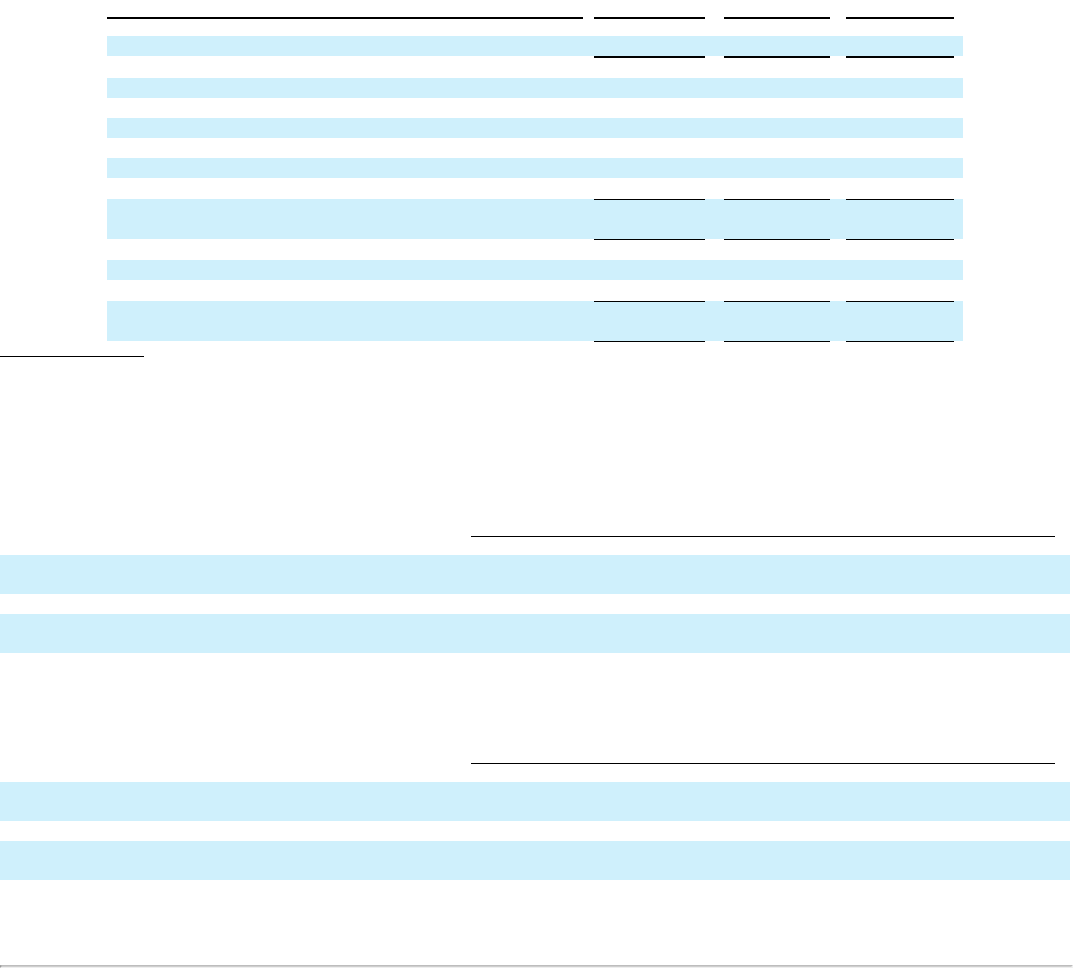

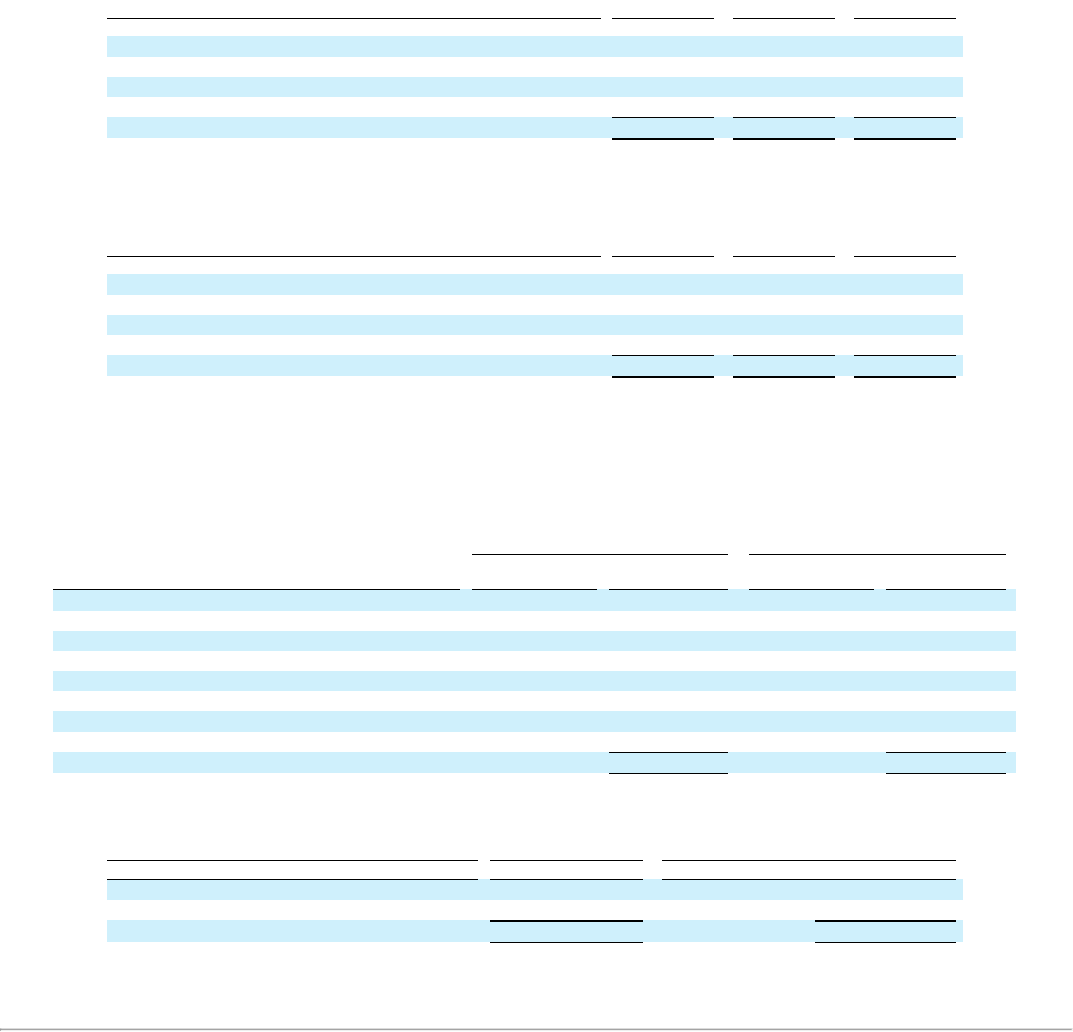

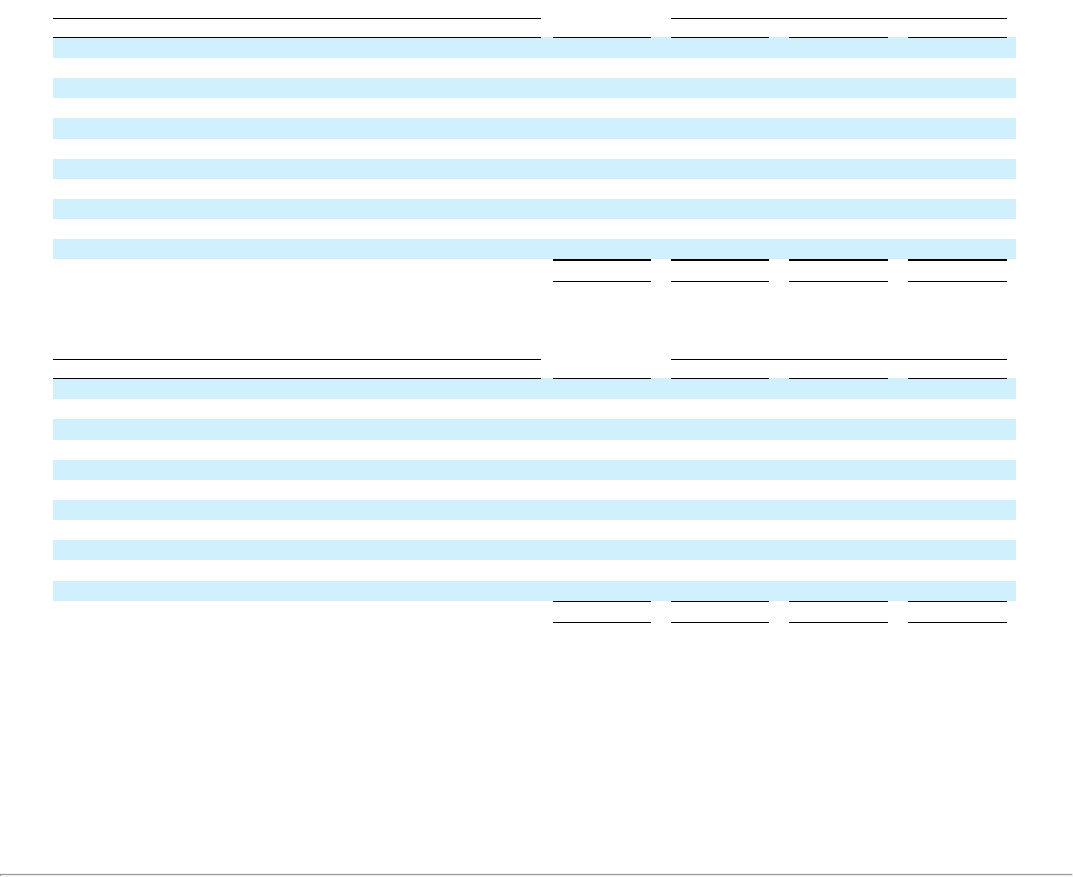

The following table sets forth certain information relating to the, rate base, number of customers and the amount of electricity or natural gas provided

by each of Networks’ regulated utilities for the year ended December 31, 2015:

Rate Base

(1)

(in billions)

Electricity

Customers

Electricity

Delivered

(in MWh)

Natural Gas

Customers

Natural Gas

Delivered

(in DTh)

Utility

December 31,

2015

December 31,

2015

For the

year ended

December 31,

2015

December 31,

2015

For the

year ended

December 31,

2015

NYSEG $ 2.4 885,000 15,711,000 265,000 56,533,000

RGE $ 1.6 375,000 7,110,000 310,000 51,498,000

CMP $ 2.3 616,979 9,256,920 — —

MNG $ 0.1 — — 4,432 15,400,000

UI $ 1.5 331,216 5,451,000 — —

SCG $ 0.5 — — 192,557 33,978,000

CNG $ 0.4 — — 172,498 37,387,000

Berkshire $ 0.1 — — 39,680 10,569,000

(1) “Rate base” means the net assets upon which a utility can receive a specified return, based on the value of such assets. The rate base is set by the relevant regulatory authority

and typically represents the value of specified property, such as plants, facilities and other investments of the utility.

Over the last five years, Networks has invested nearly $6.0 billion in creating a delivery network with greater capacity and improved reliability,

environmental security and sustainability, efficiency and automation. Networks continuously improves its grid to accommodate new requirements for

advanced metering, demand response and enhanced outage management, while improving its

8

flexibility for the integration and management of distributed energy resources, or DER. From 2009 to 2015, Networks increased capital expenditure

investments in its New York and Maine regulated utilities by 131%, from $315.0 million to $727.0 million.

New York

As of December 31, 2015, NYSEG served approximately 885,000 electricity customers and 265,000 natural gas customers across more than 40% of

upstate New York’s geographic area, while RGE served approximately 375,000 electricity customers and 310,000 natural gas customers in a nine-county

region centered around Rochester, in western New York.

In 2015, NYSEG and RGE’s nine hydroelectric plants generated nearly 366 million kilowatt-hours, or kWh, of clean hydropower, which is enough

energy to power 51,000 homes across New York State, assuming an average electricity consumption of 600 kWh per month per customer. See “—Properties—

Networks” for more information regarding Networks’ electric generation plants.

Networks also holds an approximate 20% ownership interest in the regulated New York TransCo, LLC, or New York TransCo. Through New York

TransCo, Networks has formed a partnership along with Central Hudson Gas and Electric Corporation, Consolidated Edison, Inc., National Grid, plc and

Orange and Rockland Utilities, Inc. to develop a portfolio of interconnected transmission lines and substations to fulfill the objectives of the New York

energy highway initiative, a proposal to install up to 3,200 MW of new electric generation and transmission capacity in order to deliver more power

generated from upstate New York power plants to downstate New York.

Maine

As of December 31, 2015, CMP delivered electricity to more than 616,000 customers in an 11,000 square-mile service area in central and southern

Maine. CMP has completed a $1.4 billion investment plan for the construction of upgrades to the bulk power transmission grid in Maine, the largest

transmission investment in the history of Maine, which includes the construction of five new 345-kilovolt, or kV, substations and related facilities linked by

approximately 440 miles of new transmission lines (refers to the Maine Power Reliability Program, or MPRP). CMP in 2012 also completed a $200.0 million

investment, one-half of which was funded by the Department of Energy, or DOE, in advanced meter infrastructure, which included the installation of more

than 600,000 smart meters for all of its electric customers. Smart meters monitor and record a customer’s power consumption, eliminating the need for on-

site meter reading.

CMP also owns 78% of the Maine Electric Power Corporation, or MEPCO, a single-asset 182 mile 345kV electric transmission line from Orrington,

Maine to Wiscasset, Maine.

MNG delivers natural gas to 4,432 customers in central and southern Maine and recently completed construction of the first natural gas pipeline in

Augusta, Maine. Through MNG, Networks provides these communities in southern Maine with access to natural gas for the first time, offering a competitive

and clean energy option to homes and businesses.

Connecticut

As of December 31, 2015, UI served more than 331,000 residential, commercial and industrial customers in a service area of approximately 335 square

miles in the southwestern part of Connecticut. The service area includes Bridgeport and New Haven and is home to a diverse array of business sectors

including aerospace manufacturing, healthcare, biotech, financial services, precision manufacturing, retail and education. UI’s retail electric revenues vary

by season, with the highest revenues typically in the third quarter of the year reflecting seasonal rates, hotter weather and air conditioning use.

UI is also a party to a joint venture with certain affiliates of NRG Energy, Inc., pursuant to which UI holds 50% of the membership interests in GCE

Holding LLC, whose wholly owned subsidiary, GenConn Energy LLC, or GenConn, operates peaking generation plants in Devon, Connecticut, or GenConn

Devon, and Middletown, Connecticut, or GenConn Middletown.

As of December 31, 2015, SCG and CNG provided local gas distribution services to approximately 364,000 customers in the greater Hartford-New

Britain area, Greenwich and the southern Connecticut coast from Westport to Old Saybrook, including the cities of Bridgeport and New Haven.

9

Massachusetts

As of December 31, 2015, Berkshire provided local gas distribution services to approximately 40,000 customers in a service area in western

Massachusetts which includes the cities of Pittsfield, North Adams and Greenfield.

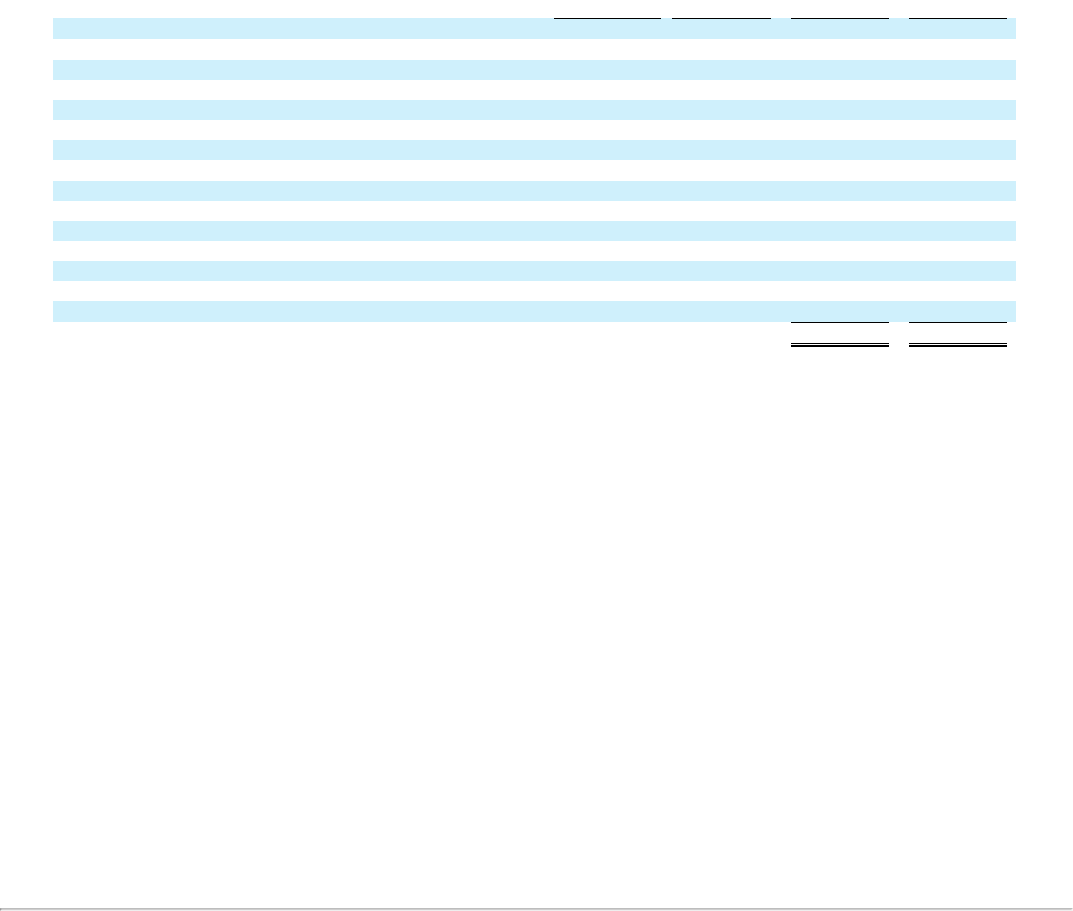

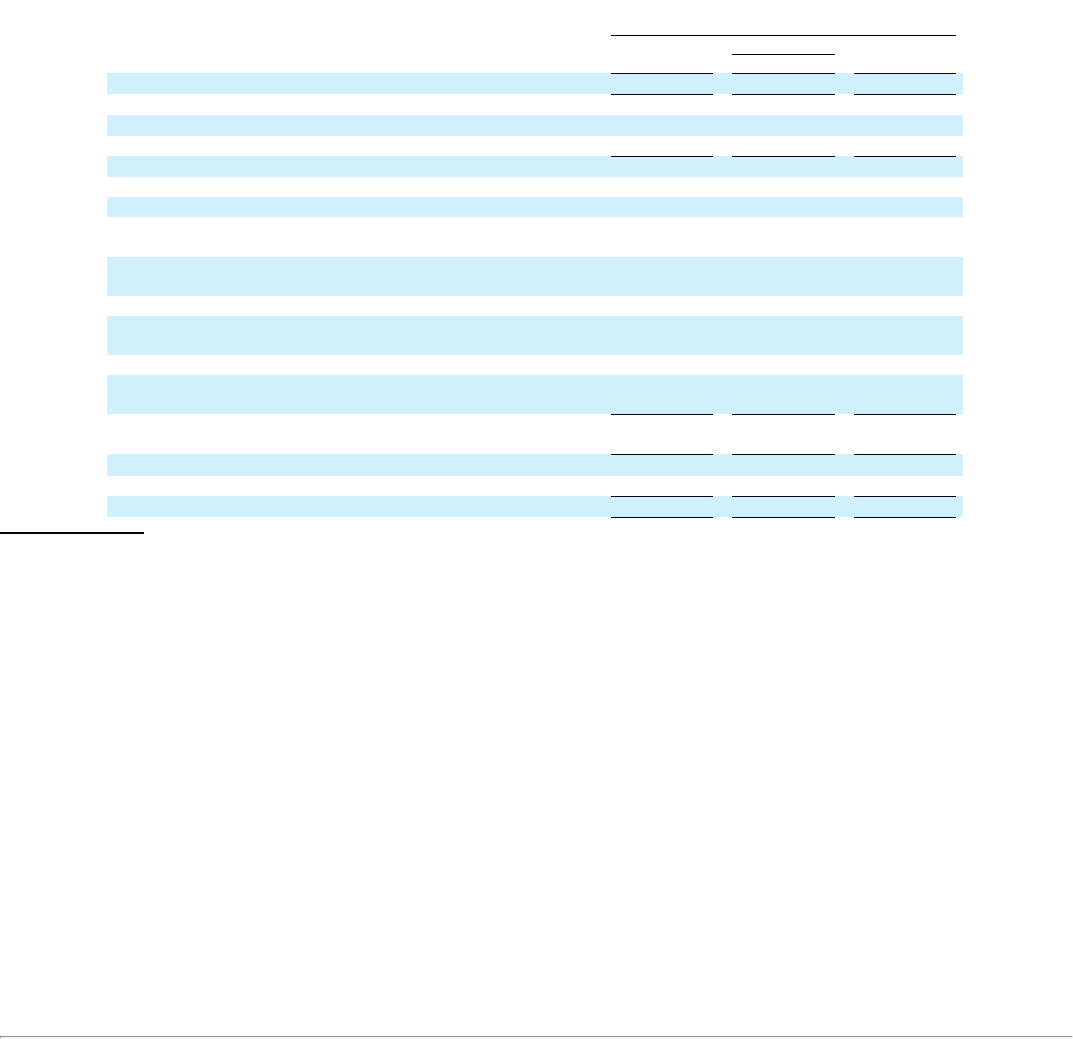

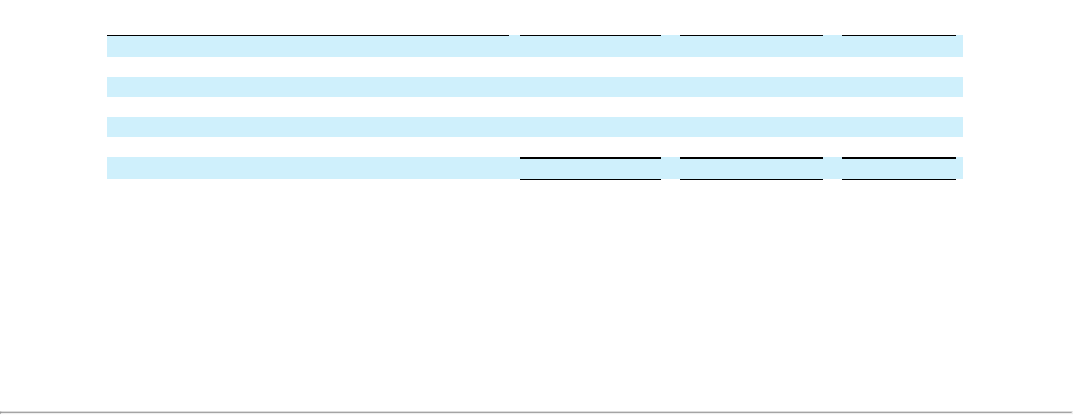

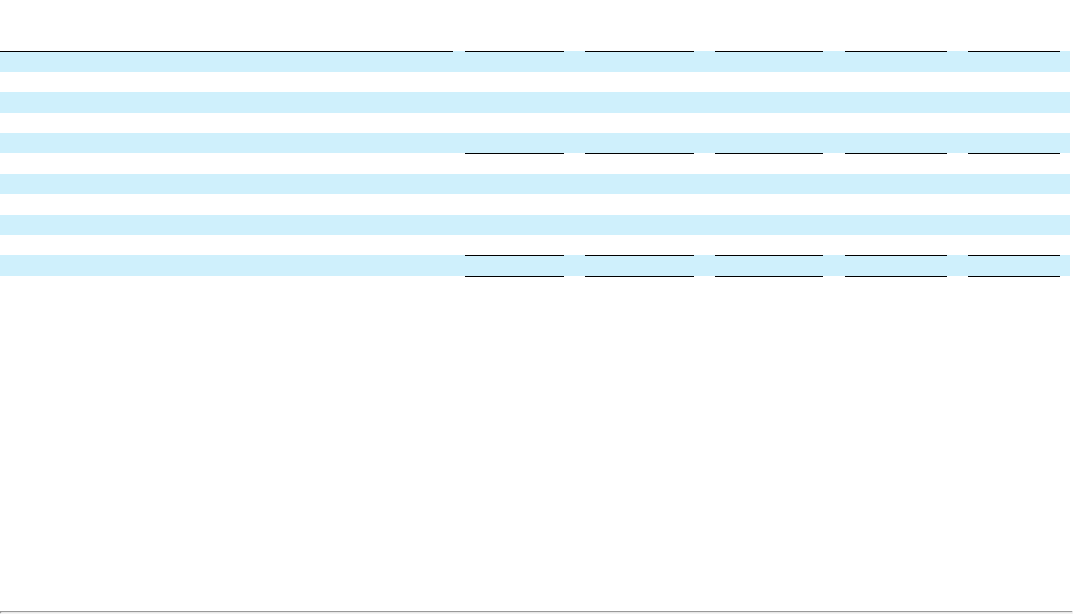

The rate base of Networks’ regulated utilities has increased significantly over the last three years, mainly due to the investments in regulated projects,

such as the Maine Reliability Power Program, or MPRP, transmission project in Maine and increased replacement of aging infrastructure and investments in

smart grid automation. The rate base of Networks’ regulated utilities for the years indicated below have been as follows:

Rate base 2013 2014 2015

(in millions)

NYSEG Electric $ 1,702 $ 1,796 $ 1,825

NYSEG Gas 482 508 531

RGE Electric 1,058 1,111 1,175

RGE Gas 427 444 446

Subtotal New York 3,669 3,859 3,977

CMP Dist 714 739 781

CMP Trans 1,252 1,467 1,472

MNG 47 64 60

Subtotal Maine 2,013 2,270 2,313

UI Dist 760 823 942

UI Trans 500 500 508

SCG 468 461 477

CNG 396 382 396

Subtotal Connecticut 2,124 2,166 2,323

Berkshire 70 72 91

Total $ 7,876 $ 8,367 $ 8,704

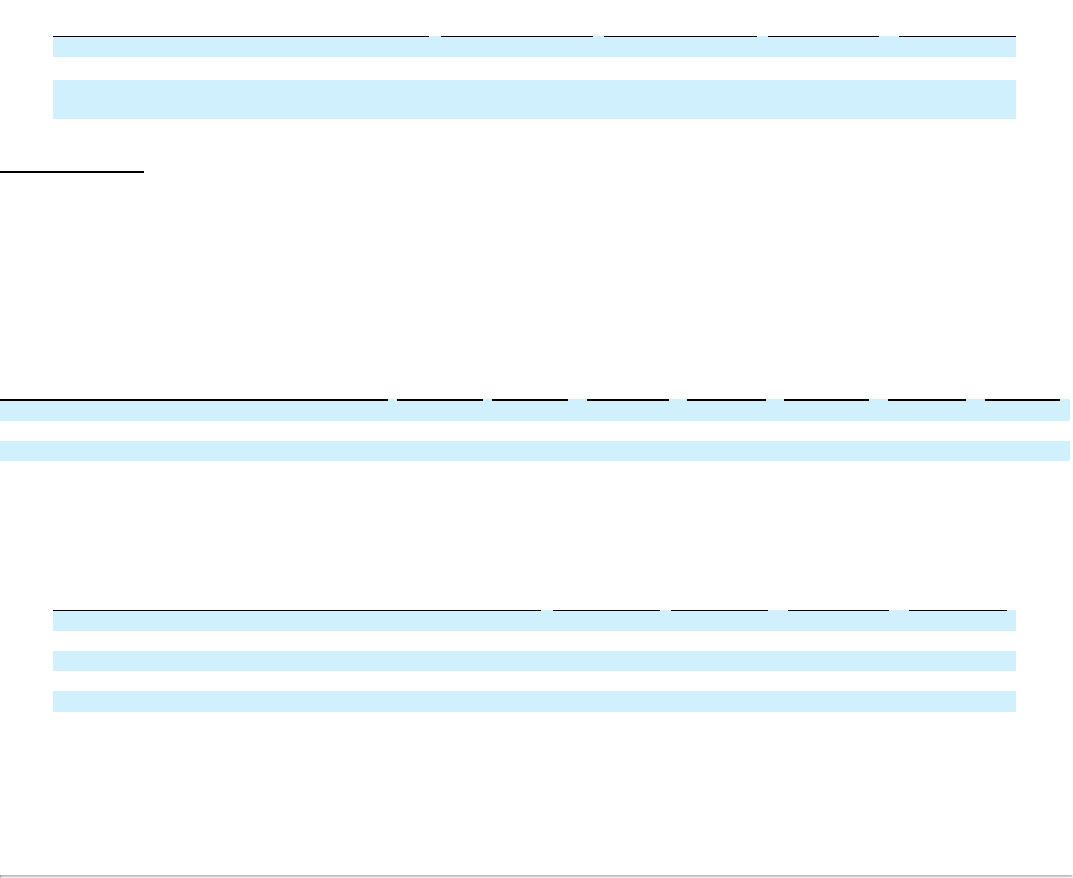

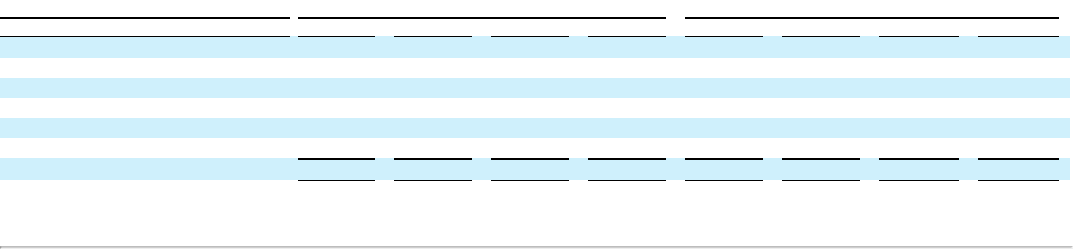

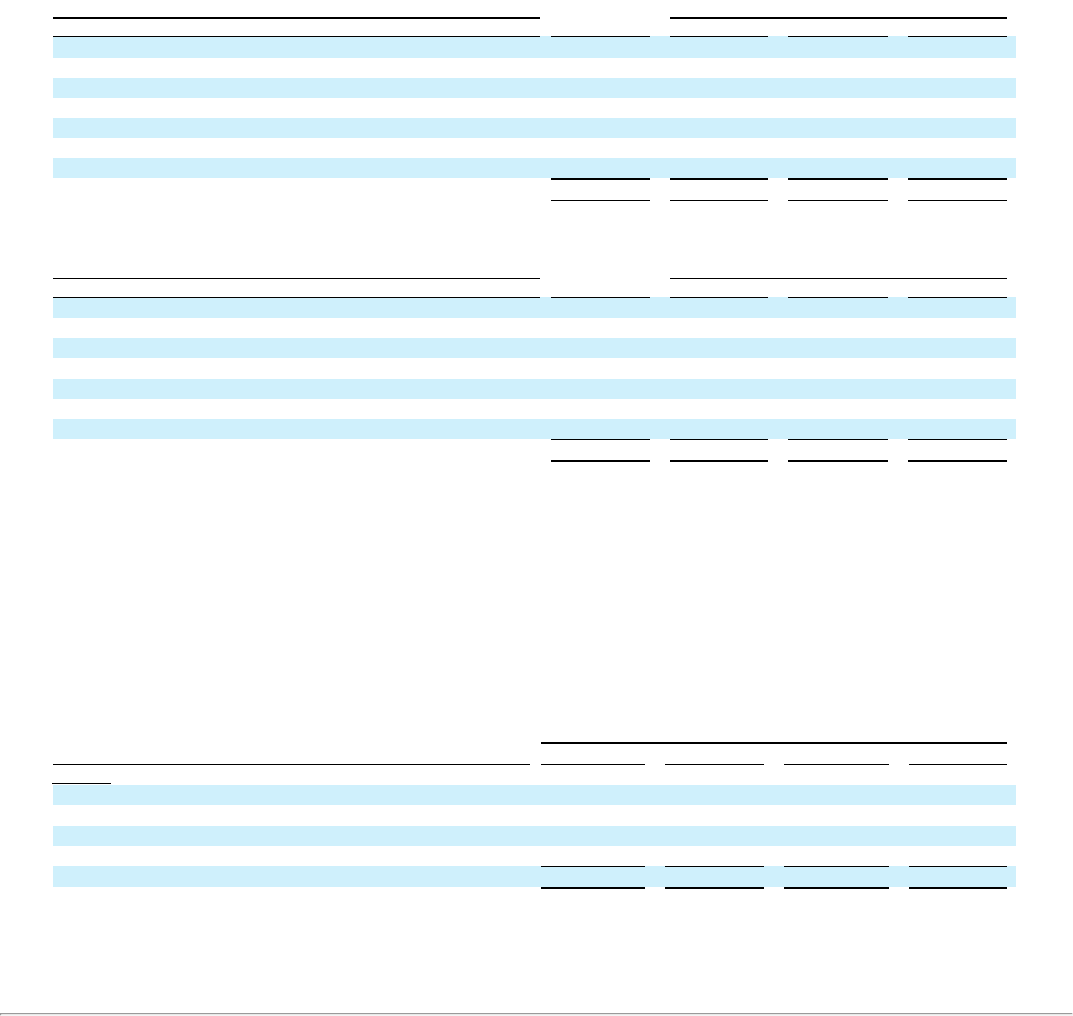

Earnings Sharing Mechanisms

The regulated utilities’ rate plans approved by regulators in New York, Maine, Connecticut and Massachusetts typically include earnings sharing

mechanisms, or ESM, that are intended to encourage regulated utilities to operate efficiently. Pursuant to ESMs, if certain of the regulated utilities of

Networks earn more than certain threshold amounts, they must share with customers a specified percentage of these earnings. Below is a history of ESMs over

the past three years:

2013 2014 2015

NYSEG Electric

50% / 50%: 10.90% - 11.65%

85% / 15%: over 11.65%;

Based on Actual Equity Ratio

up to 50%

50% / 50%: 10.90% - 11.65%

85% / 15%: over 11.65%;

Based on Actual Equity Ratio

up to 50%

50% / 50%: 10.90% - 11.65%

85% / 15%: over 11.65%;

Based on Actual Equity Ratio

up to 50%

NYSEG Gas Same as above Same as above Same as above

RGE Electric Same as above Same as above Same as above

RGE Gas Same as above Same as above Same as above

CMP Dist.

50% / 50% over 11.0%

Based on 47% Equity Ratio No ESM No ESM

CMP Trans. No ESM No ESM No ESM

MNG No ESM No ESM No ESM

UI 50% / 50% over 8.90%* 50% / 50% over 9.15% 50% / 50% over 9.15%

SCG No ESM No ESM No ESM

CNG No ESM 50% / 50% over 9.18% 50% / 50% over 9.18%

Berkshire No ESM No ESM No ESM

*

UI’s rate case decision, effective in August 2013, increased the ROE threshold subject to ESM from 8.75% to 9.15%, resulting in a weighted average of 8.90% for calendar

year 2013.

10

Merger Settlement Agreement – Connecticut and Massachusetts

As part of the process of seeking and obtaining regulatory approval of the acquisition in Connecticut and Massachusetts, AVANGRID and UIL

reached settlement agreements with the Office of Consumer Counsel, or OCC, in Connecticut and with the Attorney General of the Commonwealth of

Massachusetts and the Department of Energy Resources in Massachusetts, which settlement agreements included commitments of actions to be taken after

the transaction closed. See Part II, Item 7, “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Networks” for more

information.

In connection with the acquisition proceeding, UI signed a proposed partial consent order, or the consent order that, when approved by the

Commissioner of DEEP, and pursuant to the terms and conditions in the consent order, would require UI to investigate and remediate certain environmental

conditions within the perimeter of the English Station site. To the extent that the investigation and remediation is less than $30 million, UI would remit to

the State of Connecticut the difference between such costs and $30 million for a public purpose as determined in the discretion of the Governor, the Attorney

General of Connecticut and the Commissioner of DEEP. Pursuant to the consent order, upon its issuance and subject to its terms and conditions, UI would be

obligated to comply with the consent order, even if the cost of such compliance exceeds $30 million. See Part I, Item 1, “Business – Environmental, Health

and Safety - Management, Disposal and Remediation of Hazardous Substances” for more information.

Renewables

The Renewables business, based in Portland Oregon, is engaged primarily in the design, development, construction, management and operation of

generation plants that produce electricity using renewable resources and, with more than 50 renewable energy projects, is one of the leaders in renewable

energy production in the United States based on installed capacity. Renewables’ primary business is onshore wind energy generation, which represents

approximately 89% of Renewables’ combined installed capacity as of December 31, 2015. For the year ended December 31, 2015, Renewables produced

approximately 14,135,000 MWh of energy through wind power generation. Renewables had a pipeline of approximately 5,900 MW of future renewable

energy projects in various stages of development as of December 31, 2015.

Typically, Renewables enters into long-term lease agreements with property owners who lease their land for renewable projects. Electricity generated

at a wind project is then transmitted to customers through long-term agreements with purchasers. There are a limited number of turbine suppliers in the

market. Renewables’ largest turbine suppliers, Gamesa Wind US and GE Wind, in the aggregate supplied turbines which accounted for 67% of its installed

capacity as of December 31, 2015.

Renewables currently operates 53 wind farms in 18 states across the United States.

To monetize the tax benefits resulting from production tax credits

and accelerated tax depreciation available to qualifying wind energy projects, Renewables has entered into “tax equity” financing structures with third party

investors for a portion of its wind farms. Renewables holds 12 operating wind farms under these structures through limited liability companies jointly owned

by one or more third party investors. These investors generally provide an up-front investment or, in some cases, enter into fixed and contingent notes for

their membership interests in the financing structures. In return, the investors receive a majority or all of the cash flows and tax benefits generated by the wind

farms until such benefits achieve a negotiated return on their investment. Upon attainment of this target return, the sharing of the cash flows and tax benefits

flip, with Renewables receiving substantially all of these amounts thereafter. We also have an option to repurchase the investor’s interest within a certain

timeframe after the target return is met. Renewables maintains operational and management control over the wind farm businesses, subject to investor

approval of certain major decisions. See “—Properties—Renewables” for more information regarding Renewables’ wind power generation properties.

Additionally, as part of the Renewables portfolio, Renewables operates two thermal generation facilities in the United States, with 636 MW of

combined capacity as of December 31, 2015. Renewables worked closely with the City of Klamath Falls, Oregon to develop the Klamath Plant, which has a

current capacity of 536 MW, operating by creating two useful forms of energy, electricity and process steam, from a single fuel source of natural gas. In

addition, Renewables operates a highly flexible 100 MW Klamath Peaking Plant adjacent to the Klamath Plant, providing customers of Renewables

additional capability to meet their peak summer and winter power needs.

In addition to its wind assets, Renewables operates two solar photovoltaic facilities with an installed capacity of 50 MW. The solar photovoltaic

facilities produced over 126,000 MWh of renewable energy for the year ended December 31, 2015. Solar accounted for 0.9% of the total renewable energy

generation from Renewables in these same periods.

Renewables is pursuing the continued development of a large pipeline of wind energy projects in various regions across the United States. Each site

features a range of different atmospheric characteristics that ultimately drive the selection of turbine technology for the proposed project. As part of

Renewables’ wind resource assessment investigation, critical atmospheric parameters such as mean wind speed, extreme wind speed, turbulence intensity, and

mean air density are characterized to represent long-term

11

conditions, for over 20 years. The summary wind characteristics are then combined with a terrain, or orography, analysis to assess siting risks in order to

mitigate any future operations and maintenance concerns that may arise due to improper turbine siting.

Renewables maintains close relationships with key turbine suppliers, including Gamesa, GE, Vestas, Siemens, and others in order to identify the

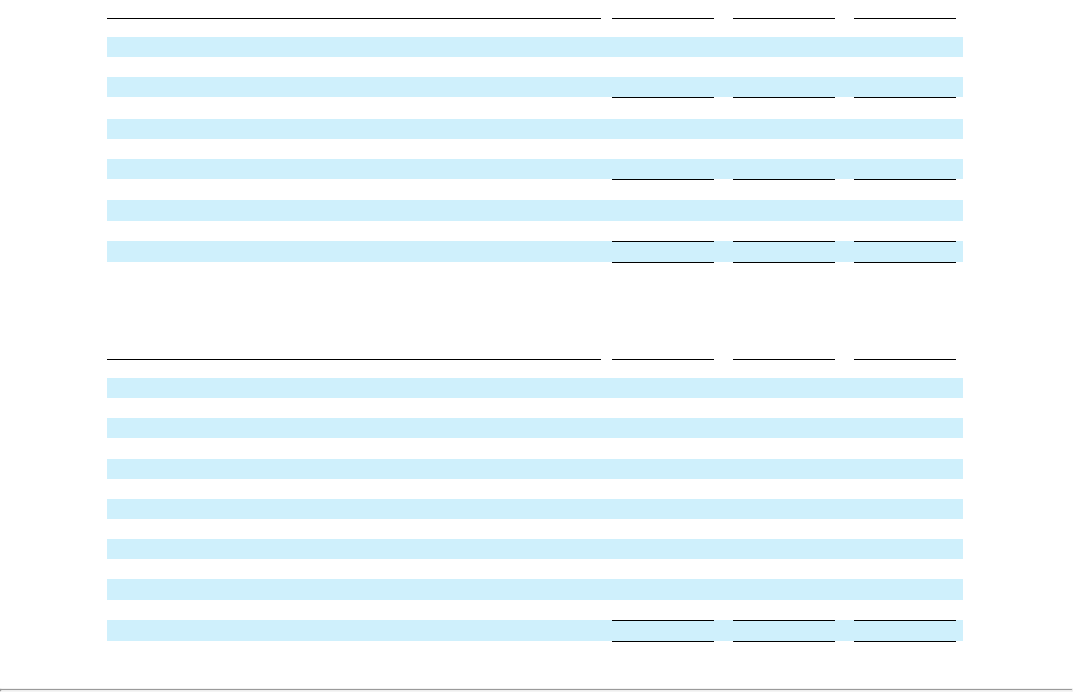

turbine technology that safely delivers the lowest cost of energy for each candidate project in its portfolio. Renewables has deployed the following mix of

turbines under this strategy. See “—Properties—Renewables” for more information regarding Renewables’ turbine technology.

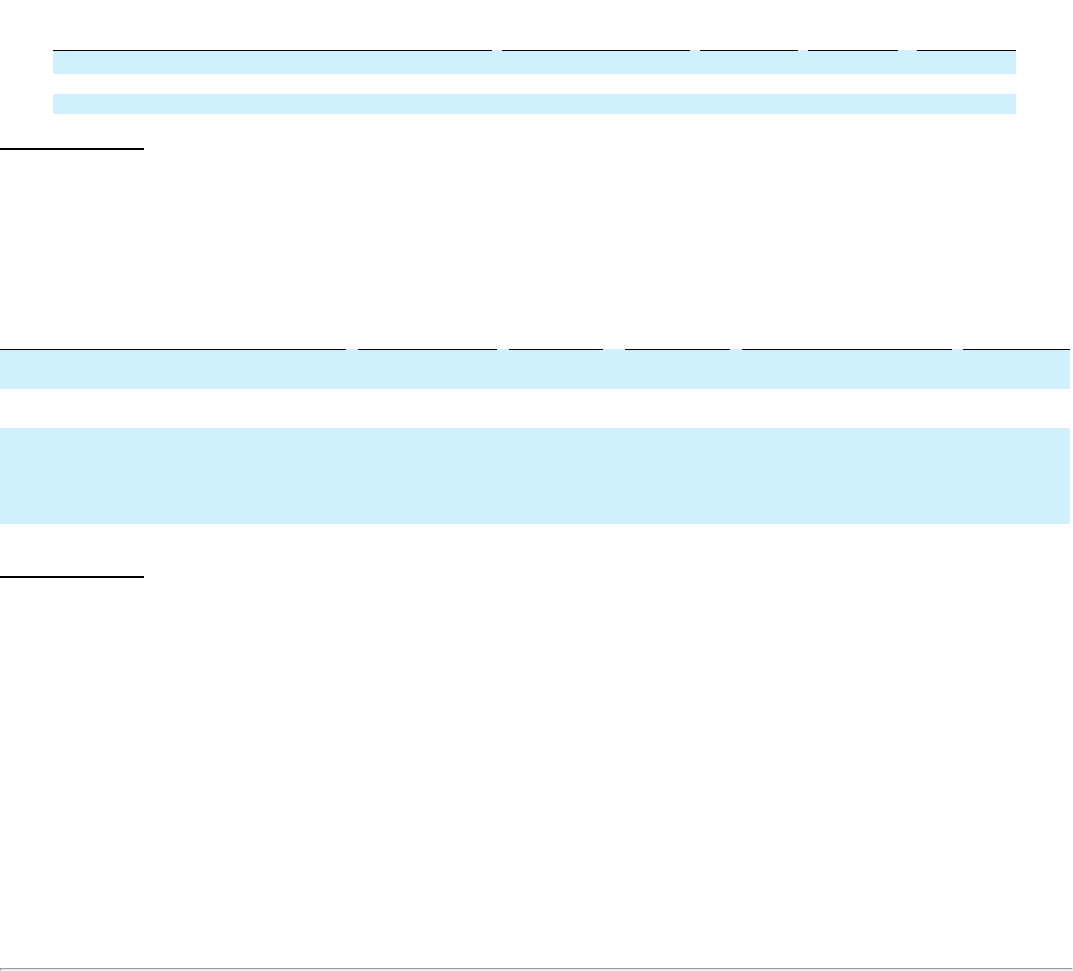

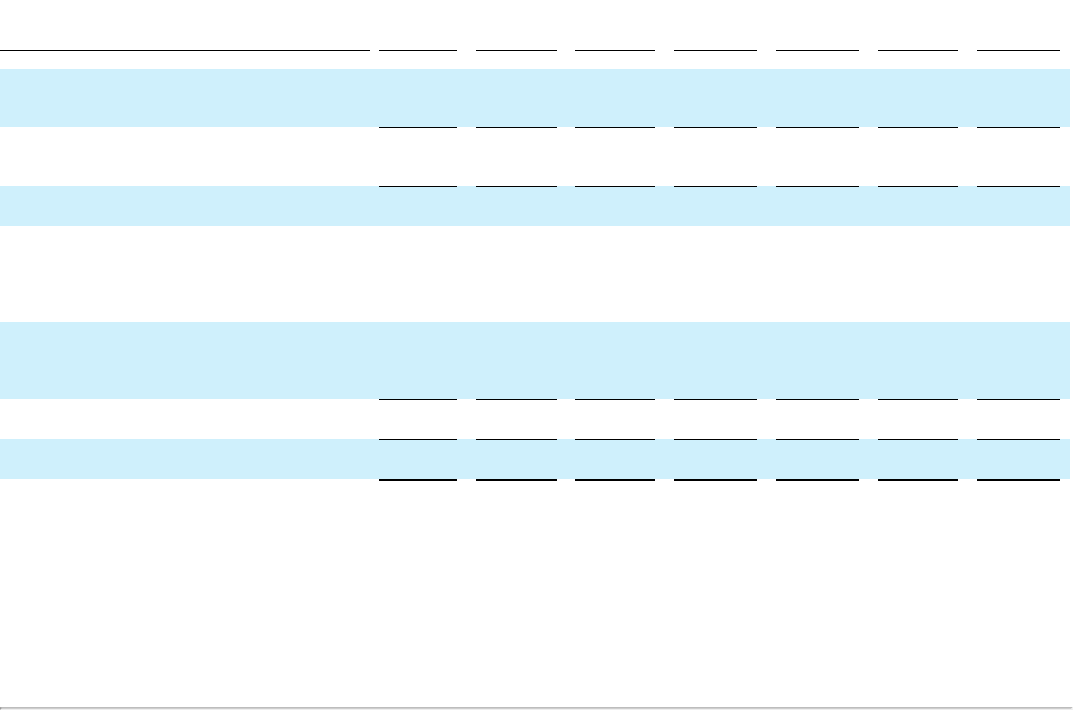

MFG Model Rating Turbines MW

Gamesa G83 2.0 61 122

Gamesa G87 2.0 643 1,286

Gamesa G90 2.0 237 474

Gamesa G97 2.0 101 202

GE 1.5s 1.5 133 200

GE 1.5sle 1.5 1,072 1,608

MHI MWT62/1.0 1.0 45 45

MHI MWT92/2.4 2.4 168 403

MHI MWT95/2.4 2.4 125 300

MHI MWT102/2.4 2.4 1 2

NEG NM48 0.7 3 2

Siemens SWT2.3-93 2.3 44 101

Suzlon S88 2.1 341 716

Vestas V47 0.7 34 22

Vestas V82 1.7 97 160

Total 3,105 5,643

The Renewables meteorology team supports the commercial development of wind energy projects in Renewables’ pipeline by performing a wide

variety of detailed investigations to characterize the expected wind energy production from a proposed wind farm in its pre-construction phase of

development. These investigations include measuring the wind resource with several well-equipped meteorological masts, utilizing state of the art laser-

based and acoustic-based remote sensing equipment, computational fluid dynamics modeling software, and energy modeling software packages that

characterize wake losses from any upwind turbines that may be present. The Renewables fleet of measurement masts consists of over 160 towers that are

currently in operation. Additionally, a total of 8 light detecting and ranging, and 6 sonic detecting and ranging, remote sensing devices are deployed at sites

across the United States. These remote sensing devices allow hub-height wind speed measurement from a ground-based sensor that can be rapidly deployed

and moved as the project matures or changes in nature. The resulting pre-construction energy production estimates that utilize these measurements have been

shown to be accurate in a multi-year internal study that compares results to actual, operational data in a benchmarking analysis. This study provides a critical

feedback loop that is used to define methodology requirements for future pre-construction energy production estimates to ensure confidence in project

investment. Renewables’ commitment to obtaining robust atmospheric measurement is driven by a company culture that values business case confidence and

understands the role that accurate meteorological data play in the pursuit of this goal.

Gas

The Gas business, based in Houston, Texas, operates a natural gas storage and natural gas trading business through its wholly-owned direct

subsidiaries, Enstor, Inc., an Oregon corporation (natural gas storage) and Enstor Energy Services LLC, a Delaware limited liability company (natural gas

trading). Gas owns and operates four natural gas storage facilities, with a total storage capacity of 88.5 Bcf and a net working gas storage capacity of 67.5 Bcf.

Enstor Operating Company, LLC, a Texas limited liability company and wholly-owned direct subsidiary of Enstor, Inc., manages all four natural gas storage

facilities. The demand for natural gas storage is dependent upon the seasonal differences in the weather. Since market prices and temporal price spreads for

natural gas reflect the demand for these products and their availability at a given time, the overall operating results of Gas’ business may fluctuate

substantially on a seasonal basis. Severe weather, such as ice and snow storms, hurricanes and other natural disasters may cause outages, bodily injury or

property damage, which may require Gas to incur additional costs, such as operation and maintenance expenses, which may not be recoverable from

customers. See “—Properties—Gas” for more information regarding Gas’ natural gas storage facilities. Enstor Energy Services LLC also contracts and

manages natural gas storage and pipeline capacity throughout the United States and parts of Canada. Gas operates 53.25 Bcf of contracted or managed

natural gas storage capacity in North America through Enstor Energy Services, LLC, as of December 31, 2015.

12

Regulatory Environment and Principal Markets

Federal Energy Regulatory Commission

Among other things, FERC regulates the transmission and wholesale sales of electricity in interstate commerce and the transmission and sale of natural

gas for resale in interstate commerce. Certain aspects of Networks’ businesses, Renewables’ competitive generation and Gas’ natural gas storage and energy

trading businesses are subject to regulation by FERC.

Pursuant to the FPA, electric utilities must maintain tariffs and rate schedules on file with FERC which govern the rates, terms and conditions for the

provision of FERC-jurisdictional wholesale power and transmission services. Unless otherwise exempt, any person that owns or operates facilities used for the

wholesale sale or transmission of power in interstate commerce is a public utility subject to FERC’s jurisdiction. FERC regulates, among other things, the

disposition of certain utility property, the issuance of securities by public utilities, the rates, the terms and conditions for the transmission or wholesale sale of

power in interstate commerce, interlocking officer and director positions, and the uniform system of accounts and reporting requirements for public utilities.

With respect to Networks’ regulated electric utilities in Maine, New York and Connecticut, FERC governs the return on equity, or ROE, rates, terms

and conditions of transmission of electric energy in interstate commerce, interconnection service in interstate commerce (which applies to independent power

generators, for example), and the rates, terms and conditions of wholesale sales of electric energy in interstate commerce, which includes cost-based rates,

market-based rates and the operations of regional capacity and electric energy markets in New England administered by an independent entity, ISO New

England, Inc., or ISO-NE, and in New York, administered by another independent entity, the New York Independent System Operator, Inc., or NYISO. FERC

approves the Networks’ regulated electric utilities’ transmission revenue requirements. Wholesale electric transmission revenues are recovered through

formula rates that are approved by FERC. CMP’s, MEPCO’s and UI’s electric transmission revenues are recovered from New England customers through

charges that recover costs of transmission and other transmission-related services provided by all regional transmission owners. NYSEG’s and RGE’s electric

transmission revenues are recovered from New York customers through charges that recover the costs of transmission, and other transmission-related services

provided by all transmission owners in New York. Several of our affiliates have been granted authority to engage in sales at market-based rates and blanket

authority to issue securities, and have also been granted certain waivers of FERC reporting and accounting regulations available to non-traditional public

utilities; however, we cannot be assured that such authorizations or waivers will not be revoked for these affiliates or will be granted in the future to other

affiliates.

Pursuant to a series of orders involving the ROE for regionally planned New England electric transmission projects, the FERC established a base-level

transmission ROE of 11.14%, as well as a 50 basis point ROE adder on Pool Transmission Facilities, or PTF, for participation in the RTO for New England

and a 100 basis point ROE incentive for projects included in the ISO-NE Regional System Plan that were completed and on line as of December 31, 2008.

Beginning in 2011, several parties filed three separate complaints with the FERC against ISO-NE and several New England transmission owners,

including UI and CMP, claiming that the current approved base ROE of 11.14% was not just and reasonable, seeking a reduction of the base ROE and a

refund to customers for the 15-month refund periods beginning October 1, 2011, December 27, 2012 and July 31, 2014, respectively.

In 2014, the FERC determined that the base ROE should be set at 10.57% for the first complaint refund period and that a utility's total or maximum

ROE should not exceed 11.74%. The FERC issued an order consolidating the second and third complaints and establishing hearing procedures. The

administrative law judge issued an initial decision in the second and third complaints on March 22, 2016. The initial decision determined that, 1) for the 15

month refund period in the second complaint, the base ROE should be 9.59% and that the ROE Cap (base ROE plus incentive ROEs) should be 10.42% and

2) for the 15 month refund period in the third complaint and prospectively, the base ROE should be 10.90% and that the ROE Cap should be 12.19%. The

initial decision is the administrative law judge’s recommendation to the FERC Commissioners. The FERC is expected to make its final decision in late 2016

or early 2017.

On March 3, 2015, the FERC issued an Order on Rehearing in the first complaint denying all rehearing requests from the complainants and the New

England transmission owners. Appeals of the FERC’s decisions on the first complaint are currently pending before the D.C. Circuit.

On December 28, 2015, the FERC issued an order instituting section 206 proceedings and establishing hearing and settlement judge

procedures. Pursuant to section 206 of the FPA, the FERC finds that ISO-NE Transmission, Markets, and Services Tariff is unjust, unreasonable, and unduly

discriminatory or preferential. FERC stated that ISO-NE’s Tariff lacks adequate transparency and challenge procedures with regard to the formula rates for

ISO-NE Participating Transmission Owners, including UI, MEPCO and CMP. FERC also found that the current Regional Network Service, or RNS and Local

Network Service, or LNS, formula rates appear to be unjust, unreasonable, unduly discriminatory or preferential, or otherwise unlawful as the formula rates

appear to lack sufficient

13

detail in order to determine how certain costs are derived and recovered in the formula rates. A settlement judge has been appointed and a settlement

conference has convened. We are unable to predict the outcome of this proceeding at this time.

FERC has the right to review books and records of “holding companies,” as defined in the Public Utility Holding Company Act of 2005, or PUHCA

2005, that are determined by FERC to be relevant to the companies’ respective FERC-jurisdictional rates. We are a holding company, as defined in PUHCA

2005.

FERC has civil penalty authority over violations of any provision of Part II of the FPA, as well as any rule or order issued thereunder. FERC is

authorized to assess a maximum civil penalty of $1.0 million per violation for each day that the violation continues. The FPA also provides for the

assessment of criminal fines and imprisonment for violations under Part II of the FPA. Pursuant to the Energy Policy Act of 2005, or EPAct 2005, the North

American Electric Reliability Corporation, or NERC, has been certified by FERC as the Electric Reliability Organization to develop and oversee the

enforcement of electric system reliability standards applicable throughout the United States. FERC-approved reliability standards may be enforced by FERC

independently, or, alternatively, by NERC and the regional reliability organizations with frontline responsibility for auditing, investigating and otherwise

ensuring compliance with reliability standards, subject to FERC oversight.

Gas’ current natural gas storage operations in the United States are subject to the jurisdiction of FERC under the Natural Gas Act of 1938, or NGA, as a

Section 7(c) natural gas storage provider (i.e., Caledonia Energy Partners, L.L.C. and Freebird Gas Storage, LLC each with Enstor Operating Company, LLC

as their manager) and by providing interstate storage and storage related services under Section 311 of the Natural Gas Policy Act of 1978 (i.e., Enstor Katy

Storage and Transportation, L.P. and Enstor Grama Ridge Storage and Transportation, LLC with Enstor Operating Company, LLC as their general partner and

manager, respectively), at market based rates. Gas’ interstate and intrastate high-deliverability multi-cycle natural gas storage service projects and operations

are subject to FERC regulation under the NGA for rates and terms of service.

Furthermore, Gas’ natural gas trading operations in the United States are subject to the jurisdiction of FERC under EPAct 2005. FERC possesses

regulatory oversight over gas markets, including the purchase, sale and transportation of gas by “any entity” in order to enforce the anti-market manipulation

provisions in EPAct 2005. The gas distribution operations of NYSEG, RGE, SCG, CNG and Berkshire, similar to Gas, are also subject to FERC regulation

with respect to their gas purchases/sales and contracted transportation/storage capacity. FERC has civil penalty authority under the NGA to impose penalties

for certain violations of up to $1.0 million per day for violations. FERC also has the authority to order the disgorgement of profits from transactions deemed

to violate the NGA and EPAct 2005. Additionally, Gas’ current natural gas trading operations are also subject to FERC regulation with respect to matters

such as market manipulation and capacity release rules.

Market Anti-Manipulation Regulation

The FERC and the Commodity Futures Trading Commission, or CFTC, monitor certain segments of the physical and futures energy commodities

market pursuant to the FPA and the Commodity Exchange Act, including our businesses’ energy transactions and operations in the United States. In July

2010, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act, or the Dodd-Frank Act, which incorporated an expansion of the

authority of the CFTC to prohibit market manipulation in the markets regulated by the CFTC. With regard to the physical purchases and sales of electricity

and natural gas, the gathering storage, transmission and delivery of these energy commodities and any related trading or hedging transactions that some of

our operating subsidiaries undertake, our operating subsidiaries are required to observe these anti-market manipulation laws and related regulations enforced

by the FERC and CFTC. The FERC and CFTC hold substantial enforcement authority, including the ability to assess civil penalties of up to $1.0 million per

day per violation, to order disgorgement of profits and to recommend criminal penalties.

State Regulation

Networks’ regulated utilities in New York, Maine, Connecticut and Massachusetts are subject to regulation by the applicable state public utility

commissions, including with regard to their rates, terms and conditions of service, issuance of securities, purchase or sale of utility assets and other

accounting and operational matters. NYSEG and RGE are subject to regulation by the NYPSC; CMP and MNG are subject to regulation by the MPUC; UI,

SCG and CNG are subject to regulation by the PURA; and Berkshire is subject to regulation by the DPU. The NYPSC, MPUC and the Connecticut Siting

Council, or CSC, exercise jurisdiction over the siting of electric transmission lines in their respective states, and each of the NYPSC, MPUC, PURA and DPU

exercise jurisdiction over the approval of certain mergers or other business combinations involving Networks’ regulated utilities. In addition, each of the

utility commissions has the authority to impose penalties on these regulated utilities, which could be substantial, for violating state utility laws and

regulations and their orders.

14

Networks’ regulated distribution utilities deliver electricity and/or natural gas to all customers in their service territory at rates established under cost

of service regulation. Under this regulatory structure, Networks’ regulated distribution utilities recover the cost of providing distribution service to their

customers based on its costs, and earn a return on their capital investment in utility assets.

The following provides a summary of Networks regulated utilities’ most recent rate cases:

·

New York. NYSEG and RGE have each completed one distribution rate case decision since they were acquired by Iberdrola, S.A. in 2008. On

September 17, 2009, NYSEG and RGE initiated a distribution rate case to allow the companies to recover past and future investments, provide

safe and adequate service, and improve their credit ratings. On February 19, 2016, the NYSEG, RGE and other signatory parties filed a Joint

Proposal, or the proposal, with the NYPSC for a three-year rate plan for electric and gas service at NYSEG and RGE commencing May 1, 2016.

The proposal balances the varied interests of the signatory parties including but not limited to maintaining the companies’ credit quality and

mitigating the rate impacts to customers. The proposal reflects many customer attributes including: acceleration of the companies’ natural gas

leak prone main replacement programs and enhanced electric vegetation management to provide continued safe and reliable service. The

allowed rate of return on common equity for NYSEG Electric, NYSEG Gas, RGE Electric and RGE Gas is 9.00%. The equity ratio for each

company is 48%. The proposal includes an ESM applicable to each company. The customer share of earnings would increase at higher

earnings levels, with customers receiving 50%, 75% and 90% of earnings over 9.5%, 10.0% and 10.5% of ROE, respectively, in the first year.

Earnings thresholds would increase in subsequent years. The proposal reflects the recovery of deferred NYSEG Electric storm costs of

approximately $262 million, of which $123 million will be amortized over ten years and the remaining $139 million will be amortized over

five years. The proposal also continues reserve accounting for qualifying Major Storms ($21.4 million annually for NYSEG Electric and $2.5

million annually for RGE Electric). Incremental maintenance costs incurred to restore service in qualifying divisions will be chargeable to the

Major Storm Reserve provided they meet certain thresholds. The administrative law judges assigned to the New York rate case will issue a

procedural schedule establishing the remaining procedure for review and decision on the proposal. We expect hearings on the proposal to be

held in April 2016 and a NYPSC decision to be made in May 2016.

·

Maine. On May 1, 2013, CMP filed a distribution service rate case in order to recover past and future investments and provide safe and

adequate service. On August 25, 2014, MPUC approved a stipulation agreement which provided for a distribution rate increase of

approximately $24.3 million effective July 1, 2014 with an allowed ROE of 9.45% and an allowed equity ratio of 50%.

On March 5, 2015, MNG filed a rate case in order to recover future investments and provide safe and adequate service. MNG requested a

10.0% ROE and 50% equity ratio. The MPUC Staff has recommended a separate revenue requirement for MNG’s Augusta customers and

MNG’s non-Augusta customers. Staff has recommended a $19.95 million disallowance of the Augusta Expansion investment based upon the

Staff’s conclusion that MNG’s management of the Augusta Expansion Project was imprudent. On November 6, 2015, a stipulation was filed

with the MPUC, which was executed by MNG, the Office of Public Advocate and the City of Augusta. The stipulation contained a combined

revenue requirement for Augusta and Non-Augusta based on a 9.55% ROE and 50% equity ratio. The stipulation also provided for an initial

Augusta investment disallowance of $6 million and an investment phase-in of $10 million. On December 22, 2015, MPUC rejected the

proposed stipulation as not in the public interest. In January 2016, the administrative law judge established a new litigation schedule. The

litigation was suspended at the end of January 2016 for settlement discussions. We cannot predict the outcome of the proceeding.

·

Connecticut. In August 2013, PURA approved distribution rate schedules for UI for two years that became effective at that time and which,

among other things, increased the UI distribution allowed ROE from 8.75% to 9.15%, continued UI’s existing earnings sharing mechanism,

continued the existing decoupling mechanism (under which the actual energy delivery revenues are compared on a periodic basis with the

authorized delivery revenues and the difference accrued, with interest, for refund to or recovery from customers, as applicable), and approved

the establishment of the requested storm reserve. In connection with the approval by PURA of the acquisition, UI agreed not to file a rate case

for new rates effective before January 1, 2017.

The allowed ROEs established by PURA for CNG and SCG, are 9.18% and 9.36%, respectively. SCG and CNG each have purchased gas

adjustment clauses that enable them to pass their reasonably incurred cost of gas purchases through to customers. These clauses allow utilities

to recover costs associated with changes in the market price of purchased natural gas, substantially eliminating exposure to natural gas price

risk.

15

On January 22, 2014, PURA approved base delivery rates for CNG, with an effective date of January 10, 2014, which, among other things,

approved an allowed ROE of 9.18%, continued the purchased gas adjustment clause, instituted a revenue decoupling mechanism, established

two separate ratemaking mechanisms that reconcile actual revenue requirements related to CNG’s cast iron and bare steel replacement program

and system expansion and an earnings sharing mechanism by which CNG and customers share on a 50/50 basis all earnings above the allowed

ROE in a calendar year. In accordance with the approval by PURA of the acquisition, SCG and CNG agreed not to file rate cases for new rates

effective before January 1, 2018.

·

Massachusetts. Berkshire’s rates are established by the DPU. Berkshire’s 10-year rate plan, which was approved by the DPU and included an

approved ROE of 10.5%, expired on January 31, 2012. Berkshire continues to charge the rates that were in effect at the end of the rate plan. In

accordance with the approval by the DPU of the acquisition, Berkshire agreed not to file a rate case for new rates effective before June 1, 2018.

Further, as a result of a restructuring of the utility industry in New York, Maine, Connecticut and Massachusetts, most of Networks’ distribution

utilities’ customers have the opportunity to purchase their electricity or natural gas supplies from third-party energy supply vendors. Most customers in New

York, however, continue to purchase such supplies through the distribution utilities under regulated energy rates and tariffs. In Maine, CMP customers can

also purchase electric supply from competitive providers but the majority receives baseline standard offer service that is provided through a MPUC

procurement process. Networks’ regulated utilities in New York, Connecticut and Massachusetts and MNG purchase electricity or natural gas from

unaffiliated wholesale suppliers and recover the actual approved costs of these supplies on a pass-through basis, as well as certain costs associated with

industry restructuring, through reconciling rate mechanisms that are periodically adjusted.

In April 2014 the NYPSC instituted its Reforming the Energy Visions, or REV, proceeding, the goals of which are to improve electric system

efficiency and reliability, encourage renewable energy resources, support DER, and empower customer choice. In this proceeding, the NYPSC is examining

the establishment of a Distributed System Platform, or DSP, to manage and coordinate DER, and provide customers with market data and tools to manage

their energy use. The NYPSC has determined distribution utilities should be the DSP providers. The NYPSC also is examining how its regulatory practices

should be modified to incent utility practices to promote REV objectives. The proceeding is following a two-phased schedule with an order relating to policy

determinations for DSP and related matters issued in February 2015 and an order for regulatory design and regulatory matters, expected in 2016. All electric

utilities have been ordered to file an initial Distributed System Implementation Plan, or DSIP, by June 30, 2016. The DSIP will also include information

regarding the potential deployment of Automated Metering Infrastructure, or AMI.

State public utility commissions may also have jurisdiction over certain aspects of Renewables’ competitive generation businesses. For example, in

New York, certain Renewables’ generation subsidiaries are electric corporations subject to “lightened” regulation by the NYPSC. As such, the NYPSC

exercises its jurisdictional authority over certain non-rate aspects of the facilities, including safety, retirements, and the issuance of debt secured by recourse

to those generation assets located in New York. In Texas, Renewables’ operations within the Electric Reliability Council of Texas, or ERCOT, footprint are

not subject to regulation by FERC, as they are deemed to operate solely within the ERCOT market and not in interstate commerce. These operations are

subject to regulation by the Public Utility Commission of Texas, or PUCT. In California, Renewables’ generation subsidiaries are subject to regulation by the

California Public Utilities Commission with regard to certain non-rate aspects of the facilities, including health and safety, outage reporting and other aspects

of the facilities’ operations. Furthermore, Gas’ natural gas storage operations are subject to certain state regulations, such as the Railroad Commission of

Texas for its facilities located in Texas.

RTOs and ISOs

Networks’ regulated electric utilities in New York, Connecticut and Maine, as well as some of Renewables’ generation fleet, operate in or have access

to organized energy markets, known as regional transmission organizations, or RTOs, or independent system operators, or ISOs, particularly NYISO and ISO-

NE. Each organized market administers centralized bid-based energy, capacity and ancillary services markets pursuant to tariffs approved by FERC, or in the

case of ERCOT, market rules approved by the PUCT. These tariffs and rules dictate how the energy, capacity and ancillary service markets operate, how

market participants bid, clear, are dispatched, make bilateral sales with one another, and how entities with market-based rates are compensated. Certain of

these markets set prices, referred to as Locational Marginal Prices that reflect the value of energy, capacity or certain ancillary services, based upon

geographic locations, transmission constraints, and other factors. Each market is subject to market mitigation measures designed to limit the exercise of

market power. Some markets limit the prices of the bidder based upon some level of cost justification. These market structures impact the bidding, operation,

dispatch and sale of energy, capacity and ancillary services.

The RTOs and ISOs are also responsible for transmission planning and operations within their respective regions. Each of Networks’ transmission-

owning subsidiaries in New York, Connecticut and Maine has transferred operational control over certain of its electric transmission facilities to its respective

ISOs, such as ISO-NE and NYISO.

16

New Renewable Source Generation

Under Connecticut law Public Act 11-80, or PA 11-80, Connecticut electric utilities are required to enter into long-term contracts to purchase

Connecticut Class I Renewable Energy Certificates, or RECs, from renewable generators located on customer premises. Under this program, UI is required to

enter into contracts totaling approximately $200 million in commitments over an approximate 21-year period. The obligations will phase in over a six-year

solicitation period, and are expected to peak at an annual commitment level of about $13.6 million per year after all selected projects are online. Upon

purchase, UI accounts for the RECs as inventory. UI expects to partially mitigate the cost of these contracts through the resale of the RECs. PA 11-80

provides that the remaining costs (and any benefits) of these contracts, including any gain or loss resulting from the resale of the RECs, are fully recoverable

from (or credited to) customers through electric rates.

On October 23, 2013, PURA approved UI’s renewable connections program filed in accordance with PA 11-80, through which UI will develop up to

10 MW of renewable generation. The costs for this program will be recovered on a cost of service basis. PURA established a base ROE to be calculated as the

greater of: (A) the current UI authorized distribution ROE (currently 9.15%) plus 25 basis points and (B) the current authorized distribution ROE for The

Connecticut Light and Power Company, or CL&P, (currently 9.17%), less target equivalent market revenues (reflected as 25 basis points). In addition, UI will

retain a percentage of the market revenues from the project, which percentage is expected to equate to approximately 25 basis points on a levelized basis over

the life of the project. UI expects the cost of this program, a planned 2.8 MW fuel cell facility in New Haven, solar photovoltaic and fuel cell facilities

totaling 5 MW in Bridgeport, and a 2.2 MW fuel cell facility in Woodbridge, to be approximately $47 million.

Pursuant to Section 8 of Connecticut Public Act 13-303, “An Act Concerning Connecticut’s Clean Energy Goals,” in January 2014, at DEEP’s

direction, UI entered into three contracts for the purchase of RECs associated with an aggregate of 5.7 MW of energy production from biomass plants in New

England. The costs of these agreements will be fully recoverable through electric rates.

Under Maine law 35-A M.R.S.A §§ 3210-C, 3210-D, the MPUC is authorized to conduct periodic requests for proposals seeking long-term supplies of

energy, capacity or RECs, from qualifying resources. The MPUC is further authorized to order Maine Transmission and Distribution Utilities to enter into

contracts with sellers selected from the MPUC’s competitive solicitation process. Pursuant to a MPUC Order dated October 8, 2009, CMP entered into a 20-

year agreement with Evergreen Wind Power III, LLC, on March 31, 2010, to purchase capacity and energy from Evergreen’s 60 MW Rollins wind farm in

Penobscot County, Maine. CMP’s purchase obligations under the Rollins contract are approximately $7 million per year. In accordance with subsequent

MPUC orders, CMP periodically auctions the purchased Rollins energy to wholesale buyers in the New England regional market. Under applicable law, CMP

is assured recovery of any differences between power purchase costs and achieved market revenues through a reconcilable component of its retail distribution

rates. Although the MPUC has conducted multiple requests for proposals under M.R.S.A §3210-C and has tentatively accepted long-term proposals from

other sellers, these selections have not yet resulted in additional currently effective contracts with CMP.

New England East-West Solution

Pursuant to an agreement with CL&P, UI has the right to invest in, and own transmission assets associated with, the Connecticut portion of CL&P’s,

New England East West Solution, or NEEWS, projects to improve regional energy reliability. NEEWS originally consisted of four inter-related transmission

projects being developed by subsidiaries of Northeast Utilities (doing business as Eversource Energy), the parent company of CL&P, in collaboration with

National Grid USA. Three of the original projects have portions located in Connecticut: (1) the Greater Springfield Reliability Project, which was fully

energized in November 2013, (2) the Interstate Reliability Project, which was placed in service in the fourth quarter of 2015 and (3) the Central Connecticut

Reliability Project, the need for which is now planned to be addressed by CL&P’s Greater Hartford Central Connecticut solutions, in which UI does not

anticipate making any investments. Under the agreement, as of December 31, 2015, UI had made aggregate deposits of approximately $45 million since its

inception, with assets valued at approximately $44.6 million having been transferred to UI. UI does not anticipate making any additional investments in

NEEWS under the agreement.

Environmental, Health and Safety

Permitting and Other Regulatory Requirements

Networks. Similar to Renewables and Gas, Networks’ distribution utilities in New York, Maine, Connecticut and Massachusetts are subject to various

federal, state and local laws and regulations in connection with the environmental, health and safety effects of its operations. The distribution utilities of

Networks are subject to regulation by the applicable state public utility commission with respect to the siting and approval of electric transmission lines, with

the exception of UI, the siting of whose transmission lines is subject to the jurisdiction of the CSC, and with respect to pipeline safety regulations for

intrastate gas pipeline operators.

17

The National Environmental Policy Act, or NEPA, requires that detailed statements of the environmental effect of Networks’ facilities be prepared in

connection with the issuance of various federal permits and licenses. Federal agencies are required by NEPA to make an independent environmental

evaluation of the facilities as part of their actions during proceedings with respect to these permits and licenses.

Under the federal Toxic Substances Control Act, the Environmental Protection Agency, or EPA, has issued regulations that control the use and

disposal of Polychlorinated Biphenyls, or PCBs. PCBs were widely used as insulating fluids in many electric utility transformers and capacitors

manufactured before the federal Toxic Substances Control Act prohibited any further manufacture of such PCB equipment. Fluids with a concentration of

PCBs higher than 500 parts per million and materials (such as electrical capacitors) that contain such fluids must be disposed of through burning in high

temperature incinerators approved by the EPA. For our gas distribution companies, PCBs are sometimes found in the distribution system. Networks and UIL

test any distribution piping being removed or repaired for the presence of PCBs and comply with relevant disposal procedures, as needed.

Under the federal Resource Conservation and Recovery Act, or RCRA, the generation, transportation, treatment, storage and disposal of hazardous

wastes are subject to regulations adopted by the EPA. All of Networks’ and UIL’s subsidiaries have complied with the notification and application

requirements of present regulations, and the procedures by which the subsidiaries handle, store, treat and dispose of hazardous waste products comply with

these regulations.

Prior to the last quarter of the 20th century, when environmental best practices laws and regulations were implemented, utility companies, including

Networks and UIL subsidiaries, often disposed of residues from operations by depositing or burying them on-site or disposing of them at off-site landfills or

other facilities. Typical materials disposed of include coal gasification byproducts, fuel oils, ash, and other materials that might contain PCBs or that

otherwise might be hazardous. In recent years it has been determined that such disposal practices, under certain circumstances, can cause groundwater

contamination.

Renewables. Renewables’ projects are subject to a variety of state environmental review and permitting requirements. Many states where Renewables’

projects are located, or may in the future be located, have laws that require state agencies to evaluate a broad array of environmental impacts before granting

state permits. State agencies evaluate similar issues as federal agencies, including the project’s impact on wildlife, historic sites, aesthetics, wetlands and

water resources, agricultural operations and scenic areas. States may impose different or additional monitoring or mitigation requirements than federal

agencies. Additional approvals may be required for specific aspects of a project, such as stream or wetland crossings, impacts to designated significant

wildlife habitats, storm water management and highway department authorizations for oversize loads and state road closings during construction. Permitting

requirements related to transmission lines may be required in certain cases.

Renewables’ projects also are subject to local environmental and regulatory requirements, including county and municipal land use, zoning, building